3382670

Beschreibung

Karteikarten von Nkolika Ezepue, aktualisiert more than 1 year ago

|

|

Erstellt von Nkolika Ezepue

vor mehr als 9 Jahre

|

|

| Frage | Antworten |

| What are the BRIC countries? | The BRIC countries (Brazil, Russia, India and China) are the countries that are deemed to be at the same stage of newly advanced economic development. |

| What is natural science? give examples | Objects, phenomena, laws of nature and the physical world. E.g. Chemistry, Biology and Physics. |

| What is social science? Give examples. | Study of human society and of individual relationships in and to society. E.g. Sociology, politics |

| What are the steps of applying science to economics? | Identify the issue Gather data Hypothesis Test out hypothesis Does the data agree? No-go back to hypothesis and amend or reject |

| What are hard laws? | Hard laws are theories that always apply e.g. E=MC^2 |

| What are soft laws? | Soft laws are theories that should apply but has exceptions. Economic theories are soft laws. E.g. if taxes increase, demand will fall- exceptions: if the product is a necessity. |

| What are positive statements? | The study of propositions which can be proved or disproved by data from the real world. They concern facts, truth can be scientifically tested e.g. the NHS employs more than 1 million workers |

| What are normative statements? | Statement that includes a value judgement and cannot be refuted just by looking at evidence often includes words "ought" and "should" e.g. The UK should spend more on education. |

| What is a budget deficit? think of two ways to solve this | When the government spends more than it receives. They could increase taxes or reduce taxes but cut benefits. |

| What are economic decisions frequently influenced by? | Value (whether something is desirable or nah), political and moral judgements. |

| What are the stages of economic stability/ financial security? | satisfying people's needs and wants-economic welfare (economic wellbeing)- should improve people's overall WELFARE (human happiness). Although much more to happiness than just material goods such as quality of life factors- pleasure gained from friends and family |

| What are factors of production? | Economic term to describe the inputs that are used in the production process of goods/services in the attempt to make an economic profit. The factors are LAND LABOUR CAPITAL ENTERPRISE |

| What is land and what is the payment for their use? | Land refers to minerals and natural resources we take from the earth e.g. fish, forestry and air. The payment is rent. |

| What is labour and what is the payment made for its use? | Labour is the potential workforce, but includes not just the actual person but their skills, abilities and intelligence. The payment is wages. |

| What is capital and what is the payment for their use? | Capital is the stock of goods used to make other goods and services e.g. machines, factories (producer goods). The payment or reward is interest. |

| What is enterprise and what is the payment made for it? | Enterprise refers to risk takers who are prepared to combine other factors of production for personal gain, and to produce particular goods and services. The payment or reward is profit. |

| What are consumer goods? | Consumed by individuals or households to satisfy own needs and wants. |

| How does the factors of production affect overall output? | An increase in improvement of any of the factors of production, the higher the ability of the economy to make goods/services (MORE OUTPUT) |

| What are zero hour contracts? | Allows employers to hire staff with no guarantee of work. This means employees only work when they are needed by employers, often at short notice. Their pay depends on how many hours they work. |

| Give 2 advantages of zero hour contracts | Employers only pay staff when they are needed Young people prefer this- less commitment to work. |

| Give 2 disadvantages of zero hour contracts | Older people with families- financial unstability due to flunctuations in income. People cant get a mortgage. |

| What is the economic problem and what has to be made in order to approach the situation? | People virtually have unlimited wants however resources are scarce and finite. As a result a choice has to be made (trade off). |

| What is a trade off? | Where the selection of one choice leads to the loss of another. |

| What 3 major problems do societies need to resolve? | How to produce goods To whom should they produce it for What to produce |

| Give 3 reasons why demand for NHS is increasing | Growing and ageing population Increasing customer expectations Growth in treatments and medicines available |

| What are possible solutions to this? | Limit number of people (reduce demand), buy more finance (gov have to increase taxes), privatise it (poor people...), education investment (takes time) |

| What is the opportunity cost? | The next best alternative forgone when taking a particular course of action. |

| What is 'ceteris paribus'? | Latin phrase meaning "all other factors remaining constant". All other variables except those in immediate consideration, are constant. |

| What are economic systems? | Institutional means for resolving the economic problems or resource allocation in an economy. |

| What are the 3 economic systems? | Planned economy, mixed economy, market economy |

| What is planned economy? | An economy in which production, investment, prices and income are determined by the government. Examples include, China, Cuba and North Korea. |

| What is market economy? | An economy in which decisions regarding production, investment and distribution are based on supply and demand- prices are determined in a free price system, with minimal state intervention. e.g. Mexico UK Canada |

| What are mixed economies? | Resource allocation is undertaken by state planning and market forces depending on the product. E.g. USA Norway Sweden |

| What does laissez-faire mean? | A part of market economy- gov doesnt interfere with the functioning of markets. |

| What is behavioural economics? | method of economic analysis that applies psychological insights into human behaviour to explain economic decision making. It explores why people sometimes make irrational decisions |

| What are capital goods? | Stock of goods used to produce other goods or services e.g. machinery, factories. |

| What are consumer goods? | goods consumed by individuals to satisfy their own needs and wants. |

| What are the top 5 highest populations? | China, India, USA, Indonesia,Brazil |

| What does a ppf show? | The maximum possible output combinations of capital and consumer goods an economy can achieve when all resources are fully and efficiently employed. |

| What does the line represent? | maximum capacity |

| What does it mean if an economy is producing goods on the ppf line? | Shows it has reached maximum capacity, its shows productive efficiency |

| What other things can a ppf diagram show? | Micro: illustrates scarcity, choice, opportunity cost, and productive efficiency Macro: economic growth, full employment and unemployment |

| Give causes of shifts outwards in the ppf | Higher productivity/efficiency of factor inputs better management of factor inputs- reduces waste and improves quality increase in the stock of capital and labour supply Innovation and invention of new products and resources discovery of new natural resources |

| What could cause an inward shift of the ppf line? | Damaging effects of natural disasters Loss of factor inputs by civil war and other forms of conflict Large scale net outward labour migration e.g. due to an economic depression that leads to a brain drain of skilled workers A trend decline in productivity perhaps caused by a persistent recession |

| What is productive efficiency? | An economy: It is impossible to produce more of one good without reducing output of another. A firm: All total costs of production is minimised |

| What is allocative efficiency? | Resources used to produce goods and services that best matches people's tastes and preferences |

| Describe markets | -Voluntary meeting of buyers and sellers-exchange goods and services -Do not have to exist in a particular location -Some markets are global (oil) |

| What do we mean by a competitive market? | -Large numbers of buyers and sellers (choice) -It's easy for new buyers and sellers to enter the market (low barriers to entry and exit) -Buyers and sellers can quickly find out what everyone is doing (transparency) |

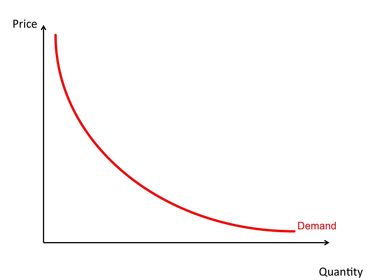

| Finish the sentence: in economics, demand has to be... | effective demand: demand is backed up by the ability to pay for it. |

| What is market demand? | quantity of a good or service that consumers or willing and able to buy at different market prices |

| BRUH | |

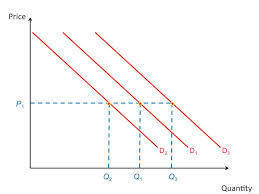

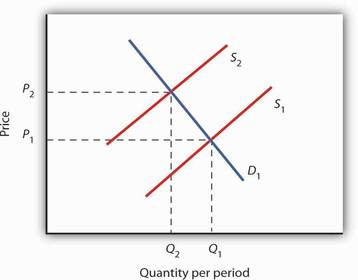

| Increases in demand... | the demand curve shifts the right D1 to D2 |

| At price P1 the quantity demanded... | has risen from Q1 to Q2 |

| Decreases in demand... | demand curve shifts to the left, from D1 to D3 |

| At price P1, the quantity demanded | has fallen from Q1 to Q3 |

| What might cause the demand curve to shift? | Taste and preferences Changes in population size Price of other goods and services weather conditions uncertainty of future prices prices of substitutes and complementary products |

| What are normal goods? | Goods where an increase in demand arises from an increase in disposable incomes- directly proportional |

| What are inferior goods, give an example | Demand falls as income rises and increases as income falls- inversely proportional. Consumers of inferior goods "trade up" to higher priced goods as they can afford it. So used cars demand will fall as they buy more prestige cars. |

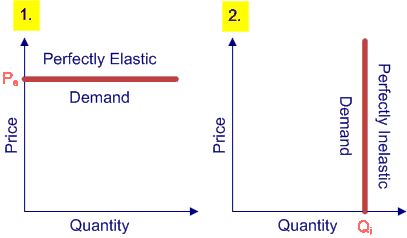

| perfectly elastic- demand is infinity completely inelastic- PED=0 | |

| PED>1 | |

| ped<1 | |

| PED=1 | |

| What is the law of demand? | As price fall, the quantity demanded expands and as prices rise the demand contracts.- a movement along the demand curve. |

| What is price elasticity of demand? | The measurement of the responsiveness of demand to a change in price. |

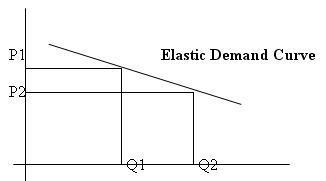

| Elastic? | Change in price, results to a larger change in demand. PED= greater than 1 |

| Inelastic? | Change in price, results to a smaller change in demand. PED= less than 1 |

| What determines elasticity? | - lots of substitutes= more elastic (people likely to switch) -Relatively cheap (insignificant expenditure)=less elastic -Necessity or luxury - Width of market definition e.g. demand for petrol is inelastic but demand for particular oil company's petrol e.g. shell is elastic -Time- longer the time period, usually the higher the elasticity. |

| How can consumer behaviourisms affect the elasticity? | Consumers may be ignorant of alternative prices= less elastic e.g. the energy market May be difficult to change spending=less elastic e.g. signed contracts |

| The equation for PED? | PED= %CHANGE DEMAND/%CHANGE PRICE |

| What is income elasticity of demand (YED)? | A measurement of responsiveness of demand to a change in income. Normal G= demand rises as income rises(+ve YED) Inferior G= demand falls as income rises (-ve YED) inferior brands include home bargains and lidl |

| Positive>1= | normal good, elastic |

| positive<1 | normal good, inelastic |

| negative>1 | inferior, elastic |

| negative<1 | Inferior, inelastic |

| What are complementary products? | Goods or services that are consumed together e.g. DVDs and DVD Players |

| What are substitutes? | Goods or services that can be used as an alternative to another good or service. |

| What is cross elasticity of demand? | A measurement of responsiveness of demand for one product to changes in the price of another product. |

| XED= | =%change in quantity demanded of good x/%change in price of good y the greater the number the stronger the relationship. |

| Substitutes are always... | positive- an increase in the price of a product leads to an increase in demand for its substitute. |

| Complements are always... | negative- and increase in price of a product, leads to a fall in demand for its complement. |

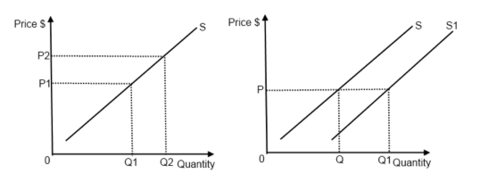

| What is the most important determinant of supply? | =price, higher prices means a higher profit which leads to increased supply (vice versa). Changes in price=movement along supply curve. |

| Why does the supply curve shift? | If there is a change in the conditions of supply |

| What factors cause a shift in the supply curve? | -costs of production change- wages, raw materials, energy, borrowing costs -Technical/productivity advances means lower cost per product- at same price more profit made -subsidies- reduces the cost to producer- increases ability to make profits |

| What is supply? | Quantity of a good or service that a firm is willing and able to buy at a given price in a time period |

| What is price elasticity of supply? | A measure of responsiveness of supply to a change in price |

| What factors affect elasticity of supply? | -Ease of accumulating stocks -Availability of spare capacity, labour and raw materials -Ability to switch production from other products-more elastic -Ability of new firms to enter the market -Length of production period and time |

| Give 3 reasons why elasticity of supply increases over time | -The suppliers may not be willing or able to change quickly -The may wait to see if price change is temporary -May take time to obtain/reduce resources required. |

| If prices of oil rose there would be a little increase in supply (inelastic) because... | the discovery, tapping and exploration of new oil reserves take a long time Extremely expensive market to enter |

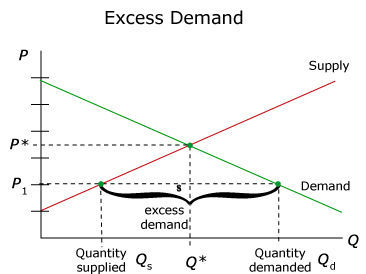

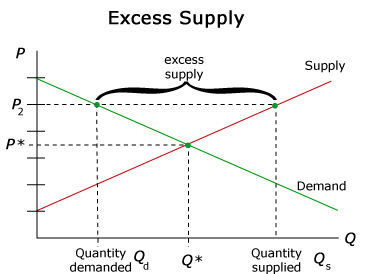

| What is the equilibrium price? | Price at which planned demand for a good or service equals to planned supply |

| What is disequilibrium? | Situation in a market where there is excess supply or excess demand |

| What is excess supply? | Firms wish to sell more than consumers wish to buy, with the price above equilibrium price |

| What is excess demand? | When demand exceeds supply. Price below equilibrium price. |

| What is joint supply? | For complementary good, when one good is produced, another good is also produced from the same raw material e.g. beef and leather. A rise in demand for one product leads to a rise in the supply of another. |

| What is composite demand? | demand for a good which has more than one use. An increase in the demand for one purpose reduces available supply for other purposes. (raising the price). |

| What is derived demand? | Demand for a good which is an input into the production of another good. e.g. higher demand for cars come from higher demand from iron ore. |

| what is competing supply? | For substitute good, when raw material can be used to produce one good they cannot be used to produce another good |

| Does price affect substitutes? | If the price of a product is raised or lowered this will increase or decrease the demand for its substitutes. Similarly, if the price is altered this will alter the demand for its complements. |

| What is productivity? | Output per unit of input |

| What are different measurements of productivity? | - labour productivity- most common measure (output per worker) = total output per time period/number of workers -Capital productivity (output per unit of capital) |

| What are advantages of higher productivity? | - Lower average costs (cost per unit) which should lead to: -More internationally competitive -Greater profits -Rise in real wages- firms willing and able to pay more -Economic growth- ability to push out ppf if you can get more out of factor inputs |

| What is the division of labour? | Where the production of a good is broken into many separate tasks each performed by different people. |

| What are the benefits of division of labour? | -Become more skilled and specialised in what they're good at- more quality -Less wasted time (changing equipment, moving) -requires less duplication of capital equipment. |

| What are the downsides? | -Boredom -Alienation from the process can result in workers taking less pride in their work -one machine breaking/ a fault could stop entire production. |

| What is specialisation? | A worker only performing one task in a narrow range of tasks. Also, different firms specialising in producing different goods or services. |

| What is our main medium of exchange? | Money- allows buying and selling of services |

| What is bartering and what is the problem with is? | Bartering is the exchange of goods and service without the involvement of money. It allows specialisation but it relies on the coincidence of wants. |

| What is short run? | The time period where at least one factor of production is fixed |

| What is long run? | The time period when no factors of production are fixed, they can all be changed. |

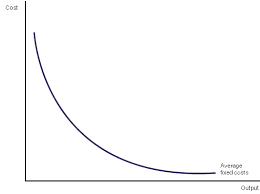

| What are fixed costs and variable costs? | Fixed costs- costs which in the short run, do not vary as output changes variable costs- Costs that vary with output, even in the short run. |

| How do you work out total cost, average total cost? | TC=TFC+TVC ATC=TC/number of output units ATC= AFC+AVC |

| What is the average cost curve shape, and why is it like that? | As company increases its output, the fixed costs stay the same. AFC=FC/OUTPUT. If the FC stays the same but output rises then AFC falls. |

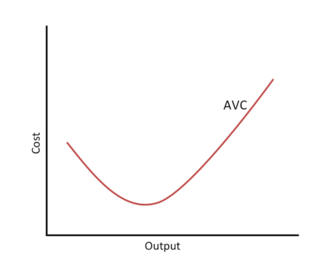

| What is the shape of the AVC and why is it like that? | When firm first employs workers increasing the division of labour and specialisation means productivity increases. However, workers start getting into each other way and productivity decreases. |

| What is economies of scale? | Benefits of producing on a large scale. The reduction of average costs of output. |

| What are the types of economies of scale? | -Technical economies -Marketing economies -managerial economies -Financial economies -Buying/purchasing economies -Risk bearing economies |

| How does technical economies work? | -Can invest in more advanced machinery, increased specialisation of workforce, law of increased dimensions, invest in R&D, greater utilisation of capital equipment |

| How does marketing and managerial economies work? | Marketing- advertising and marketing budget is spread over a larger output Managerial- Larger firms can employ specialist managers who raise productivity and reduce cost per unit |

| How does Financial economies work? | -Bigger companies can raise greater amounts of finance and at lower rates of interest. They are usually rated as less risky and thus more credit worthy. -PLCs can raise huge amounts by selling shares on the stock exchange (cheaper form of finance than loans) |

| How does purchasing economies and risk bearing economies work? | Purchasing- buying in bulk at lower prices Risk bearing- larger companies more able to spread risks by diversifying in products, markets and suppliers |

| What is diseconomies of scale? | The cost per unit rises as companies produce on a larger scale. The disadvantages that arise from companies producing on a large scale. |

| What are the causes of diseconomies of scale? | Control- monitoring quality and productivity in a big company is hard and costly Coordination- flows difficult to manage, production processes and info, dealing with lots of suppliers is hard cooperation- workers may feel alienated- motivation and productivity decreases |

| What are external economies of scale? | Lower average costs caused by the expansion of a particular industry rather than an individual firm. Often associated with clustering e.g. silicon valley |

| What are the benefits of clustering/ external economies of scale? | -skilled labour growth -specialised suppliers of raw materials, equipment, and capital goods -specialised services such as banking, insurance and education -improved infrastructure -good reputation |

| What is clustering? | business cluster is a geographic concentration of interconnected businesses, suppliers, and associated institutions in a particular field. considered to increase the productivity with which companies can compete, nationally and globally |

| How can we compare markets? | -The number of firms in the market -How competitive the market is -How much product differentiation there is -How easy it is to enter the market, barriers to entry. |

| Compare hairdressing with banking | Hairdressing would have thousands more firms and more competition, its easier to change hairdressers and easier to enter that market. Banks make more profit. |

| What are the two main market structures? | Perfect competition (price takers) and Monopoly (price makers) |

| What are the characteristics/assumptions of perfect competition? | -Many suppliers (businesses) -individual firms too small to affect market price-price taker -Homogeneous products which are all perfect substitutes -Consumers and producers have complete info about products and prices -Each consumer is able to buy, and each producer able to sell as much as they wish at the ruling market price -NO barriers to entry and exit |

| Why are they so important? | -Model is a benchmark to compare market performance against. |

| Give 2 examples of prefect competition | -Chinese restaurants in Chinatown, London -Fruit sellers at a weekly local market |

| Why are prices low in a competitive market? | Lots of companies competing drives down prices and profits. Few barriers to entry and exit means high profits will attract more firms (raising supply and lowering prices) which will lower profits. |

| What are the objectives of firms? | -Profit maximisation e.g. Amazon tax avoidance -Growth maximisation e.g. Lidl and Aldi -Sales/revenue maximisation e.g. Banks pre credit crunch -Market share maximisation- Tesco -Survival e.g. smaller companies-HMV |

| What are concentrated markets and give examples | -Has fewer firms -e.g. chocolate banks, insurance, petrol Pure monopoly like Yorkshire water is an extreme example of this. Everything but perfect competition is imperfect competition. |

| What does it mean to have monopoly power? | The ability to dominate the market, the power to act as a price maker not a price taker. In the UK the CMA deems any firm with greater that 25% market share to have a monopoly |

| Give 3 types of monopolies | -Geographical location- local population doesn't support more than 1 business -Natural monopoly- market suits one provider due to huge economies of scale -Government created monopoly- may be done through issuing licences and patents |

| What are natural monopolies in detail? | -In some markets the economies of scale so great that one firm can reach productively efficient point. One firm can produce as much lower costs than 2 companies due to the economies of scale. |

| What are some drawbacks of monopolies? | -Monopolies have the power to raise prices by restricting supply -High prices mean that consumers buy less of a product they would have- reduces economic welfare- resource misallocation e.g. high energy prices- elderly -lack of choice for consumer -monopolies may be productively inefficient |

| What are the 4 factors that influence how much monopoly power a business has? | 1. Barriers to entry 2. Number of competitors 3. Advertising 4. Product differentiation |

| What do you mean by barriers to entry? | There is natural (innocent) barriers- existing firms benefit from significant economies of scale due to size. New entrants would have high ATC- not able to compete Artficial/strategic (man made) barriers- deliberate action by firms e.g. predatory pricing or patents |

| What do you mean by the number of competitors? | Generally the greater the number of competitors, the less likely that a firm would have monopoly power |

| What do you mean by advertising? | advertising can be used to create monopoly power in 2 ways: -can create brand loyalty e.g. clubcards preventing customers trying cheaper substitutes -Saturated advertising- may discourage smaller firms or new entrants e.g. soap and washing powder market |

| What do you mean by product differentiation? | Making the product different from other products (USP) will increase the monopoly power of a firm. This could be its design or functionality. |

| What are concentration ratios? | -Measures the combined market share of the largest firms in a particular market -Most common are 3,4,5- doesn't include "others" -Market dominated by a few firms is called an oligopoly. |

| What are benefits of monopolies? | -Monopolies benefit from huge economies of scale- may pass on lower prices to consumers. Depends on whether they want to do that though. -Can make large profit- incentive to carry out R&D- protect their monopoly position -consumers may benefit through greater invention and innovation |

| What do firms compete for? | -Lowest prices -Best products (quality, reliability, design) -customer service -location |

| What is the economic problem? | Scarcity due to limited resources and unlimited wants |

| How is this problem resolved in a market economy? | -The price mechanism |

| What are the 3 functions of price? | 1. Rationing function 2. Incentive function 3. Signalling function |

| What is the rationing function and give an example? | High prices ration (limit) the demand for a product or service e.g. petrol prices for cars |

| What is the incentive function and give an example? | High prices create an incentive for producers to increase supply. They also incentivise consumers to seek alternative options. e.g. high oil prices |

| What is the signalling function? | high prices indicate potential profits for producers and thus send a signal to firms to increase output or for new firms to enter the market. High prices also sends out a signal for consumers to cut back their demand for a good/service. |

| What do we mean by market failure and give an example? | When the market mechanism leads to a misallocation of resources. e.g. binge drinking |

| What are the 2 types of market failure? | 1. Complete market failure- no market for a good is provided (missing market) e.g. free market unable to charge for street lights 2. Partial market failure- market does not allocate resources in a way that maximises social welfare e.g. fly-tipping, individuals under valuing education |

| What are private goods? | Good, such as an orange, that is excludable (not everyone benefits) and rival (once consumed no one else can consume). e.g. can of coke, education |

| What are public goods? | Good, such as a streetlight, that is non-excludable and non-rival. |

| Why does the government tend to provide public goods? | Because if left to the market there would be complete market failure- no firm would provide the good (missing market) because it's hard to make a profit- free rider problem e.g. firework display |

| What is a quasi-public good? | Good which is not fully non-rival and/or where It is possible to exclude people from consuming the product. e.g. beaches, parks. You can make a quasi public good excludable e.g. roads. |

| What is an externality? | Effects of economic activity on third parties, who are not involved and have no say in the economic activity taking place. They can be positive or negative, and they can be created by either production or consumption. An example of market failure. |

| What are positive externalities? | Benefits to the third party arising from the manufacturing or provision of a good or service. The social benefit is greater than the private benefit. |

| What are negative externalities? | Costs to the third party arising from the manufacturing and provision of a good or service. e.g. can be noise pollution, bad landscape, congestion etc. Social cost greater than the private cost. |

| What is a production externality? | An externality (which may be positive or negative) generated in the course of producing a good or service. |

| Give an example of a negative production externality | -ve: pollution in a power station- these externalities aren't part of the real costs so the energy is under priced- allocative function has broken down- over consumption of energy and over production. |

| Give an example of a +ve production externality | +ve: power station discharges warm water to the lake nearby, increasing fish stocks so commercial fishing boats benefit. |

| What is a consumption externality? | An externality (which may be positive or negative) generated in the course of consuming a good/service. +ve e.g: view of a flower garden -ve e.g.: Litter |

| Negative production externality: real costs aren't reflected- should be higher so supply should be less. It's too cheap and over-produced. | |

| Positive production externality: Costs to the consumer should be higher so supply should be higher. Its too expensive and under-produced. | |

| What are social benefits? | The total benefit of an activity, including external as well as private benefits. Social benefit= private +external |

| What are merit goods? | A good, such as healthcare and education, for which the social benefits of consumption exceed the private benefits. Value judgement is involved in deciding that a good is a merit good. They are private goods |

| Merit goods are under-provided and consumed because consumers only consider the benefits to themselves. Not the wider benefits to society. Too few resources are allocated to the production and consumption of merit goods = partial market failure. | |

| What are demerit goods? | A good, such as tobacco, for which the social costs of consumption exceed the private costs. Valued judgements are involved in deciding that a good is a demerit good. |

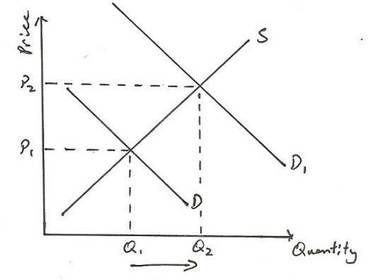

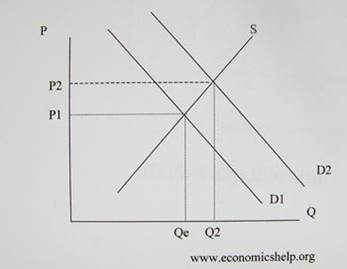

| How do you show demerit goods on a diagram? The consumer over-estimates the good- willing to pay p2 etc. but in natural fact, if they took to account the real benefits, demand will fall to D1 | |

| Why might it not be so straight forward to deem a good as a merit or demerit good? | -Can be based on the value judgements of the individual-subjectivity -May be linked into their religion e.g. contraception and abortion. |

| What do some economists argue the cause is for the over consumption of demerit goods and the under consumption of merit goods? | The information problem- occurs when people make wrong decisions because they don't possess or they ignore relevant information. Very often, they are myopic (short sighted) about the future. |

| What is the root issue with the response of consumers to merit goods? | Only consider the short term costs and benefits |

| What is the root issue with response of consumers to demerit goods? | They under-value and under-estimate the long term costs of their actions e.g. effects of drinking fizzy drinks |

| What are private costs/benefits? | costs/benefits of an activity to an individual or firm |

| What are social costs/benefits? | costs/benefits to the individual, firm but also the rest of society (third parties) that arise from an activity. |

| In what situation would you get positive or negative externalities? | negative externalities arise when the social cost Is greater than the private costs and positive externalities arise when the social benefits is greater than the private benefits. |

| How can monopolies lead to market failure? | Monopolies have the power to restrict supply which raises prices to the consumer- consumer exploitation. As a result, people may not buy as much of the good as they intended to leading to a misallocation of resources. |

| What is immobility of labour? | the inability of labour to move from one job to another either for occupational reasons (e.g. need for training) or geographical reasons (e.g. the cost to move to another country) |

| What is geographical immobility of labour? | Occurs when workers find it difficult or impossible to move to another job in other part of the country or in other countries for reasons like higher housing costs in locations where the job exists, family and social ties, difference in general cost of living |

| How can it be reduced? | Reforms to the housing market designed to improve the supply and reduce the price of rented properties and to increase the supply of affordable properties Specific subsidies for people moving into areas where there are shortages of labour – for example teachers and workers in the National Health Services |

| What is occupational immobility of labour? | Occurs when workers find it difficult or impossible to move between jobs because they lack or cannot develop the skills required for the new jobs. All these causes of immobility of labour leads to unemployment and a waste of scarce resources, and contributes to market failure in factor markets. |

| What is equity? | Fairness or justness |

| What is the distribution of income and wealth? | The way in which distribution and wealth are divided among the population . |

| How can this lead to market failure? | Free markets may result in an inequitable allocation of resources. Some unable to access goods or services consumed by the average citizen. Encourages alienation and crime with wider negative consequences for the rest of society. |

| What are free marker economists? | Believes the market and price mechanism leads to the best allocation of resources. The role of the government is to ensure markets are competitive and then to leave them alone- laissez faire. |

| What are interventionist economists? | Believe that if left alone markets too frequently result In market failure. They intend to counter disestablishing forces such as uncertainty about the future and info failure. The role of the government is to intervene to minimise this. |

| What is regulation? | Involves the imposition of rules, controls and constraints, which restrict freedom of economic action in the market place. Aims to restrict the consumption/production of goods or services which produce negative externalities. |

| How does regulation be used as a source of government intervention to correct market failures? | Regulation directly influences the quantity of an externality that a firm or household can generate, and the level of consumption of a demerit good such as tobacco. |

| How does taxation be used as a source of government intervention to correct market failure? | Taxation adjusts the market price at which a good that generates the externality is sold, or the price of a demerit good. e.g. taxing pollution discharged by power stations creates an incentive for less pollution to be created, and taxing tobacco creates an incentive for lower consumption of it. |

| What is the 'polluter must pay' principle? | In environmental law, the polluter pays principle is enacted to make the party responsible for producing pollution responsible for paying for the damage done to the natural environment-internalising the externalities . |

| What is a tax? | A compulsory levy imposed by the government to pay for its activities. Taxes can also be used to achieve other objectives , such as reduced consumption of demerit goods. |

| What is the price ceiling and what problems does it cause? | It's below the free market price. It was introduced to tackle rents and it is the price above which it is illegal to trade. It leads to excess demand which leads to queues, waiting lists and possible black market. |

| What is price floor? | It is the price below which it is illegal to trade. They can distort markets by creating excess supply e.g. unemployment with minimum wage. |

| What is gov failure? | Occurs when government intervention reduces economic welfare, leading to an allocation of resources that is worse than the free- market outcome. |

| Give some sources of government failure | 1. Imperfect info- gov makes decisions based on wrong info e.g. with dairy 2. Conflicting objectives- action in pursuit of 1 objective may be at the detriment of another 3. Administrative costs- costs of gov bureaucracy can undermine benefits of gov intervention 4. Disincentive effects-gov intervention which reduces incentive for businesses to invest, make profit or for people to work |

| What are some other sources of government failure? | 5. Political decisions- gov decisions based on political considerations 6. Short-termism- most effective long term solution is rejected due to short term costs 7. Regulatory capture-Where the state acts in favour of producers to the detriment of the consumer 8. Law of unintended consequences- never expected or anticipated. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

0 Kommentare

Möchten Sie mit GoConqr kostenlos Ihre eigenen Karteikarten erstellen? Mehr erfahren.