6509635

Beschreibung

Karteikarten von Lucille Compton, aktualisiert more than 1 year ago

|

|

Erstellt von Lucille Compton

vor mehr als 8 Jahre

|

|

| Frage | Antworten |

| Users of Accounting Info | * Internal Owner Managers Employees * External Customer Competitors Lenders Government Suppliers Investment Analysis |

| What are the reasons for using accounting info? | Owners - Determine profitability and financial viability. Managers - Ensure business operates efficiently and solve problem areas. Employees - Determine if employer can provide stable employment and remunerations. Customers - Determine if business can provide products over long period. Competitors - To maintain the competitive edge. Lenders - Determine if business can repay a loan and the interest on it. Government - Determine how much tax and levies should be paid. Suppliers - Determine if business can pay for goods purchased on credit. Investment Analysis - Determine if business will be a good investment. |

| Describe the different types of Business Activities | * Service Businesses - Provide a service at a fee, e.g. hairdresser, attorney, etc. * Manufacturers - Buy raw materials and transforms it into finished products which are sold to wholesalers and retailers. * Wholesalers - AKA middleman. Buy in bulk from manufacturers and then sell in smaller quantities to retailers or the public. * Retailers - Buy goods from wholesalers or manufacturers and sell to the general public. |

| What is the financial manager's goal? | Manage the money of a business. Maximise the shareholders' wealth by increasing the value of the business. Value of organisation is measured as the difference between assets and debts. |

| Basic Accounting Equation (BAE) | Assets = Owners Equity (OE) + Liabilities |

| Definition of Accounting | * Gathering - bringing together of all financial info that has an effect on a specific business. * Analysing - determining how the financial info will affect the business. * Recording - inputting the financial info through proper accounting processes. * Reporting - summarising of all financial info for a given period so that it can be read and understood in a more condensed format. * Interpreting - preparing an analysis of the summarised reports to allow users to make informed decisions. |

| Qualitative Characteristics | * Comparability - the info must be comparable to the financial info presented by other organisations and also various accounting periods within the organisation, so that users can identify trends in the performance and financial position of the organisation. * Understandability - the info must be readily understandable by all users of financial statements. * Relevance - the info reported must be relevant to the needs of the users. This may involve reporting info that could influence the economic decisions of the users. * Reliability - the info must not be misleading and should be free of material error and bias. |

| Considerations before commencing a business | * The type of business activity * The entity form * The location of the business * Capital requirements |

| How wealthy are you? | Possessions - Debts = Wealth (net worth) |

| Assets | Economic resources. Anything tangible / intangible that is capable of being owned or controlled to produce value and has a positive economic value. Assets represent ownership of value that can be converted into cash. (cash also an asset) |

| Liabilities | Present obligations resulting from past events, the settlement of which leads to decreases in economic benefits. |

| Owner's Equity | Owner's interest in the business and comprises of capital contributions less drawings plus net profit. (Income - expenses = net profit) |

| Non-current Assets | Item of value with a lifespan of more than one year. - property, plant and equipment - financial assets (investments) - intangible assets (patents, trademarks) |

| Current Assets | Lifespan of less than one year. - cash - debtors - inventory |

| Non-current Liabilities | Obligations payable over more than one year. - long term loan - bond |

| Current Liabilities | Obligations payable within one year. - bank overdraft - creditors |

| Income | Receipts for normal operations. - sales - rent received - fees earned - interest received |

| Expenses | Amounts spent during normal operations. - rent paid - interest paid - advertising - salaries |

| Debit | D - Debit E - Expenses A - Assets D - Drawings |

| Credit | C - Credit L - Liabilities I - Income C - Capital Contributions |

| Going Concern Concept | Implies that the business will continue to operate for a long time and there is no intention to cease operations. |

| Matching Concept | Cost and revenue are matched to reflect the same time period. This concept is also known as the accruals concept. |

| Consistency Concept | Once a method has been chosen by the accountant to treat accounting entries, it is essential that the same method is applied in future years. This will ensure that statements can be compared over time. |

| Prudence Concept | Chose the most conservative option to deal with items, meaning when choosing an accounting method, select the method which has the least favourable effect on net income and the financial position. The prudence concept requires that estimates be conservative. AKA doctrine of conservatism. |

| Accounting Cycle | 1. Transaction occurs 2. Source documents 3. Journals 4. Posting to general ledger 5. Pre-adjustment trial balance 6. Adjustments 7. Post-adjustment trial balance 8. Closing entries 9. Final trial balance 10. Financial statements 11. Analysis and interpretation |

| Transactions | An agreement between two parties to make something happen. Cash is not necessarily involved in this occurrence. - buy - sell - pay - receive money - return goods - receive goods back |

| Source Documents | Under no circumstances may any entries be made in the records without a source document to substantiate the entry. A specific source document is used for every type of transaction. It is important to distinguish between an original and duplicate source document. - receipt for cash received - cash slip for cash sales of goods - invoice for credit purchases - credit note for goods returned |

| Journals | Purpose of journals is to summarise transactions of the same type. Distinction is made between cash and credit transactions. Further distinction of cash transactions, nl. cash payments and cash receipts. - general journal (GJ) - cash receipts journal (CRJ) - cash payments journal (CPJ) - debtors' journal (DJ) or sales journal (SJ) - creditors' journal (CJ) or purchases journal (PJ) - debtors' allowance journal (DAJ) or sales returns journal (SRJ) - creditors' allowances journal (CAJ) or purchase returns journal (PRJ) - petty cash journal (PCJ) |

| General Ledger Accounts | When info is transferred from journals to GL, we use the term post. The purpose of the GL account is to determine a balance for each account. An account is opened for every item, be it an asset, liability, income or expense and the balance is determined for every account. Left side - debit; right side - credit. |

| Pre-adjustment trial balance | Summary of the debit and credit balances in the GL before any adjustments are made to the balances. Purpose it to ensure the transactions have been captures correctly. Debit and credit side must balance. |

| Adjustments | Adjustment is not a transaction - does not involve two parties. Adjustments are changes made at the end of a financial period. E.g. - depreciation - expenses prepaid - accrued expenses - accrued income - income received in advance - allowance for credit losses Adjustments are made in the GL and the journal description acts as the source document. |

| Post-adjustment Trial Balance | Is prepared after making all the necessary adjustments. Represents the final balances of all GL accounts and includes income, expense, asset, owner's equity and liability accounts. |

| Closing Entries | Entries are made using the general journal. All income and expense accounts are closed so that no balances remain on these accounts and a clean start can be made during the next financial year. Income and expense accounts that influence gross profit are closed off against the trading account, all other income and expense accounts are closed off against the profit and loss account. |

| Final Trial Balance | After all closing entries have been made the only balances that remain in the GL are assets, liabilities and the profit or loss as calculated in the profit and loss account. The final trial balance therefore consists of a summary of those closing balances that remain in the general ledger after ll the closing entries have been made. |

| Financial Statements | Financial statements of a business entity comprise five sections. - statement of profit or loss and other comprehensive income - statement of financial position - statement of changes in equity - statement of cash flow - notes |

| Analysis and Interpretation | Final step. Done by calculating ratios and comparing the figures in the financial statements with those of other concerns or with budgets that have been drawn up previously. |

| Perpetual method for accounting for stock | Gross profit = selling price - cost price |

| Periodic method of accounting for stock | Cost of sales = opening stock + purchases - closing stock |

| Year-end Adjustments | - Depreciation - Allowance for credit losses - Prepaid expense - Accrued expense - Accrued income - Income received in advance / prepaid income |

| Depreciation | By accepting that the life of a fixed asset is limited, the accounts of an organisation need to recognise the benefits of the fixed asset as it is "consumed" over several years. This consumption of a fixed asset if referred to as depreciation. |

| Methods of Depreciation | - Straight-line method - Reducing balance method - Utilisation method |

| Allowance for credit losses / Provision for doubtful debts | When sales are allowed on credit, the possibility exists that some of the debtors will not pay their outstanding debt. It is prudent that some provision for doubtful debt is created in order to give a more accurate report on the expected amount of outstanding debt, including a provision for doubtful debt. The amount provided for doubtful debt is estimated as a percentage of the total amount of debt outstanding and is based on past experience and the economic climate. |

| Prepaid expenses | Payments that you have made in one accounting period even though some of them are only due in the next accounting period. Even though the expense was made in full, only the part due for payment in the current accounting period should be matched to the income of the current accounting period. |

| Accrued expenses | Expenses that have been incurred in the current accounting period, but have not been paid for. These expenses have to be written off against the income of the current accounting period, even though they have not yet been paid. |

| Accrued income | Income that you have earned during the current accounting period, but have not yet received. This income must be recorded in full in the current accounting period, even though it has not yet been received. |

| Income received in advance | Income that you have received in advance (that is, before it is due). In terms of the matching principle only the income generated for the current accounting period should b recorded in the statement of profit or loss and other comprehensive income and the prepaid amount should be deferred or transferred to the next accounting period as a current liability in the statement of financial position. |

| Closing Process | 1. Close off the sales and cost of sales accounts to the trading account, in order to determine the gross profit for the period. 2. Transfer the gross profit calculated in the trading account to the profit and loss account. 3. Close off all the income and expense accounts to the profit and loss account, and determine the net profit or loss for the period. 4. The net profit is transferred to the capital account, since it belongs to the owner. |

| 5 Types of Profit Companies | - State owned company - Private company - Public company - Personal liability company - External company |

| Share Capital | Once a company has been formed, capital can be raised by issuing shares. We have what is known as authorised share capital and issued share capital. |

| Authorised Share Capital | This it the amount of share capital that the company is authorised to issue according to the CIPC. The authorised share capital must state specifically the types of share, e.g. preference or ordinary, and the number of shares, as well as the par value/nominal value of the shares. The company can issue all or only part of this capital as it wishes. |

| Issued Share Capital | This is the amount of the authorised share capital that the company has actually issued. |

| Share Premium | If the company has been making good profits, it may choose to issue shares for more than the nominal value. This extra money generated is known as the share premium. E.g. nominal value is R1 but the company issues the share for R1.5 each. The 50c is the share premium. This is seen as a capital profit on the sale of the shares. |

| Preference Shares | Holders receive a fixed rate dividend every year and have preferential rights over and above those of ordinary shareholders, that is, they must be paid their dividend first. These shareholders do not have voting rights. |

| Ordinary Shares | Holders do not receive a fixed dividend each year. The dividend received fluctuates according to the company's prosperity and dividend policy. The owners of these shares have voting rights and rank after preference shareholders for certain rights. |

| Reserves | The equity of a company consists of share capital and reserves. Reserves are essential profits that are retained within the business and can be used for expansion of the business. |

| Non-distributable Reserves | These reserves are non-trading profits which are not available for distribution to shareholders as a dividend. They are recorded in the financial statements as share capital and share premium. |

| Distributable Reserves | This refers predominantly to retained earnings. This figure is adjusted every year with that amount in the statement of comprehensive income that is not spent on expenses and dividends. |

| Profits, taxation, reserves and dividends | Companies are treated a separate legal entities and are therefore liable for taxation. Once the profits have been calculated, the first slice must go to the Receiver of Revenue in the form of taxation. Thereafter, profits are divided between reserves and dividends, with the remainder being retained in the company. Ordinary shareholders have not rights to profits. They only receive a share of the profits if the directors declare a dividend. |

| Income Statement (Statement of Comprehensive Income) | Measures the operating performance during a given accounting period. It reflects the normal operating transactions, and include losses or gains on the disposal of assets and other non-recurring and extraordinary events. Measures the income over a period. |

| Revenue | Measured at the fair value of the consideration received or receivable. Revenue is usually reduced for estimated customer returns, rebates and other similar allowances. |

| Cost of Sales (C.O.S.) | The expense a company incurred in order to manufacture, create, or buy inventory. It includes the purchase price of the raw material, as well as the expenses of turning it into a product. |

| C.O.S. Calculations - Trading Company | Opening Stock + Purchases + Other Charges (customs duty, freight, railage) - Closing Stock |

| C.O.S. Calculations - Manufacturing Company | Opening Stock + Manufacturing Labour + Raw Material + Manufacturing Overhead - Closing Stock |

| Gross Profit | The total revenue subtracted by the cost of generating that revenue. Tells you how much money a business would have made if it didn't pay any other expenses such as salary, general admin expenses and income taxes. |

| Investment Revenue | Comprises rental income earned through investment properties, and interest received earned through assets such as bank deposits. |

| Other Gains and Losses | # gain/loss on disposal of property, plant and equipment. # gain/loss on disposal of available-for-sale investments. # government grants received for staff re-training. # net foreign exchange gains/losses. # gain/loss arising on effective settlement of legal claims. |

| Distribution Expenses | Cost to the business when sending their finished goods out to customers and may also include payroll costs (salaries, commissions, and travel expenses of executives, sales people and employees), involved in sales. |

| Marketing Expenses | Advertising expenses a company incurs in selling the products or services. |

| Occupancy Expenses | Rent, depreciation and amortisation, utilities, maintenance, insurance, rates and taxes, and other expenses of premises occupied by the business. |

| Administration Expenses | Consists of salaries paid to employees not directly involved in the selling of the product, research and development costs, and other miscellaneous charges that must be subtracted from the company's income. |

| Finance Cost | Interest paid on bank overdrafts, loans and financial lease obligations. |

| Income Tax | The sum of the tax currently payable and deferred tax. The tax currently payable is based on taxable profit for the year. Taxable profit differs from profit as reported in the income statement, because of items of income or expense that are taxable or deductible in other years and items that are never taxable or deductible. |

| Dividends | Distributions from retained earnings to owners of an entity. |

| Retained Earnings | Amounts an entity generates and has not been distributed to owners. |

| Balance Sheet (Statement of Financial Position) | Provides a snapshot of a business' health at a point in time. It is a summary of what the business owns (assets) and owes (liabilities). Balance sheets are usually prepared at the close of an accounting period such as month-end, quarter-end or year-end. |

| Intangible Assets | Cannot be seen or touched and include items such as goodwill, patents, brands and trademarks. |

| Contingent Liabilities | Debts that the firm may be faced with in future, e.g. legal disputes, guarantees or assets financed with residual values. These are revealed in the notes to the balance sheet. |

| Analysis and Interpretation | Analysis is the process of examining the info on the financial statements. Interpretation is using the analysed info to make informed business decisions. Aim is to assess the financial health of the business. |

| Methods of Analysing Financial Statements | * Comparisons of financial statements * Ratio analysis * Calculation of ratios |

| Comparisons of Financial Statements | - Comparative Financial Statements Compare the financial statements for a required period of time, e.g. 10 years. The trend over the years can then be calculated and analysed. - Indexed Financial Statements The first year is shown as the base year (100%) and the subsequent years and figures are shown as percentages of that year. Overview of the growth or decline form the base year to a certain date. - Common Size Statements Each item on the statements is stated as a % of the total of the specific section, e.g. in the statement of financial position, current and non-current assets will be stated as a percentage of the total assets; in the statement of profit or loss and other comprehensive income, the figures will be stated as a % of revenue. |

| Ratio Analysis | Compare items or examine the relationships between items on a financial statement. Ratios illustrate relationships between different aspects of an organisation's operations and provide relative measures of the financial condition and performance of the organisation. Ratio analysis can be performed using time-series or cross-sectional analysis, or a combination of both. - Cross-sectional analysis involves the comparison of different firms' financial ratios at the same point in time. - Time-series analysis involves comparison of a company's current to its past performance and the evaluation of developing trends. |

| Calculation of Ratios | - Liquidity ratios - Efficiency ratios - Profitability ratios - Solvency ratios |

| Liquidity Ratios | Indicate the ability of the organisation to generate and conserve cash from its working capital in order to meet its short-term debts. Working capital refers to the current assets and current liabilities. |

| Efficiency Ratios | Measure how efficiently assets and liabilities have been utilised within the business. These ratios can calculate the turnover of receivables, the repayment of liabilities and the general use of inventory and machinery. |

| Profitability Ratios | Deal with the return of profit on the capital invested in a company. |

| Solvency Ratios | Measure the organisation's ability to repay its long-term debts, which include the repayment of capital and the payment of interest. |

| Current Ratio Calculation | Indicates the business' ability to settle short-term obligations using short-term assets. |

| Quick ratio/acid test ratio calculation | Measures the immediate debt-paying ability of the company. |

| Debtors turnover calculation | Indicates the number of times debtors are covered by credit sales. |

| Receivable days calculation (debtors' collection period) | Shows how long debtors take to pay in days. |

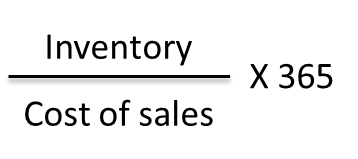

| Inventory turnover calculation | Indicates how many times inventory on hand has been sold during the year. May indicate whether there is an over- or under-investment in inventory. |

| Days inventory on hand calculation | Indicates how many days inventory spends on the shelf before it is sold. |

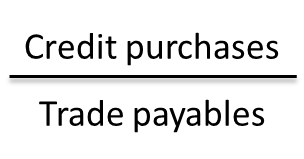

| Creditors turnover calculation | Indicates how many times creditors are paid during the year. |

| Payable days calculation (creditors' payment period) | Indicates how long in days the business takes to repay the creditors. |

| Gross profit margin calculation | Expresses the gross profit as a % of revenue. |

| Operating profit margin calculation | Net profit after accounting for operating expenditure but before finance cost, tax and investment income. Expressed as a % of revenue. |

| Net profit margin calculation | Expresses the net profit as a % of revenue. Looks at the relationship between profits earned and sales generated. |

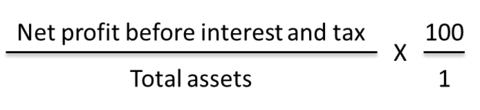

| Return on assets calculation | Indicates whether the assets of the business are being used effectively to produce a reasonable profit. |

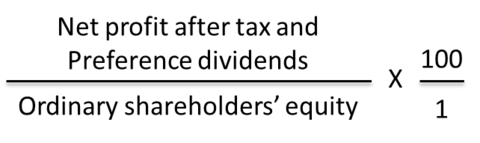

| Return on equity calculation | Expresses the relationship between the profit attributable to ordinary shareholders and the capital invested by ordinary shareholders. |

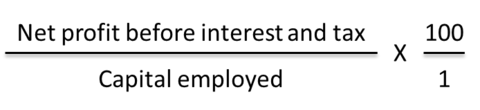

| Return on capital employed calculation | Expresses the relationship between the profits earned and owner's capital invested plus long-term financing. Net profit amount is before interest paid if it is assumed that the interest paid relates only to long-term liabilities. |

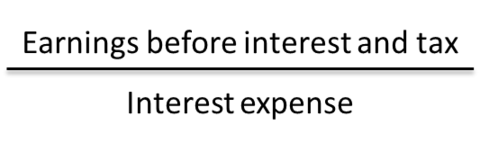

| Interest cover ratio calculation | Measures the number of times the operating profit will cover interest expense. The more coverage, the safer it is to borrow funds. |

| Debt to equity ratio calculation | Measures the level of financial risk. Debt financing creates an obligation that has to be paid whether or not the organisation can afford it. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Möchten Sie mit GoConqr kostenlos Ihre eigenen Karteikarten erstellen? Mehr erfahren.