Beschreibung

|

|

Erstellt von Donald Foss

vor etwa 4 Jahre

|

|

Anmerkungen:

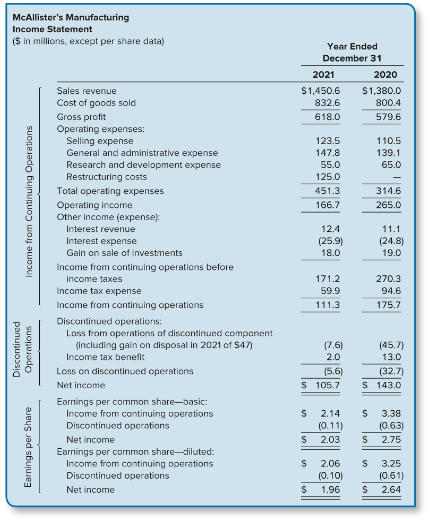

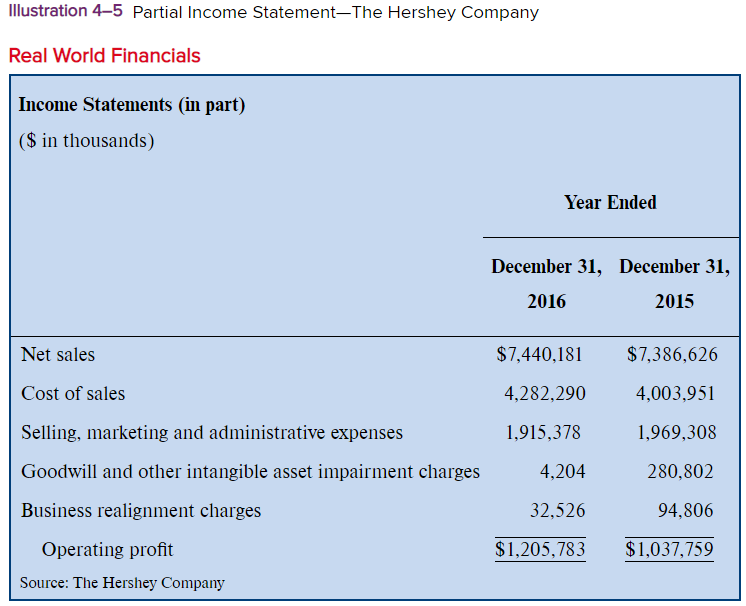

- Statement of operations or statement of earnings that is used to summarize the profit-generating activities that occurred during a particular reporting period

- Income from

Continuing

Operations

Anmerkungen:

- These are the revenues, expenses (including income taxes), gains, and losses, EXCLUDING those related to discontinued operations and extraordinary items. More likely to continue into the future.

- Operating

Income

Anmerkungen:

- Includes revenues, expenses, gains, and losses directly related to the principal revenue-generating activities of the company

- e.g., Sales revenues less COGS

(gross profit), service revenue

less operating expenses

- **May still involve unusual or infrequent events**

Anmerkungen:

- In general, the more frequently these sorts of unusual charges occur, the more appropriate it is that financial statement users include them in their estimation of the company's permanent earnings stream.

- Unusual items included in operating income require investigation to determine their permanent or temporary nature, and subsequently their impact on earnings quality.

- Restructuring costs

Anmerkungen:

- Costs associated with plans by management to materially change either the scope or manner in which its company's operations are conducted

- Examples include furloughing employees, closing manufacturing plants or shifting production to a new location.

- Companies undertake these moves in an effort to boost profitability, but first must take a one-off hit in the form of an upfront restructuring charge.

- Goodwill impairment

- Asset impairment

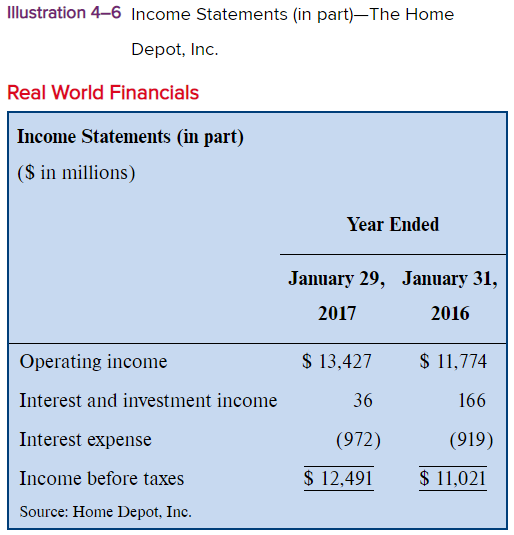

- Nonoperating

Income

Anmerkungen:

- Includes revenues, expenses, gains, and losses related to peripheral or incidental activities of the company

- e.g., Interest revenue,

gains/losses from selling

investments, etc.

- Typically relate

only tangentially

to normal

operations

Anmerkungen:

- Investors need to understand that some of these items may recur, such as interest expense, while others are less likely to recur, such as gains and losses on investments.

- Income Tax

Expense

- Can involve

intraperiod tax

allocation

Anmerkungen:

- Separating income tax expense from continuing and discontinued operations and reporting as discrete line items

- Can involve

intraperiod tax

allocation

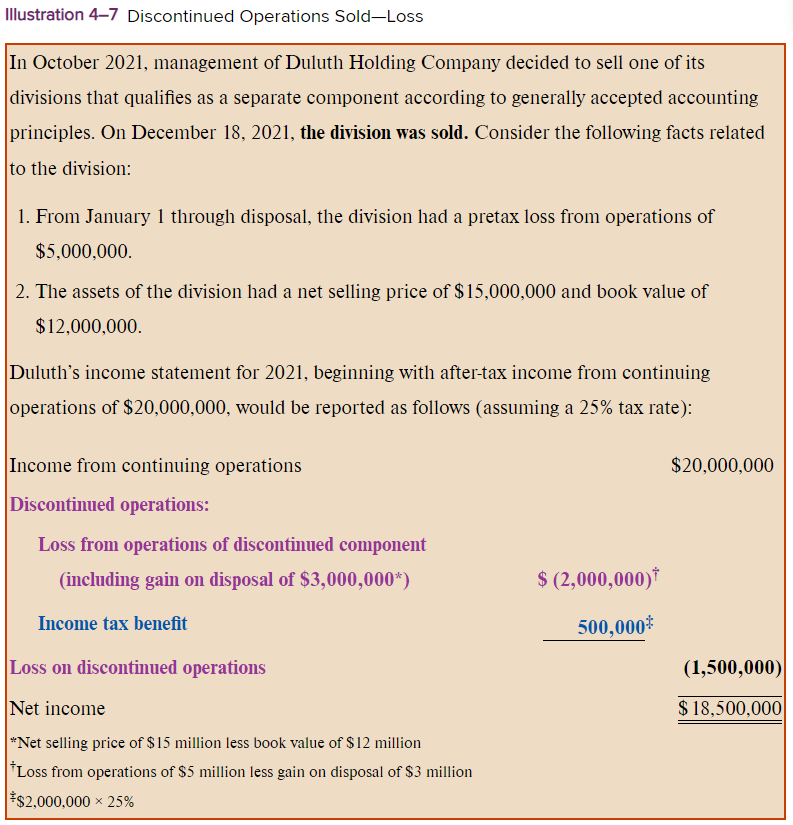

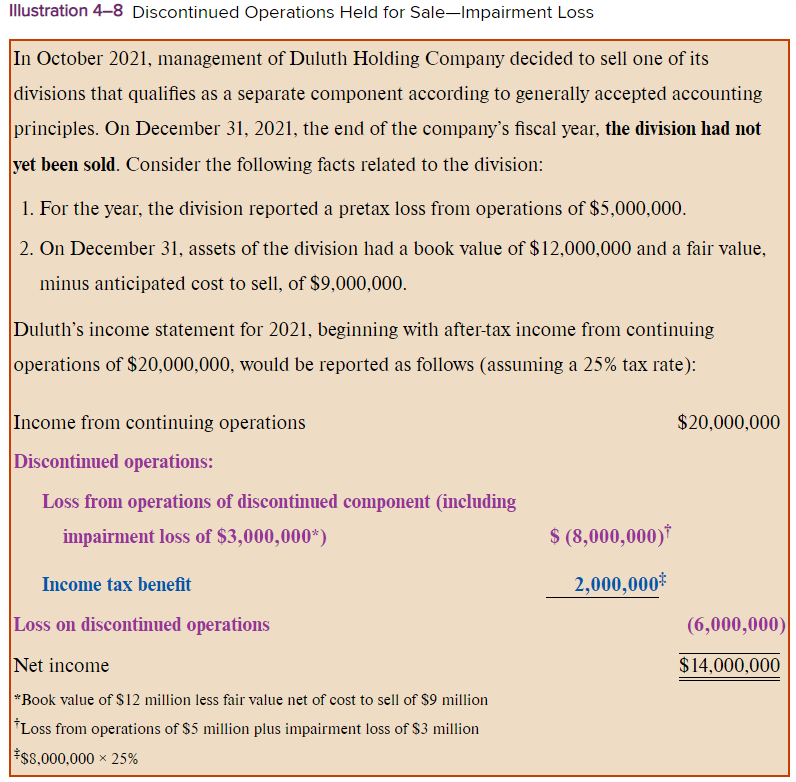

- Discontinued

Operations

Anmerkungen:

- The discontinuance of a component of an entity whose operations and cash flows can be clearly distinguished from the rest of the entity.

- Recognized if:

- A component of an entity

has been sold/disposed,

or is held for sale

Anmerkungen:

- Includes activities and cash flows that can be clearly distinguished from the rest of the company

- When the component has been sold,

recognize:

- Income from operations of the

component from the beginning of the

reporting period to the disposal date

Anmerkungen:

- Would include typical revenues from sales to customers and ordinary expenses such as cost of goods sold, salaries, rent, and insurance

- Gain/loss

on disposal

of assets

Anmerkungen:

- Would include gains and losses on the sale of assets, such as selling a building or office equipment of this discontinued component

- Income from operations of the

component from the beginning of the

reporting period to the disposal date

- When the component is held for

sale, recognize:

- Income from operations of the

component from the beginning

of the reporting period to the

end of the reporting period

- Potential impairment loss

Anmerkungen:

- Recognized if the book (carrying) value/amount of the assets of the component is more than fair value minus cost to sell

- Income from operations of the

component from the beginning

of the reporting period to the

end of the reporting period

- The disposal represents a

strategic shift that will have a

major effect on the

company's operations

Anmerkungen:

- Requires the judgment of company management; examples of possible strategic shifts include the disposal of operations in a major geographical area, a major line of business, a major equity method investment, or other major parts of the company

- A component of an entity

has been sold/disposed,

or is held for sale

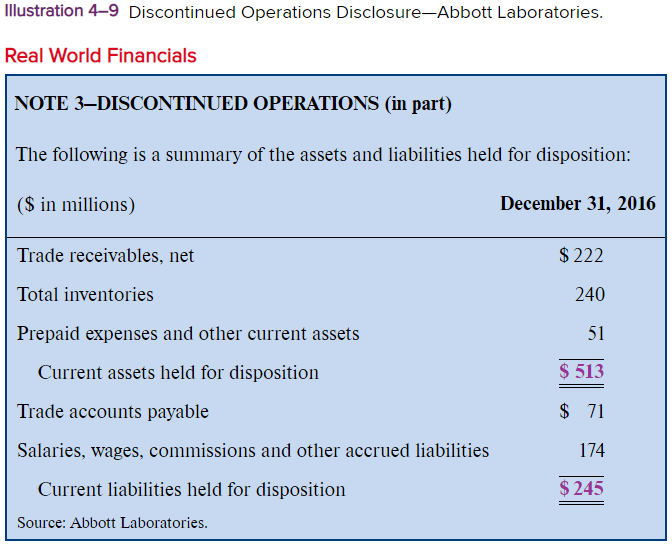

- Important info about

discontinued operations is

reported in a disclosure note

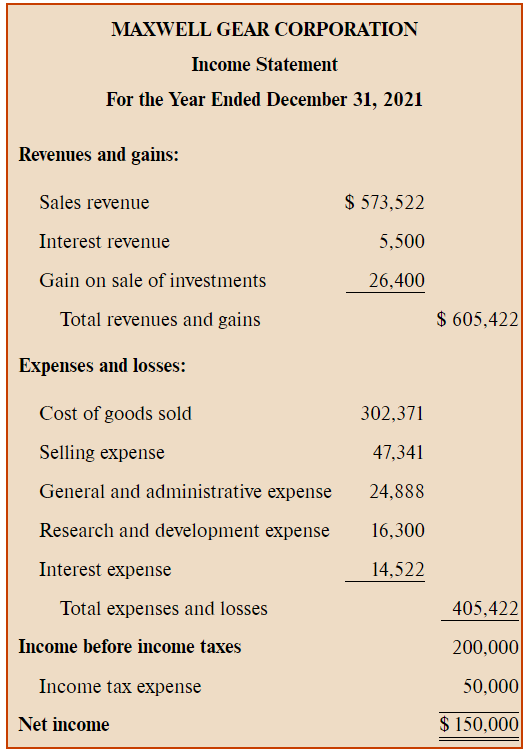

- Single-step

Anmerkungen:

- Income statement format that groups all revenues and gains together and all expenses and losses together

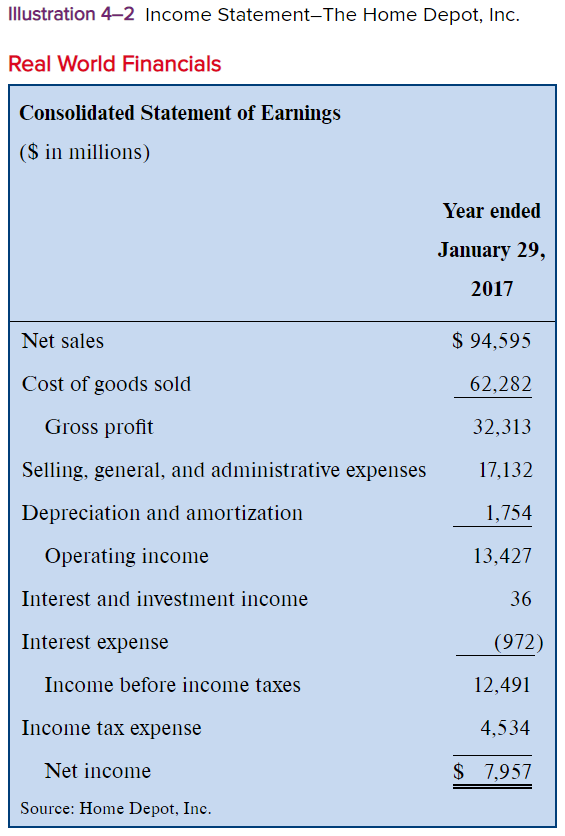

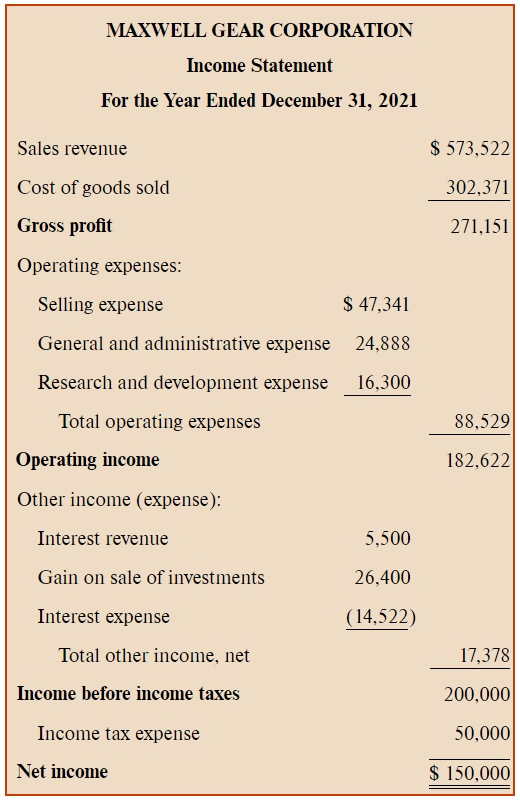

- Multiple-step

Anmerkungen:

- Income statement format that includes a number of intermediate subtotals before arriving at income from continuing operations. Most companies use this format.

- Earnings Quality

Anmerkungen:

- Refers to the ability of reported earnings (income) to predict a company's future earnings

- Income smoothing

Anmerkungen:

- In a year where income is high, managers may create reserves by overestimating certain expenses (such as future bad debts or warranties). These reserves reduce reported income in the current year.

- Then, in later years, they can use those reserves by underestimating expenses, which will increase reported income.

- By shifting income in this manner, managers effectively smooth the pattern in reported income over time, portraying a steadier income stream to investors, creditors, and other financial users.

- Helps investors predict

future performance,

but also hides volatility

- Classification shifting

Anmerkungen:

- Could involve misclassifying operating expenses as nonoperating expenses, thereby reporting fewer operating expenses and subsequently higher operating income.

- Creates the appearance of

stronger performance for

core operations

- Non-GAAP

Earnings

Anmerkungen:

- Actual (GAAP) earnings reduced by any expenses the reporting company feels are unusual and should be excluded.

- Common expenses excluded are restructuring costs, acquisition costs, write-downs of impaired assets, and stock-based compensation

- Supposedly management's view of

"permanent earnings," though

controversial

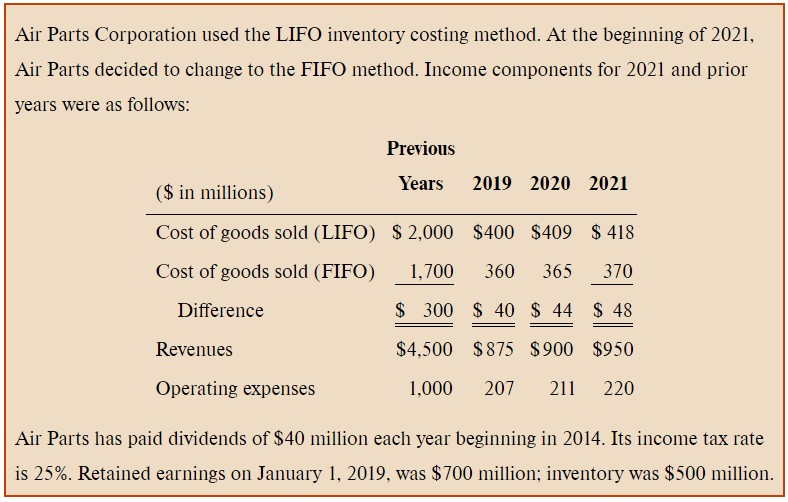

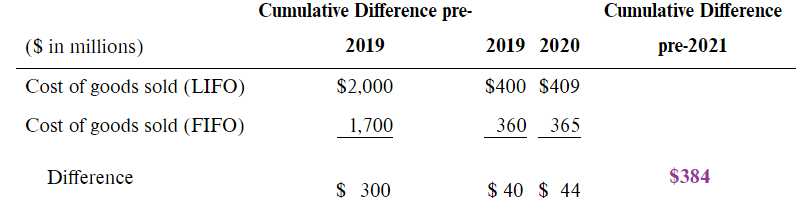

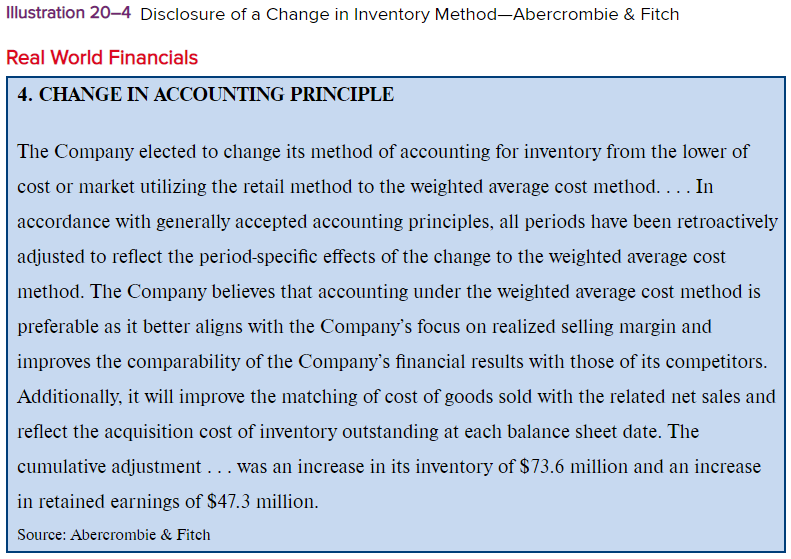

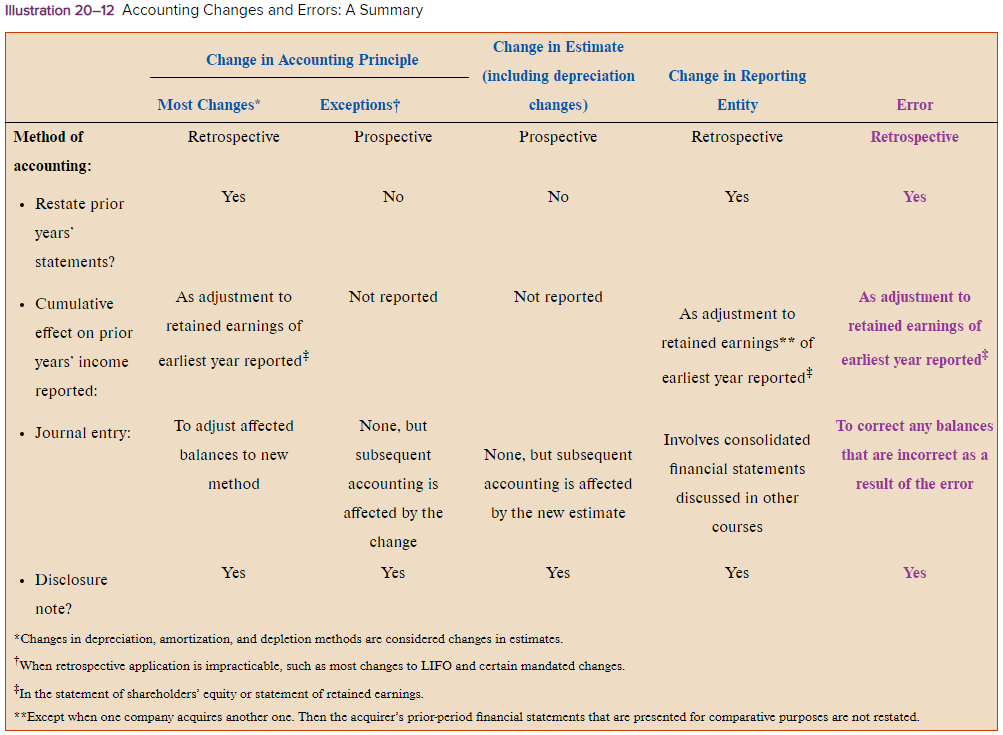

- Accounting Changes

- Accounting principle

Anmerkungen:

- Change from one generally accepted accounting principle to another

- 1. Revise comparative financial statements

Anmerkungen:

- When accounting changes occur, the usefulness of the comparative financial statements is enhanced with retrospective application of those changes.

- 2. Adjust accounts for the change

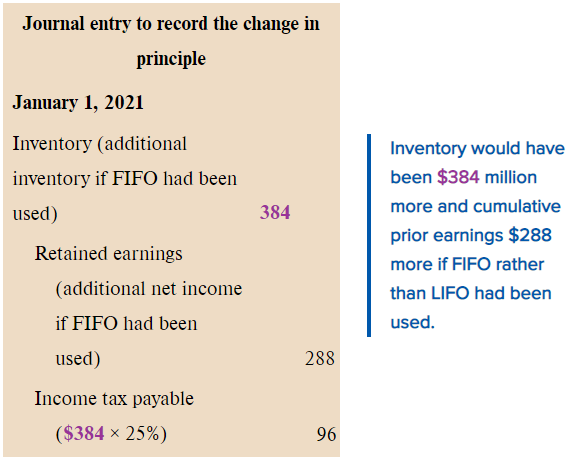

Anmerkungen:

- Air Parts adjusts the book balances of affected accounts by creating a journal entry to change those balances from their current amounts (from using LIFO) to what those balances WOULD have been using the newly adopted method (FIFO).

- 3. Disclosure

notes

Anmerkungen:

- Note disclosure explains why the change was needed as well as its effects on items NOT reported on the face of the primary statements.

- Usually retrospective

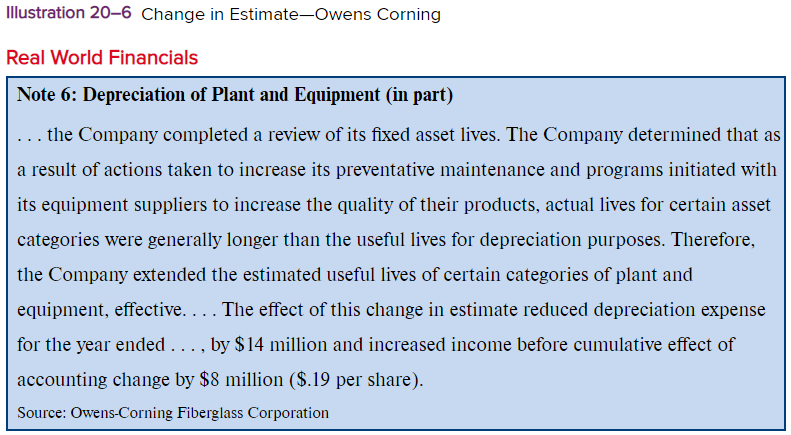

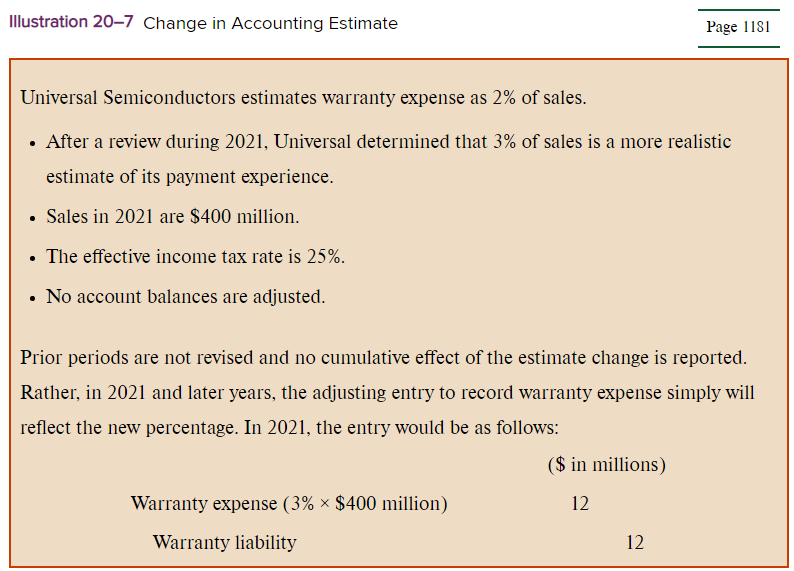

- Estimate

Anmerkungen:

- Revise an estimate because of new information or new experience

- Reflected in the financial statements

of current and future periods

Anmerkungen:

- Prior financial statements are not revised. If the effect is considered material, a disclosure note should describe the effect of the change.

- Prospective

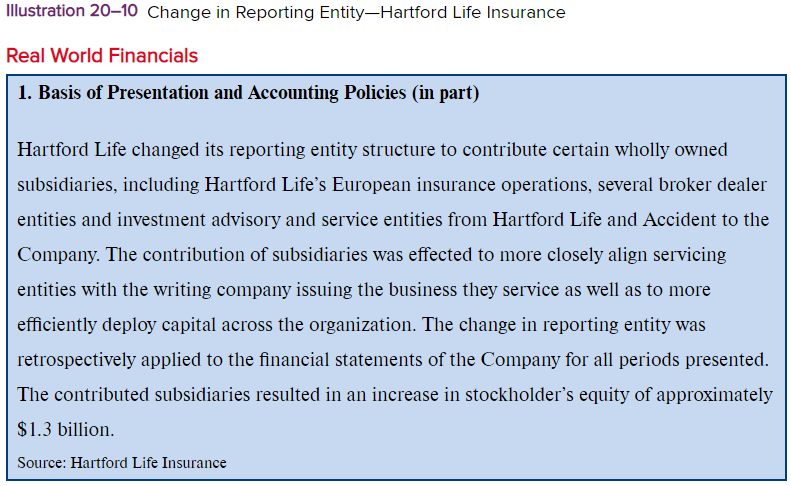

- Reporting entity

Anmerkungen:

- Change of reporting as one type of entity to another type of entity

- Retrospective

Anmerkungen:

- A change in reporting entity requires that financial statements of prior periods be retrospectively revised to report the financial information for the new reporting entity in all periods.

- Error correction

Anmerkungen:

- Correct an error caused by a transaction being recorded incorrectly or not at all

- Retrospective

Anmerkungen:

- Previous years' financial statements are retrospectively restated to reflect the correction of an error. Any account balances that are incorrect as a result of the error are corrected by a journal entry.

- Prior period adjustment

Anmerkungen:

- An addition to or reduction in the beginning retained earnings balance in a statement of shareholders' equity due to a correction of an error.

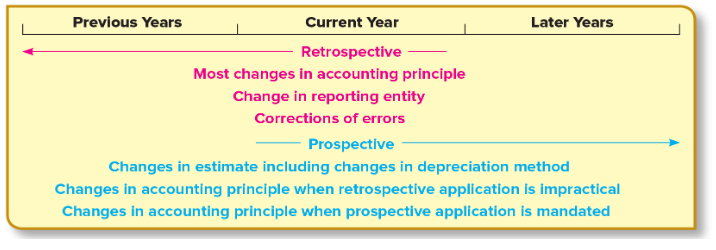

- Three approaches:

- Retrospective

Anmerkungen:

- Financial statements issued in previous years are revised to reflect the impact of an accounting change whenever those statements are presented again for comparative purpose.

- Most changes in accounting

principle use this approach

Anmerkungen:

- (except for most changes from FIFO to LIFO)

- Modified retrospective

Anmerkungen:

- Accounting change is applied ONLY to the adoption period (that is, the current period) with adjustment of the balance of retained earnings at the beginning of the adoption period to capture the cumulative effects of prior periods.

- Prospective

Anmerkungen:

- Effects of a change are reflected in the financial statements of only the year of the change and future years.

- Sometimes a lack of information makes it impracticable to report a change retrospectively so the new method is simply applied prospectively.

- Used when:

- Mandated by authoritative

accounting literature

- Changing depreciation, amortization,

or depletion methods

Anmerkungen:

- A change in depreciation methods is considered to be a change in accounting estimate that is achieved by a change in accounting principle. As a result, we account for such a change prospectively.

- A change in depreciation method is both a change in accounting principle AND in estimate.

- Cannot determine certain

period-specific effects, or

cumulative effects of prior years

Anmerkungen:

- If it's impracticable to adjust each year reported, the change is applied retrospectively as of the earliest year practicable.

- If full retrospective application isn't possible, the new method is applied prospectively beginning in the earliest year practicable.

- Mandated by authoritative

accounting literature

- Retrospective

- Accounting principle

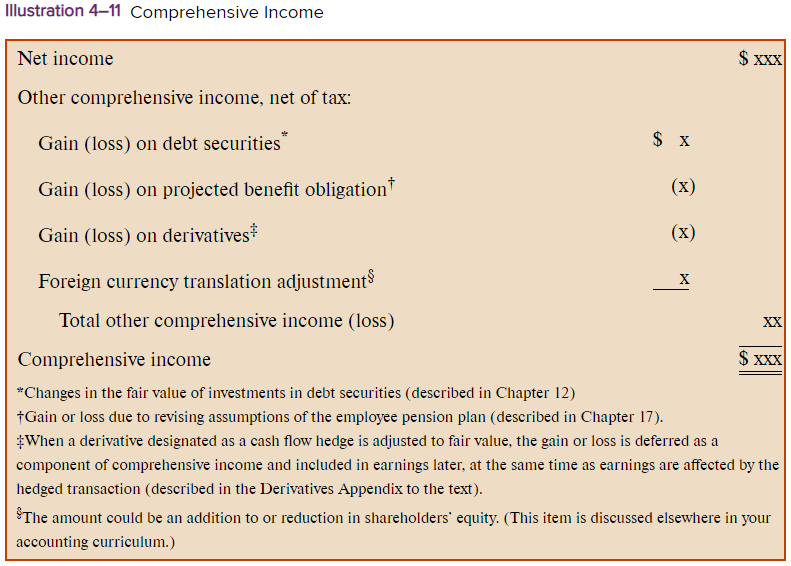

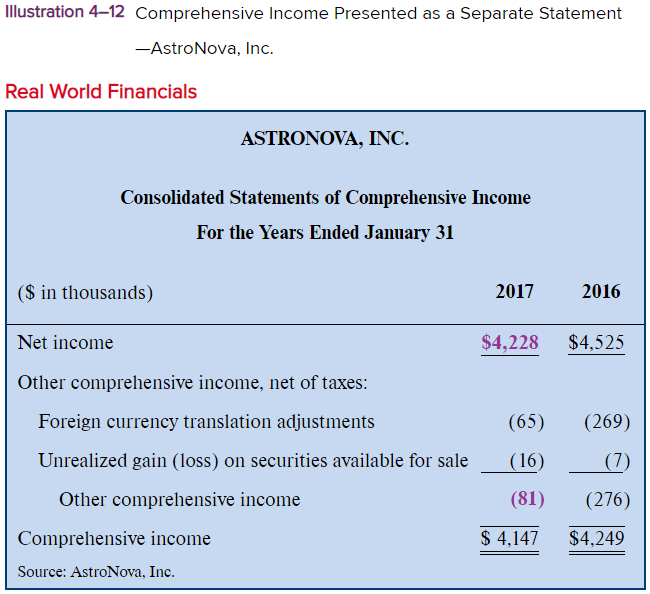

- Comprehensive Income

Anmerkungen:

- Change in shareholders' equity for the period from nonowner sources; equal to net income plus other comprehensive income. Traditional net income plus other nonowner changes in equity.

- Currently, the FASB has established no conceptual basis for determining which gains and losses qualify for net income versus other comprehensive income. To help avoid confusion, companies are required to provide a reconciliation from net income to comprehensive income.

- Net income

Anmerkungen:

- The transactions and events that lead to changes in equity from nonowner sources are recorded as revenues, expenses, gains, and losses. They are reported in the income statement are used to calculate net income.

- Other comprehensive

income

Anmerkungen:

- Changes in stockholders' equity other than transactions with owners and other than items that affect net income

- Can be reported as a single,

continuous statement OR in two

separate, but consecutive statements

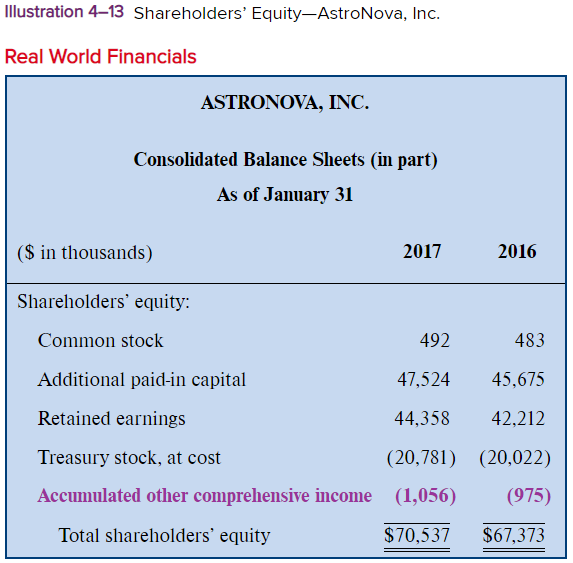

- Accumulated other

comprehensive income

(AOCI)

Anmerkungen:

- A component of stockholders' equity that reports the accumulated amount of other comprehensive income items in the current and prior periods.

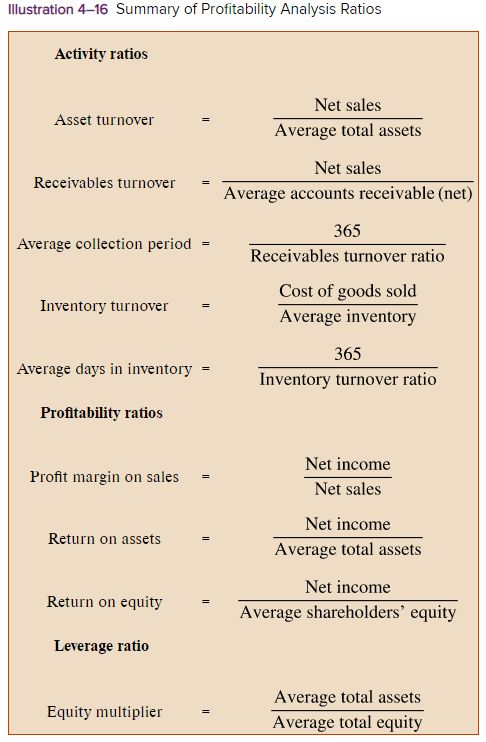

- Profitability Analysis

- Activity ratios

Anmerkungen:

- Measure a company's efficiency in managing its assets

- The greater the # of times an asset turns over, the fewer assets that are required to maintain a given level of activity (revenue). Therefore, high turnover ratios are preferred.

- Asset

turnover

Anmerkungen:

- Measure of a company's efficiency in using assets to generate revenues

- Receivables

turnover

Anmerkungen:

- Indicates how quickly a company is able to collect its accounts receivable; shows the number of times during a period that the average accounts receivable balance is collected

- Average

collection period

Anmerkungen:

- Indication of the average age of accounts receivable

- Inventory

turnover

Anmerkungen:

- Measures a company's efficiency in managing its investment in inventory.

- A high ratio indicates comparative strength, perhaps caused by a company's superior sales force or maybe a successful advertising campaign. However, it might also be caused by relatively low inventory level, which could mean either very efficient inventory management or stockouts and lost sales in the future.

- Average days

in inventory

Anmerkungen:

- Indicates the average number of days it normally takes to sell inventory

- Profitability ratios

Anmerkungen:

- Attempt to measure a company's ability to earn an adequate return relative to sales or resources devoted to operations

- Notice that for all of the profitability ratios, our numerator is net income. To enhance predictive value, analysts often adjust net income in these ratios to separate a company's temporary earnings from its permanent earnings.

- Profit margin

on sales

Anmerkungen:

- Measures the amount of net income achieved per sales dollar; indicates the portion of each dollar of revenue that is available after all expenses have been covered

- Return on assets

(ROA)

Anmerkungen:

- A company's profitability in relation to overall resources, measured as net income divided by average total assets

- Return on equity

(ROE)

Anmerkungen:

- Amount of profit management can generate from shareholders' equity

- DuPont framework

Anmerkungen:

- Depicts return on equity as determined by profit margin (representing profitability), asset turnover (representing efficiency), and the equity multiplier (representing leverage)

- Activity ratios

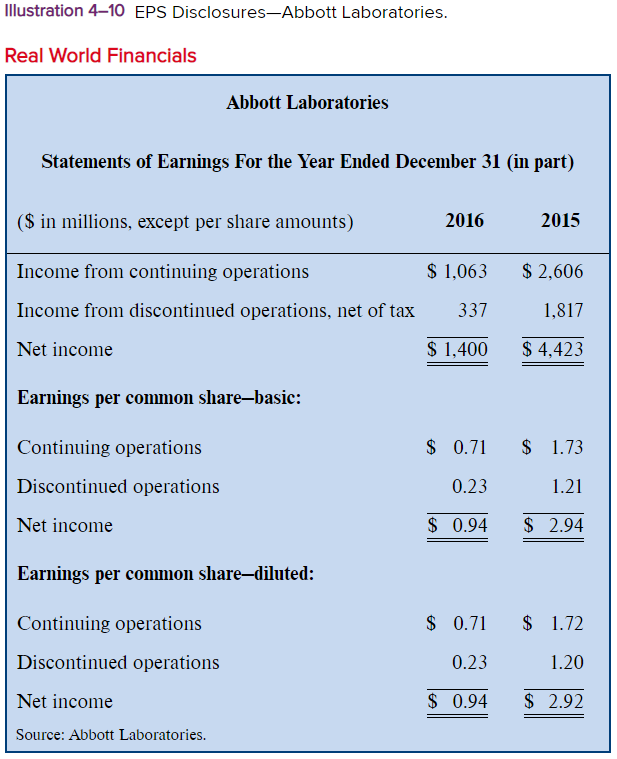

- Earnings per Share (EPS)

Anmerkungen:

- EPS provides a convenient way for investors to link the company's profitability to the value of an individual share of ownership. It also makes it easier to compare the performance of the company over time or with other companies.

- Basic EPS

Anmerkungen:

- Computed by dividing income available to common stockholders (net income less any preferred stock dividends) by the weighted-average number of common shares outstanding for the period

- Dividends to preferred shareholders are subtracted from net income in the numerator because those dividends are distributions of the company not available to common shareholders.

- The denominator is the weighted-average number of common shares outstanding because the goal is to relate for performance for the period to the shares that were in place throughout that period.

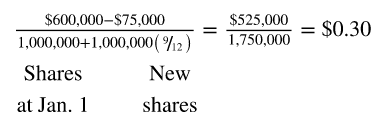

- (Net income - preferred stock dividends)

/ (Weighted-average outstanding

common stock shares)

- Diluted EPS

Anmerkungen:

- Incorporates the dilutive effect of all potential common shares in the calculation of EPS.

- Dilution refers to the reduction in EPS that occurs as the number of common shares outstanding increases.

- Takes into account ALL convertible

securities (e.g., convertible bonds

or convertible preferred stock)

Medienanhänge

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Möchten Sie kostenlos Ihre eigenen Mindmaps mit GoConqr erstellen? Mehr erfahren.