3850123

Description

Quiz by Justin Guy (just, updated more than 1 year ago

|

|

Created by Justin Guy (just

about 9 years ago

|

|

Question 1

Question

If contributions, benefits or availability of BRFs are discriminatory, a corrective amendment may be adopted within 9½ months after the close of the plan year.

Answer

- True

- False

Question 2

Question

A uniform points plan is the only type of nondesign-based safe harbor defined contribution plan.

Answer

- True

- False

Question 3

Question

A rate group consists of a single HCE and each NHCE who has an equal or greater allocation rate or accrual rate.

Answer

- True

- False

Question 4

Question

If plans are aggregated to satisfy the coverage tests under IRC §410(b), they must be aggregated to satisfy the nondiscrimination tests under IRC §401(a)(4).

Answer

- True

- False

Question 5

Question

If two or more plans are permissively aggregated for nondiscrimination testing, then the nondiscriminatory classification tests must be applied as if the plans were a single plan.

Answer

- True

- False

Question 6

Question

For purposes of satisfying the gateway contribution test, each NHCE who benefits under the plan must receive an allocation of at least 5 percent of IRC §415 compensation.

Answer

- True

- False

Question 7

Question

Age-based plans automatically satisfy nondiscrimination testing since every participant has the same EBAR.

Answer

- True

- False

Question 8

Question

Cross-tested defined contribution plans may not use the safe harbor approach to satisfying nondiscrimination under IRC §401(a)(4).

Answer

- True

- False

Question 9

Question

A plan must benefit at least one NHCE to satisfy nondiscrimination requirements.

Answer

- True

- False

Question 10

Question

Rate groups must satisfy the average benefit test.

Answer

- True

- False

Question 11

Question

All of the following statements regarding nondiscrimination testing under IRC §401(a)(4) are TRUE, EXCEPT:

Answer

-

A. A design-based safe harbor plan is deemed to be nondiscriminatory.

-

B. A plan that provides an allocation that is a uniform percentage of compensation is a design-based safe harbor plan.

-

C. A plan that provides an allocation that is a uniform dollar amount to each participant is a nondesign-based safe harbor plan.

-

D. Design-based safe harbor plans must use a definition of compensation for allocation purposes that satisfies IRC §414(s).

-

E. A uniform points plan is a nondesign-based safe harbor plan.

Question 12

Question

None of the following provisions affect a plan’s ability to rely on the IRC §401(a)(4) safe harbors, EXCEPT:

Answer

-

A. Multiple entry dates

-

B. Imposing a last day requirement for allocation purposes

-

C. Imposing an hours of service requirement for allocation purposes

-

D. Limiting allocations to a total of $5,000

-

E. Lower allocations for one or more NHCEs

Question 13

Question

All of the following statements regarding general testing are TRUE, EXCEPT:

Answer

-

A. Rate groups that satisfy the coverage tests of IRC §410(b) are nondiscriminatory under IRC §401(a)(4).

-

B. Rate groups can be tested by converting the employer contributions into allocation rates.

-

C. Rate groups can be tested by converting the employer contributions into EBARs.

-

D. Determining whether a defined contribution plan satisfies nondiscrimination requirements on a benefits basis is a type of safe harbor and avoids general testing.

-

E. Elective deferrals are included when determining rate groups for the average benefits portion of the general test.

Question 14

Question

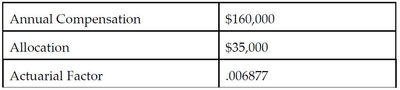

Based on the following information, determine the EBAR for the following employee:

{kind=link}

Answer

-

A. 3.18%

-

B. 6.64%

-

C. 31.81%

-

D. 66.47%

-

E. 664.74%

Question 15

Question

All of the following statements regarding EBARs are TRUE, EXCEPT:

Answer

-

A. EBARs may be expressed as percentages of average annual compensation.

-

B. The testing age used to normalize the benefits must be the Social Security retirement age.

-

C. EBARs may be expressed as dollar amounts.

-

D. The allocations used in the EBAR calculation may be based on the current plan year.

-

E. The allocations used in the EBAR calculation may be based on the current plan year and all prior years.

Question 16

Question

All of the following statements regarding gateway requirements are TRUE, EXCEPT:

Answer

-

A. The one-third test must be determined on the basis of IRC §415 compensation.

-

B. The one-third test is satisfied if the lowest permissible allocation rate for any NHCE who benefits under the plan is 2% and the highest allocation rate for any HCE who benefits under the plan is 5%.

-

C. The 5 percent test is satisfied if each NHCE receives an allocation of 6% of IRC §415 compensation.

-

D. The one-third test is satisfied if the lowest permissible allocation rate for any NHCE who benefits under the plan is 3% and the highest allocation rate for any HCE who benefits under the plan is 9%.

-

E. Compensation from date of participation may be used in the one-third test and the 5 percent test.

Question 17

Question

All of the following statements regarding nondiscrimination testing are TRUE, EXCEPT:

Answer

-

A. Plans cannot be aggregated for coverage and tested separately for nondiscrimination.

-

B. Plans cannot be permissively aggregated unless they have the same plan year.

-

C. Elective deferrals can be general tested to satisfy nondiscrimination requirements.

-

D. A plan may permissively disaggregate otherwise excludable employees for nondiscrimination purposes.

-

E. Permissive disaggregation of certain portions of a plan into component parts for nondiscrimination testing is known as restructuring.

Question 18

Question

All of the following statements regarding BRFs are TRUE, EXCEPT:

Answer

-

A. Participant loans are a right or feature subject to nondiscrimination requirements.

-

B. Life insurance is considered an ancillary benefit.

-

C. A lump sum distribution is an optional form of benefit.

-

D. Participant-direction of investments is a right or feature subject to nondiscrimination requirements.

-

E. A BRF is considered nondiscriminatory if it satisfies either the current availability test or the effective availability test.

Want to create your own Quizzes for free with GoConqr? Learn more.