Beschreibung

|

|

Erstellt von grethe sinke

vor etwa 4 Jahre

|

|

Seite 1

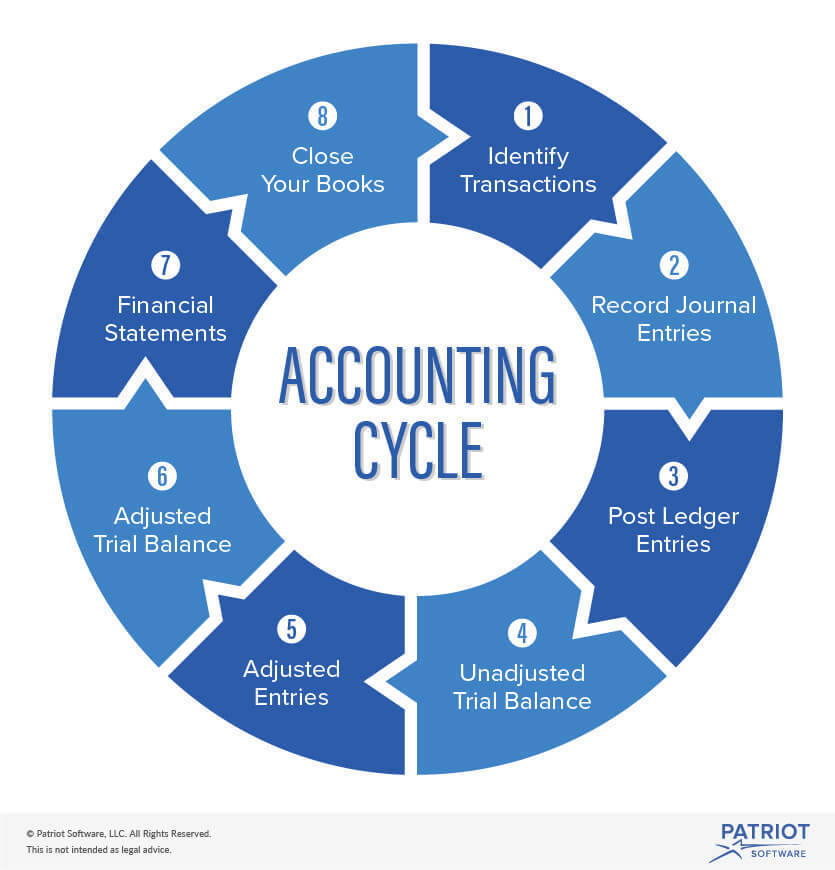

Financial accounting

Bookkeeping cycle (e.g. 2019) ginning opening balance sheet; Business transactions; Journal (translation transactions); General ledgers (grootboekrekeningen); income statement (2020) Balance sheet

{kind=link}

(possible) Literature

NHL Stenden

Seite 2

Managerial accounting

- Income statement - Budgeting and variance analysis - Pricing elasticity basic & rooms pricing - Pricing kinds of elasticity and pricing strategies - Break-even analysis - Cost analysis - Financial analysis techniques

(possible) Literature

Basic management accounting for the hospitality (3, 6, 7, 9, 10, 11, 14)

Seite 3

Income statement

= Profit and loss statement or statement of earnings/ income/ operations = Company's Financial Performance

USALI- Uniform System of Accounting for Lodging Industry 1. Revenues minus 2. Direct operating expenses (variable costs of sales and other variable operating expenses) ------------------------------------------------------------------------------------------------------------------------------- equals Departmental operating income/ profit (contribution margin) minus 3. Overhead expenses (undistributed operating expenses) ------------------------------------------------------------------------------------------------------------------------------ equals Net income (profit)

USALI Format 1. Departmental sales -- 2. Operating expenses (directly linked to department) ------------------------------------------------------------------------------------------------------------------- = Departmental profit (rooms + F&B + other) -- 3. Undistributed operating expenses ( = overhead) ------------------------------------------------------------------------------------------------------------------- = Gross operating profit (G.O.P.) -- 4. Fixed charges (fixed amount per period & related to production capacity) -------------------------------------------------------------------------------------------------------------------- = Net profit (before taxes)

{kind=link}

Example

{kind=link}

Departmental income rooms (departmental profit) = Revenue of rooms (departmental sales) - operating expenses rooms Gross profit F&B = Food and beverage revenues (departmental sales) - cost of F&B sales (cost of sales) Departmental income F&B (departmental profit) = Food and beverage revenues (department sales) - Operating expenses F&B Gross operating profit (G.O.P.) = Departmental profits F&B and rooms - Undistributed operating expenses (overhead) Overall income (Net profit) = G.O.P - fixed charges

Seite 4

Income statement II

1. Operating revenues: = the amount of assets created by the hospitality operation during normal business activities = p x q (price x amount) Sales, minus all sales discounts, returns, allowances

Expenses = (v x q) + f = ((variable costs x goods sold) + fixed costs)

2. Direct operating expenses: = the amount of assets consumed from the performance during normal business activities Cost of good sales 1. Beginning inventory plus 2. Inventory purchases equals Goods available for sale ----------------------------------------------------------------------------------------------------------------------------- minus 3. Ending inventory equals Costs of goods consumed ------------------------------------------------------------------------------------------------------------------------------ minus 4. Goods used internally equals Costs of goods sold Payroll and related expenses Other departmental expenses utilities, supplies, commissions, transportation, marketing, insurance, research and development, rents, interest, repairs and maintenance, depreciation and taxes;

3. Overhead expenses or undistributed operating expenses Administrative and general expenses (GM and accounting) Information and telecommunications systems expenses (ICT) Sales and marketing expenses Property and operations maintenance expenses Utility expenses Electricity, gas, oil, water, other fuels

Gross operating profit (G.O.P)

(4.) Non-operating: = Not generated to revenue, customers are not aware of these activities, = Gains and losses from other than its primary business activities Non-operating income (interest income); Rents (land and buildings); Property and other taxes; Insurance; Other expenses (cost recovery);

4. Fixed expanses (non-operating)

Net profit Revenue > expenses = profit Revenue < expenses = loss

Seite 5

Terms

Direct = Located to a specific department Indirect = Not located to a specific department (overhead) Overhead = Indirect or undistributed Fixed = Fixed amount every period (rent) Variable = Amount that changes as sales changes e.g. more rooms are sold which requires more cleaning Gross profit = Departmental sales - cost of sales = Bruto winst e.g. 10 euro cost of food, menu price of 20 euro = 10 euro gross profit Depreciation = Is to be found on an income statement and is always fixed Accumulated depreciation = Is to be found on a balance sheet Utility = gas, water, electricity Turnover = Revenue Operating = Generated to revenue (sales F&B, salary) Non-operating = Not generated to revenue (maintenance) Sales = p x q Costs = (c x q) + f Cost effect = (BC (Budget costs) - AC (actual costs)) x AQ (actual quantity) sales: (AP - BP) x AQ Quantity effect = (BQ (budget quantity) - AQ (actual quantity)) x BC (budget costs) sales: (AQ - BQ) x BP

Seite 6

Budgeting and variance analysis

Budget = the expected revenues and expenses for next year for: Planning Cost control Co-ordination Performance evaluation Knowledge if profit will be made next year Variance analysis = Difference between 'real world' (actual sales and/ or costs) and budget In Sales, a difference can either be in price or in quantity Higher actual prices and quantities are favourable In Costs, a difference can either be in costs or in quantity Lower actual costs and quantities are favourable

Example

Budget in costs of labour: 2900 euros for 58 hours and 50 euro/ hour Actual week: 2805 euros for 55 hours and 51 euro/ hour -95 euros difference (51-50) x 55 = 55 euros, unfavourable (BC (Budget costs) - AC (actual costs) x AQ (actual quantity) = Cost effect (58-55) x 50 = 150 euros, favourable (BQ (budget quantity) - AQ (actual quantity)) x BC (budget costs) = Quantity effect = (+) 95 euros favourable budget variance

{kind=link}

Seite 7

Pricing elasticity basic and room pricing

Major grounds for pricing 1. Product Nature of product Elastic: luxury goods Inelastic: goods of necessity Time Inelastic: short term increase does not/ has little effect on demand (the need for fuel) Elastic: long term increase affects demand (electric cars) 2. Competition Substitutes Elastic: substitutes are available Inelastic: no substitutes are available Cross elasticity of demand = %ΔQ of product X (wheat) / %ΔP (rice) Negative elasticity: two products are complements Positive elasticity: two products are substitutes Zero elasticity: products have no relationship Use of product Elastic: decrease in price affects usage in the product (multi-purpose) Inelastic: an increase in price will restrict the use of urgent/ minimal purposes 3. Customers Habits and loyalty Income Inelastic: a small proportion of income is spent on good Income elasticity of demand = %Δ quantity demanded / %Δ income

Price elasticity

Price elasticity = Relative change in quantity as a component = Ed = %ΔQ / %ΔP (relative quantity change/ relative price change) = normally negative (-) due to decrease in quantity when price increases Relative quantity change = (quantity difference: new - old)/ old quantity x100% Relative price change = (price difference) / old price x100%

Perfect inelasticity (medicine): Ed = 0 Whatever changes affect the price, the demand is not affected. Relative Inelasticity (cigarettes): -1 < Ed < 0 The relative change in the quantity demanded is less than the relative change in the price. Unit elasticity: Ed = -1 The relative change in the quantity demanded is exactly equal to the relative change in the price. Elastic demand: Ed < -1 Perfect elasticity: Ed = -∞ The change in quantity demanded is slightly higher than the change in price. Relative elasticity: -∞< Ed < -1 The change in quantity demanded is infinitely higher than the change in price - the slightest change in price would lead to an infinite change in quantity demanded.

Example

Exercise 1 Hotel A is unhappy with occupancy rate. It wants to get more customers with lower price. Hotels lowers price from 80,- to 72,-. Quantity changes from 100 to 105. Calculate price elasticity: Is demand price elastic? (price): (72-80)/ 80 x 100% = -10% (quantity): (105-100)/ 100 x 100% = 5% Ed = 5/-10 = -0,5 Price elasticity is inelastic Exercise 2 Hotel B is happy with nr of guests. The 100 room hotel is selling 90 on average per night. Hotel B wants to invest and considers higher price as a good option. It raises selling price from 70 to 77. New occupancy rate 72%. Calculate price elasticity. Is demand price elastic? (price) (77-70)/ 70 x 100% = 10% (quantity) (72-90)/ 90 x 100% = -20% Ed = -20/10 = -2 Price elasticity is elastic

Room pricing

1. Rule of thousand approach 2. Bottom-up approach 3. Relative room size approach

Möchten Sie kostenlos Ihre eigenen Notizen mit GoConqr erstellen? Mehr erfahren.