9074146

Description

Quiz by Hello World, updated more than 1 year ago

|

|

Created by Hello World

over 7 years ago

|

|

Question 1

Question

1. The scientific method can best be defined as

Answer

-

• the use of modern electronic testing equipment in understanding the world.

-

• the use of controlled experiments in understanding the way the world works.

-

• the dispassionate development and testing of theories about how the world works

-

• finding evidence to support preconceived theories about how the world works.

Question 2

Question

2. The use of theory and observation is more difficult in economics than in sciences such as physics due to

Answer

-

• The difficulty in actually performing an experiment in an economic system.

-

• The difficulty in devising an economic experiment.

-

• The difficulty in evaluating an economic experiment.

-

• All of the above.

Question 3

Question

3. Because it is difficult for economists to use experiments to generate economic data

Answer

-

• They do without.

-

• They make up the data.

-

• They ask policymakers to conduct experiments for them.

-

• They use whatever data the world gives them.

Question 4

Question

4. Economists make assumptions

Answer

-

• To diminish the chance of wrong answers.

-

• To make certain that all necessary variables are included.

-

• Because all scientists make assumptions.

-

• To make the world easier to understand.

Question 5

Question

5. If an economist develops a theory about international trade based on the assumption that there are only two countries and two goods.

Answer

-

• The theory can be useful only in situations involving two countries and two goods.

-

• It is a total waste of time, since the actual world has many countries trading many goods.

-

• The theory can be useful in helping economists understand the complex world of international trade involving many countries and many goods.

-

• The theory can be useful in the classroom, but has no use in the real world.

Question 6

Question

6. What would be the best statement about a theory based on assumptions which are not true?

Answer

-

• If the assumptions underlying the theory are not true, the theory must be false.

-

• The ideas may be good in theory, but not in practice.

-

• The theory is a good one if no logical mistakes were made in developing it.

-

• The theory is a good one if it helps to understand how the world works.

Question 7

Question

7. What is the goal of theories?

Answer

-

• To provide an interesting, but not useful, framework of analysis

-

• To help scientists understand how the world works.

-

• To provoke stimulating debate in scientific journals

-

• To demonstrate that the developer of the theory is capable of logical thinking

Question 8

Question

8. Economists use models in order to

Answer

-

• Lear how the economy works.

-

• Make their profession appear more precise.

-

• Make economics difficult for students.

-

• Make sure that all of the details of the economy are included in their analysis

Question 9

Question

9. A model

Answer

-

• Simplifies reality.

-

• Can explain how the economy is organized.

-

• Assumes away irrelevant details.

-

• All of the above

Question 10

Question

10. Economic models are usually composed of

Answer

-

• Plastic.

-

• Beautiful people.

-

• Assumptions only.

-

• Diagrams and equations.

Question 11

Question

11. Which of the following is the most accurate statement about economic models?

Answer

-

• Economic models attempt mirror reality exactly.

-

• Economic models are useful, but should not be used for policy- making.

-

• Economic models cannot be used in the real world because they omit details.

-

• Economic models omit many details to allow us to see what is truly important.

Question 12

Question

12. The foundation stones from which economic models are built are

Answer

-

• Economic policies.

-

• The legal system.

-

• Assumptions.

-

• Statistical forecasts.

Question 13

Question

13. A circular-flow diagram is

Answer

-

• A model that illustrates cost – benefit analysis.

-

• A model that explains how the economy is organized.

-

• A model that explains how banks circulate money in the economy.

-

• A model that shows the flow of traffic in an economic region.

Question 14

Question

14. Factors of production are

Answer

-

• Inputs into the production process.

-

• Weather, social, and political conditions that affect production.

-

• The physical relationships between economic inputs and outputs.

-

• The mathematical calculations firms make to determine production.

Question 15

Question

15. For a scientist, the decision of which assumption to make

Answer

-

• Is part art.

-

• Is the flip of a coin.

-

• Is almost impossible.

-

• Is the easiest part of the scientific method.

Question 16

Question

1.People who provide you with goods and services

Answer

-

Are acting out of generosity

-

Are acting because they like you

-

Are required to do so by government

-

Do so because they get something in return

Question 17

Question

2.A rancher can produce only hamburgers, and a farmer can produce only french fries. The rancher and the farmer both like both foods. They

Answer

-

cannot gain from trade.

-

could gain from trade under certain circumstances, but not always.

-

could gain from trade because each would enjoy a greater variety of food.

-

could gain from trade only if each were indifferent between hamburgers and french fries.

Question 18

Question

3.Without trade

Answer

-

a country’s production possibilities frontier is also its consumption possibilities frontier.

-

a country is better off because it will become self-sufficient.

-

a country can still benefit from international specialization.

-

more product variety is available in a country.

Question 19

Question

4. Which of the following is NOT correct?

Answer

-

Trade allows for specialization.

-

Trade is good for nations.

-

Trade is based on absolute advantage.

-

Trade allows individuals to consume outside of their individual production possibilities curve.

Question 20

Question

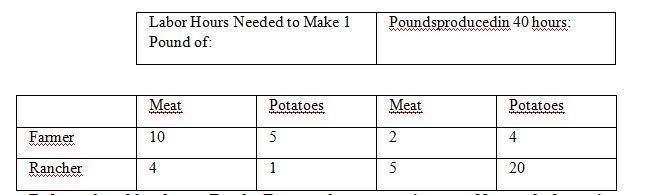

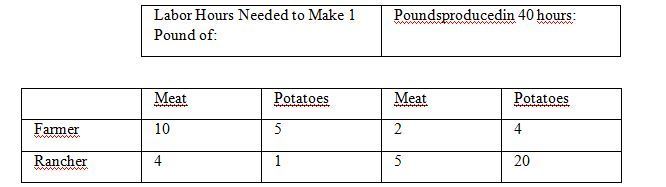

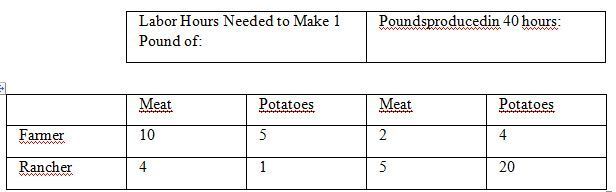

Refer to the tables shown. For the Farmer, the opportunity cost of 1 pound of meat is:

Image:

1 (image/jpeg)

{kind=link}

Answer

-

8 hours labor

-

4 hours labor

-

2 pounds potatoes

-

1/2 pound potatoes

Question 21

Question

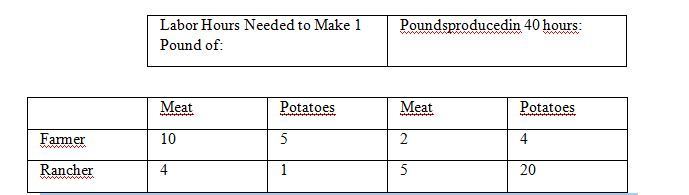

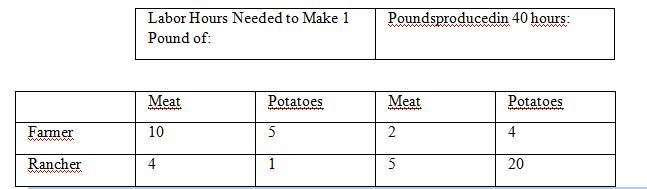

Refer to the tables shown. For the Rancher, the opportunity cost of 1 pound of meat is:

Image:

3,6 (image/jpeg)

{kind=link}

Answer

-

5 hours labor

-

1 hour labor

-

¼ pound of potatoes

-

4 pounds potatoes

Question 22

Question

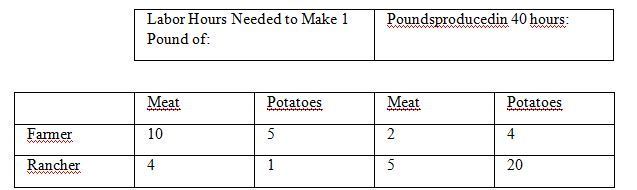

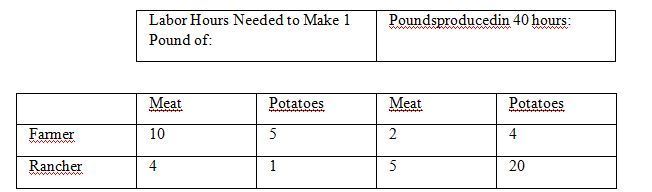

Refer to the tables shown. For the Farmer, the opportunity cost of 1 pound of potatoes is:

Image:

3,7 (image/jpeg)

{kind=link}

Answer

-

8 hours labor

-

4 hour labor

-

2 pound of meat

-

½ pounds meat

Question 23

Question

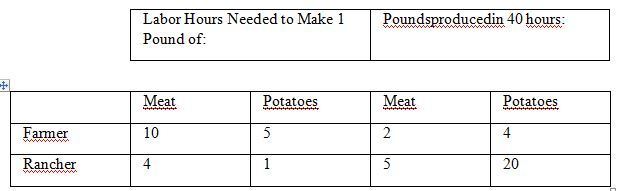

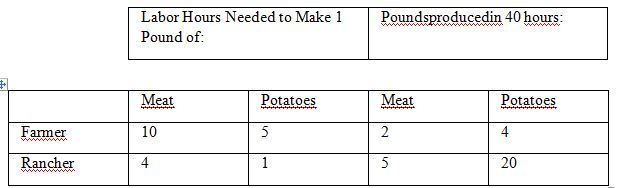

Refer to the tables shown. For the Rancher, the opportunity cost of 1 pound of potatoes is:

Image:

3,8 (image/jpeg)

{kind=link}

Answer

-

4 hours labor

-

2 hours labor

-

1/4 pound of meat

-

4 pounds meat

Question 24

Question

Refer to the tables shown. The Farmer has an absolute advantage in _____and the Rancher has an absolute advantage in_____.

Image:

3,9 (image/jpeg)

{kind=link}

Answer

-

Meat, potatoes

-

Potatoes, meat

-

Meat, meat

-

Neither food, both goods

Question 25

Question

Refer to the tables shown. The Rancher has an absolute advantage in _____and the Farmer has a comparative advantage in_____.

Image:

3,10 (image/jpeg)

{kind=link}

Answer

-

Both goods, meat

-

meat, neither good

-

Meat, potatoes

-

both goods, potatoes

Question 26

Question

11. A country’s consumption possibilities frontier can be outside its production possibilities frontier

Answer

-

With trade

-

By allocating resources differently

-

By producing a greater variety of goods and services

-

By lowering unemployment in the country

Question 27

Question

12. A production possibilities frontier will be linear and not bowed out if

Answer

-

a. no tradeoffs exist.

-

b. the tradeoff between the two goods is always at a constant rate.

-

c. unemployment is zero.

-

d. resources are allocated efficiently.

Question 28

Question

Refer to the tables shown. The Farmer has an absolute advantage in _____and the Rancher has a comparative advantage in_____.

Image:

3,13 (image/jpeg)

{kind=link}

Answer

-

Meat, meat

-

Potatoes, potatoes

-

Neither good, potatoes

-

Neither good, meat

Question 29

Question

Refer to the tables shown. The Rancher has a comparative advantage in _____and the Farmer has a comparative advantage in_____.

Image:

3,14 (image/jpeg)

{kind=link}

Answer

-

Potatoes, meat

-

Both goods, neither good

-

Meat, potatoes

-

Neither good, both goods

Question 30

Question

Refer to the tables shown. The Farmer and Rancher both could benefit by the Farmer specializing in ________and the Rancher specializing in_______.

Image:

3,15 (image/jpeg)

{kind=link}

Answer

-

Meat, potatoes

-

Potatoes, meat

-

Neither good, meat

-

They cannot benefit by specialization and trade

Question 31

Question

16. Imports are

Answer

-

Goods produced abroad and sold domestically

-

People who work in foreign countries

-

Whatever is given up to obtain some item

-

An example of an economic model

Question 32

Question

17.Exports are

Answer

-

Goods produced domestically and sold abroad

-

A country’s ability to produce a good

-

A limit placed on the quantity of goods brought into a country

Question 33

Question

Which of the following are the words most commonly used by economists?

Answer

-

• Supply and demand

-

• Scarcity and human wants

-

• Entrepreneurial ability

-

• Prices and exchange

Question 34

Question

In a free market, who determines how much of a good will be sold and the price at which it is sold?

Answer

-

• Demanders

-

• Suppliers

-

• The government

-

• Both suppliers and demanders

Question 35

Question

A market is

Answer

-

• A place where only buyers come together

-

• A place where only sellers meet

-

• A group of demanders and suppliers of a particular good or service

-

• A group of people with common desires

Question 36

Question

Firms that sell their products in a competitive market have limited pricing power because

Answer

-

• Sellers have reason to charge more than their competitors

-

• Each buyer has a significant influence on the price of the product

-

• Other sellers are offering very similar products

-

• None of the above are correct

Question 37

Question

If a seller in a competitive market chooses to charge more than the market price, then

Answer

-

• Buyers will tend to make their purchases elsewhere

-

• The owners of the raw materials used in production would raise the prices for the raw materials

-

• Other sellers would also raise their price

-

• Buyers would tend to buy more from this seller

Question 38

Question

If buyers and/or sellers are price takers, then individually

Answer

-

• They can somewhat influence the market price

-

• They have ultimate control over market price

-

• Buyers will be able to find prices lower than those determined in the market

-

• They have no influence on market price because there are so many in the market

Question 39

Question

There are thousands of wheat farmers who produce and sell wheat and there are millions of consumers who use wheat and wheat products. The market for wheat would be considered

Answer

-

• Perfectly competitive

-

• Monopolistic

-

• Monopolistically competitive

-

• Oligopolistic

Question 40

Question

As a seller, you would be considered part of a perfectly competitive market if

Answer

-

• Your actions are quickly followed by competitors

-

• Your pricing has no impact on the amount you can sell

-

• Your actions essentially have no effect on the market price

-

• Increases in the price of your product have an impact on the market price

Question 41

Question

A market with many sellers offering similar but slightly different products is called

Answer

-

• A monopoly

-

• Oligopolistic

-

• Monopolistically competitive

Question 42

Question

If a seller is supplying a product that is slightly different than that of many close competitors and is able to charge a different price than competitors, then the seller

Answer

-

• Is a monopolist

-

• Is producing a homogeneous product

-

• Will eventually have to decrease the price

-

• Is participating in a monopolistically competitive market

Question 43

Question

Which of the following would NOT be a determinant of demand?

Answer

-

• Tastes

-

• The price of related goods

-

• Income

-

• The prices of the inputs used to produce the good

Question 44

Question

If a good is “normal”, then an increase in income will result in

Answer

-

• A decrease in the demand for the good

-

• No change in the demand for the good

-

• An increase in the demand for the good

-

• A lower market price

Question 45

Question

Suppose you like banana cream pie made with vanilla pudding. Assuming all other things are constant, you notice that the price of bananas is higher. How would your demand for vanilla pudding be affected by this?

Answer

-

• It would increase

-

• It would decrease

-

• It would be unaffected

-

• There is insufficient information given to answer the question

Question 46

Question

A higher for batteries would tend to

Answer

-

• Increase the demand for flashlights

-

• Decrease the demand for electricity

-

• Increase the demand for electricity

-

• Increase the demand for batteries

Question 47

Question

In general, elasticity is

Answer

-

• the friction that develops between buyer and seller in a market.

-

• a measure of how much government intervention is prevalent in a market.

-

• a measure of how much buyers and sellers respond to changes in market conditions.

-

• a measure of the competitive nature of a market.

Question 48

Question

Demand is said to be elastic

Answer

-

• if the price of the good responds substantially to changes in demand.

-

• if demand shiftssubstantially when the price of the good changes.

-

• if the quantity demanded responds substantially to changes in the price of the good.

-

• if buyers don’t respond much to changes in the price of the good.

Question 49

Question

Demand is said to be inelastic

Answer

-

• if the price of the good responds only slightly to changes in demand.

-

• if demand shiftsonly slightly when the price of the good changes.

-

• if buyers respond substantially to changes in the price of the good.

-

• if the quantity demanded changes only slightly when the price of the good changes.

Question 50

Question

If a good is a necessity, demand for the good would tend to be

Answer

-

• elastic.

-

• inelastic.

-

• unit elastic.

-

• horizontal.

Question 51

Question

If a good is a luxury, demand for the good would tend to be

Answer

-

• elastic.

-

• inelastic.

-

• unit elastic.

-

• horizontal.

Question 52

Question

If a person has very little concern for his/her health, demand for health care would tend to be

Answer

-

• elastic.

-

• inelastic.

-

• unit elastic.

-

• horizontal.

Question 53

Question

A person who lives to be on the sea in a boat would tend to have what type of demand for boats?

Answer

-

• elastic.

-

• inelastic.

-

• unit elastic.

-

• weak.

Question 54

Question

Demand for a good would tend to be more elastic

Answer

-

• the greater the availability of complements.

-

• the longer the period of time considered.

-

• the fewer substitutes there are.

-

• the broader the definition of the market .

Question 55

Question

If there are very few, if any, good substitutes for good A, then

Answer

-

• the demand for good A would tend to be price elastic.

-

• the supply of good A would tend to be price elastic.

-

• the demand for good A would tend to be price inelastic.

-

• the demand for good A would tend to beincome elastic.

Question 56

Question

The demand for a good tends to be more elastic

Answer

-

• the greater the availability of close substitutes.

-

• the narrower the definition of the market.

-

• the longer the period of time.

-

• All of the above are correct.

Question 57

Question

Economists compute the price elasticity of demand as

Answer

-

• the percentage change in the price divided by the percentage change in quantity demanded.

-

• the change in the quantity demanded divided by the change in price.

-

• the percentage change in the quantity demanded divided by the percentage change in price.

-

• the percentage change in the quantity demanded divided by the percentage change in income.

Question 58

Question

Suppose there is a 6 percent increase in the price of good X and a resulting 6 percent decrease in the quantity of X demanded. Price elasticity of demand for X is

Answer

-

• 1.

-

• 0.

-

• 6.

-

• Infinite.

Question 59

Question

Suppose the price of product X is reduced from $1.45 to $1.25 and, as a result, the quantity of X demanded increases from 2,000 to 2,200. Using the midpoint method, the price elasticity of demand for X in the given price range is

Answer

-

• 2.00.

-

• 1.00.

-

• 1.55.

-

• .64.

Question 60

Question

If the price elasticity of demand for a good is 4.0, then a 10 percent increase in price would result in a

Answer

-

• 4.0 percent decrease in the quantity demanded.

-

• 10 percent decrease in the quantity demanded.

-

• 40 percent decrease in the quantity demanded.

-

• 400 percent decrease in the quantity demanded.

Question 61

Question

The main reason for using the midpoint method is that it

Answer

-

• gives the same answer regardless of the direction of change.

-

• rounds prices to the nearest dollar.

-

• uses fewer numbers.

-

• rounds quantities to the nearest whole unit.

Question 62

Question

The local pizza restaurant makes such great bread sticks that consumers do not respond much to a change in the price. If the owner is only interested in increasing revenue, he should

Answer

-

• Raise the price of the bread sticks.

-

• lower the price of the bread sticks.

-

• Reduce costs.

-

• Leave the price of the bread sticks alone.

Question 63

Question

1) A legal maximum price at which a good can be sold is a

Answer

-

• price floor

-

• price stabilization

-

• price support

-

• price ceiling

Question 64

Question

• A legal minimum price at which a good can be sold is a

Answer

-

• price floor

-

• price stabilization

-

• price ceiling

-

• price cut

Question 65

Question

• If a price ceiling is not binding

Answer

-

• the equilibrium price is above the ceiling

-

• the equilibrium price is below the ceiling

-

• it has no legal enforcement mechanism

-

• people must voluntarily agree to abide by it

Question 66

Question

• A price ceiling which is not binding

Answer

-

• has no effect

-

• is a detriment to society

-

• will cause a shortage

-

• will cause a surplus

Question 67

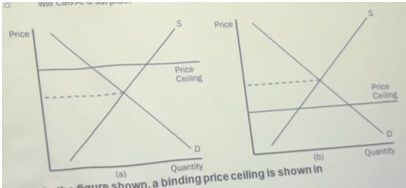

{kind=link}

Answer

-

• panel (a)

-

• panel (b)

-

• both panel (a) and panel (b)

-

• neither panel (a) nor panel (b)

Question 68

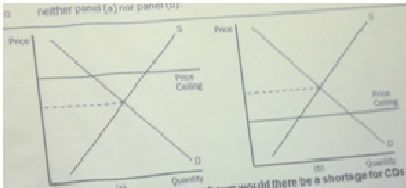

Question

• In which panel(s) in the figure shown would there be a shortage for CDs at the market price?

Image:

6,6 (image/jpeg)

{kind=link}

Answer

-

• panel (a)

-

• panel (b)

-

• both panel (a) and panel (b)

-

• neither panel (a) nor panel (b)

Question 69

Question

• If a price ceiling is a binding constraint on the market

Answer

-

• the equilibrium price must be below the price ceiling

-

• the equilibrium price must be above the price ceiling

-

• the forcesof supply and demand must be in equilibrium

-

• it will have no effecton supply or demand

Question 70

Question

• If a price ceiling is a binding constraint

Answer

-

• the actual price will be below the price ceiling

-

• the actual price will be above the price ceiling

-

• the equilibrium price will equal the price ceiling

-

• the actual price will be equal the price ceiling

Question 71

Question

• A binding price ceiling is imposed on the market for peaches. At the ceiling price,

Answer

-

• the quantity demanded of peaches will be greater than the quantity supplied

-

• the quantity demanded of peaches will be equal to the quantity supplied

-

• the quantity demanded of peaches will be smaller than the quantity supplied

-

• the quantity demanded of peaches will be artificiallyrestricted by the price ceiling

Question 72

Question

• A binding price ceiling in the computer market will cause

Answer

-

o a surplus of computers

-

o a shortage of computers

-

o an increase in the demand for computers

-

o quantity demanded of computers to be equal to quantity supplied

Question 73

Question

• A binding price ceiling will make it necessary to

Answer

-

o supply more of the product

-

o develop a way of rationing the product, because there will be a shortage

-

o develop a better marketing plan, because there will be a surplus

-

o increase demand for product, because there will be a surplus

Question 74

Question

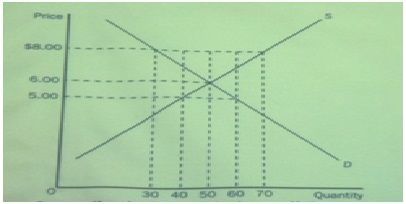

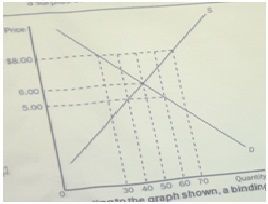

• According to the graph shown, if the government imposes a binding price ceiling in this market at a price of $5.00, the result would be

Image:

6,12 (image/jpeg)

{kind=link}

Answer

-

• a shortage of 30 units

-

• a shortage of 20 units

-

• a surplus of 40 units

-

• a surplus of 20 units

Question 75

Question

• According to the graph shown, a binding price ceiling would exist at a price of

Image:

6,13 (image/jpeg)

{kind=link}

Answer

-

• $8.00

-

• $6.00

-

• $5.00

Question 76

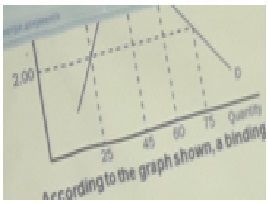

Question

• According to the graph shown, a binding price floor would exist at a price of

Image:

6,14 (image/jpeg)

{kind=link}

Answer

-

• $5.00

-

• $2.00

-

• $6.00

-

• none of the above

Question 77

Question

• Rationing by long lines

Answer

-

• is inefficient, because it wastes buyers’ time

-

• is efficient, because those who are willing to wait the longest get the goods

-

• is the only way scarce goods can be rationed

-

• is only necessary if price ceilings are not binding

Question 78

Question

• According to the law of supply,

Answer

-

• the supply curve slopes downward

-

• firms are willing to produce a greater quantity of a good when the price of the good is higher

-

• firms’ production levels are not correlated with the price of a good

-

• none of the above

Question 79

Question

Industrial organization is the study of

Answer

-

• How industries organize for political advantage

-

• Now firms’ decisions regarding prices and quantities depend on the market conditions they face

-

• How labor unions organize workers in industries

-

• How profitable firms are in organized industries

Question 80

Question

The amount of money that firms receives from the sale of its outputs is called

Answer

-

• Total revenue

-

• Total net profit

-

• Total gross profit

-

• Net revenue

Question 81

Question

The amount of money that a firm pays to buy inputs is called

Answer

-

• Total cost

-

• Variable cost

-

• Marginal cost

-

• Fixed cost

Question 82

Question

Profit defined as

Answer

-

• Net revenue minus depreciation

-

• Average revenue minus average total cost

-

• Marginal revenue minus marginal cost

-

• Total revenue minus total cost

Question 83

Question

Profit plus total cost equals

Answer

-

• Total revenue

-

• Not profit

-

• Operational profit

-

• Capital profit

Question 84

Question

Total revenue equals

Answer

-

• Total output multiplied by sales price of output

-

• Total output multiplied by the profit

-

• (total output multiplied by sales price) – inventory surplus

-

• (total output multiplied by sales price) – inventory shortage

Question 85

Question

Those things that must be forgone to acquire a good are called

Answer

-

• competitors

-

• substitutes

-

• opportunity cost

-

• explicit costs

Question 86

Question

XYZ corporation produced 300 units of output but sold only 275 of the units it produced. The average cost of production for each unit of output produced was $100. Each of the 275 units sold were sold for a price of $95. Total revenue for the XYZ corporations would be

Answer

-

• $30,000.

-

• $28,500.

-

• $26,125.

-

• -$3,875.

Question 87

Question

Opportunity costs are comprised of

Answer

-

• Explicit costs

-

• Implicit costs

-

• Forgone income.

-

• all of the above

Question 88

Question

Which of the following would be categorized as an opportunity cost?

(i) Wages of workers

(ii) Raw materials costs

(iii) Forgone investment opportunities

Answer

-

• (i) and (iii)

-

• (iii) only

-

• (ii) and (iii)

-

• All the above

Question 89

Question

Which of the following is an implicit cost?

(i) A business owner forgoing an opportunity to earn a large salary working for a wall street brokerage firm

(ii) Interest on debt

(iii) Uncollected revenue

Answer

-

• (i) only

-

• (ii) and (iii)

-

• (i) and (iii)

-

• All the above

Question 90

Question

An example of an implicit cost of production would be

Answer

-

• The cost of raw materials for producing bread in a bakery.

-

• The cost of a delivery truck in a business that rarely makes deliveries.

-

• The income an entrepreneur could have earned working for someone else.

-

• All of the above

Question 91

Question

To an economist, the field of industrial organization answers which of the following questions?

Answer

-

• How does the difference in the number of firms affect prices and efficiency of market outcomes?

-

• Why are consumers subject to the law of demand?

-

• Why do firms experience falling marginal product of labor?

-

• Why do firms consider production costs when determining product supply?

Question 92

Question

Assuming John owns a shoe-shine business, his accountant most likely includes which of the following costs on his financial statements?

Answer

-

• Cost of shoe polish

-

• Dividends John’s money was earning in the stock market before John sold his stock and bought a shoe-shine booth

-

• Wages John could earn washing windows

-

• All of the above

Question 93

Question

An important implicit cost of almost every business is

Answer

-

• The opportunity cost of financial capital that has been invested in the business

-

• The cost of accounting services

-

• The cost of compliance with government regulation

-

• The cost of debt

Question 94

Question

1. Monopolistic competition is characterized by which of the following attributes? (i) Many sellers (ii) Product differentiation (iii) barriers to entry

Answer

-

(i) and (iii) only

-

(i) and (ii) only

-

(ii) and (iii) only

-

All of the above

Question 95

Question

2. In a monopolistically competitive market structure each firm sells a good that is

Answer

-

Slightly different from goods sold be other firms

-

Produced at minimum average cost

-

Identical to other goods sold in the market

-

Produced at minimum marginal cost

Question 96

Question

3. In a monopolistically competitive industry, price is

Answer

-

Above marginal cost since each firm is a price setter

-

Equal to marginal cost since each firm is a price taker

-

Below marginal cost since each firm is a price setter

-

Always a fraction of marginal cost since each firm is a price setter.

Question 97

Question

4. Which of the following market structures is consistent with many sellers in the market place? (i) perfect competition (ii) monopolistic competition (iii) monopoly (iv) oligopoly

Answer

-

(i) only

-

both (i) and (ii)

-

(ii) only

-

all of the above

Question 98

Question

5. Which of the following market structures do not have barriers to entry that restrict firms from entering the market? (i) perfect competition (ii) monopolistic competition (iii) monopoly (iv) oligopoly

Answer

-

(i) only

-

(i) and (ii) only

-

(ii) and (iii) only

-

All of the above are correct.

Question 99

Question

6. A profit-maximizing firm in a monopolistically competitive market differs from a firm in a perfectly competitive market because the firm in the monopolistically competitive market

Answer

-

Faces a downward-sloping demand curve for its product

-

Faces a horizontal demand curve at the market clearing price

-

Is characterized by market share maximization

-

Has no barriers to entry

Question 100

Question

7. The profit-maximizing rule for a firm in a monopolistically competitive market is to select the quantity at which

Answer

-

Average revenue exceeds average total cost

-

Marginal revenue is equal to marginal cost

-

Average total cost is minimum

-

Average total cost is equal to marginal revenue

Question 101

Question

8. A profit-maximizing firm in a monopolistically competitive market is characterized by which of the following?

Answer

-

Revenue is always maximized along with profit

-

Average revenue exceeds marginal revenue

-

Marginal revenue exceeds average revenue.

-

Average revenue is equal to marginal revenue.

Question 102

Question

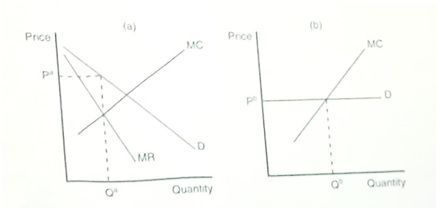

9. Which of the following graphs would most likely represent profit-maximizing firm in a monopolistically competitive market?

Image:

8.9 (image/jpeg)

{kind=link}

Answer

-

panel a

-

panel b

Question 103

Question

10. The firm depicted in panel b faces a horizontal demand curve. If panel b depicts a profit-maximizing firm,

Answer

-

• It would not be operating in a monopolistically competitive market

-

• It would not have excess capacity in its production as long as it is earning zero economic profit

-

• It is not able to choose the price at which it sells its product

-

• All the above

Question 104

Question

11. Product differentiation causes the seller of a good to face what type of demand curve?

Answer

-

• Horizontal

-

• Vertical

-

• Downward sloping

-

• Upward sloping

Question 105

Question

12. Which of the graphs shown would be consistent with a firm in a monopolistically competitive market that is minimizing its losses?

Answer

-

• Panel a

-

• Panel b

-

• Panel c

-

• Panel d

Question 106

Question

13. Free entry into a market drives economic profit to

Answer

-

• Zero

-

• The Nash equilibrium

Question 107

Question

1. Which of the following best describes the economy’s stock of equipment and structures?

Answer

-

Aggregate stock

-

Capital

-

Aggregate demand

-

Long term inventory

Question 108

Question

2. Rent, interest, and profit are all forms of income paid to the owners of

Answer

-

Land and capital

-

Long term inventory

-

Aggregate stock

-

Aggregate demand

Question 109

Question

3. For a computer software firm, capital could be thought of as

(i) Wages paid to computer programmers.

(ii) Computer equipment

(iii) The interest earned by shareholders.

Answer

-

(i) Only

-

(i) and(iii)

-

(ii) Only

-

(ii) and(iii)

Question 110

Question

4. When a gas station sells gas, which of the following would qualify as capital?

(i) The service attendants time

(ii) The physical space on which the station exists

(iii) The gas tanks and pumps

Answer

-

(i)only

-

(iii)only

-

(i)and(iii)

-

(ii)and(iii)

Question 111

Question

5. A firm’s demand for a factor of production is derived form its decision to supply a good in the market, therefore we call this type of demand

Answer

-

Derived demand

-

Supplied demand

-

Differentiated demand

-

Secondary demand

Question 112

Question

6. Labor markets are governed by the force(s) of

Answer

-

Supply and demand

-

Regulation and supply

-

Supply only

-

Demand only

Question 113

Question

7. Gertrude Kelp owns thee boats that participate in commercial fishing for fresh pacific salmon off the coast of Alaska. As part of her business the hires a captain and several crew members for each boat. In the market for fresh pacific salmon, Gertrude is one of thousands of fisher-persons. While Gertrude usually catches a significant number of fish each year, her contribution to the entire harvest of salmon is negligible relative to the size of the market.

What type of market structure is most likely to characterize the fresh pacific salmon market?

Answer

-

Monopolist

-

Oligopolist

-

Perfect competitor

-

Monopolistic competitor

Question 114

Question

8. Gertrude Kelp owns thee boats that participate in commercial fishing for fresh pacific salmon off the coast of Alaska. As part of her business the hires a captain and several crew members for each boat. In the market for fresh pacific salmon, Gertrude is one of thousands of fisher-persons. While Gertrude usually catches a significant number of fish each year, her contribution to the entire harvest of salmon is negligible relative to the size of the market.

Answer

-

Hire more crew workers

-

Become a seller in the factor market

-

Reduce her demand for crew workers

-

Try to increase her catch to make up for lost revenue

Question 115

Question

9. Gertrude Kelp owns thee boats that participate in commercial fishing for fresh pacific salmon off the coast of Alaska. As part of her business the hires a captain and several crew members for each boat. In the market for fresh pacific salmon, Gertrude is one of thousands of fisher-persons. While Gertrude usually catches a significant number of fish each year, her contribution to the entire harvest of salmon is negligible relative to the size of the market.

If Gertrude is a competitor in both the fresh pacific salmon market and the market for crew workers she is called a

Answer

-

Price taker in the salmon market and a wage setter in the crew market

-

Price taker in both markets

-

Price takerin the crew market and a price setter in the salmon market

-

Price setter in both markets

Question 116

Question

10. Gertrude Kelp owns thee boats that participate in commercial fishing for fresh pacific salmon off the coast of Alaska. As part of her business the hires a captain and several crew members for each boat. In the market for fresh pacific salmon, Gertrude is one of thousands of fisher-persons. While Gertrude usually catches a significant number of fish each year, her contribution to the entire harvest of salmon is negligible relative to the size of the market.

If Gertrude is a price taker in the crew market, she has only to decide

Answer

-

The wage to pay the crew she hires

-

How many crew members to hire

-

The price of fish she will catch

-

The size of the boats others use to catch salmon

Question 117

Question

11. Gertrude Kelp owns thee boats that participate in commercial fishing for fresh pacific salmon off the coast of Alaska. As part of her business the hires a captain and several crew members for each boat. In the market for fresh pacific salmon, Gertrude is one of thousands of fisher-persons. While Gertrude usually catches a significant number of fish each year, her contribution to the entire harvest of salmon is negligible relative to the size of the market.

Labor market theory assumes that Gertrude’s demand for crew workers and her supply of fresh pacific salmon results from

Answer

-

Her intrinsic desire to hire crew members

-

Her primary goal of maximizing profit

-

Altruistic motives to provide fresh salmon to consumers

-

All of the above

Question 118

Question

12. When a firm is a profit maximizer

Answer

-

It is driven to produce as much of its product as possible

-

It does not care directly about the number of workers it hires

-

It will measure its success by the number of employees it has

-

Its revenue will always be maximized as well

Question 119

Question

1. Macroeconomics is

Answer

-

• The study of market regulation.

-

• The study of economy-wide phenomena.

-

• The study of how households and firms make decisions and how they interact .

-

• The study of money and financial markets.

Question 120

Question

2. Statistics such as GDP, the unemployment rate, the rate of inflation, and the trade balance are

Answer

-

• Microeconomic, since they affect individual households and firms.

-

• Both microeconomic and macroeconomic.

-

• Macroeconomic, since they tell us something about the economy as a whole.

-

• Neither macroeconomic nor microeconomic.

Question 121

Question

3. The goal of macroeconomics is

Answer

-

• To explain the economic changes that affect a particular household, firm, or market.

-

• To explain the economic changes that affect many households, firms, and markets at once.

-

• To devise policies to deal with market failures such as monopoly, externalities, common resources, and public goods.

-

• All of the above.

Question 122

Question

4. Gross Domestic Product measures

Answer

-

• The total income of everyone in the economy.

-

• The total expenditure on the economy’s output of goods and services.

-

• Both a and b.

-

• Neither a nor b.

Question 123

Question

5. For the economy as a whole

Answer

-

• Income must equal expenditure.

-

• Expenditure exceeds income because of taxes.

-

• Income exceeds expenditure because of saving.

-

• Expenditure exceeds income because of the government budget deficit.

Question 124

Question

6. In a simple circular-flow diagram, total income and total expenditure in an economy

Answer

-

• Are seldom equal because of the dynamic changes which occur in an economy.

-

• Are equal only when all goods and services produced are sold.

-

• Are always equal because every transaction has both a buyer and seller.

-

• Are always equal because of accounting rules.

Question 125

Question

7. If you buy a new snowboard from the local sporting goods store, as a result of your purchase

Answer

-

• The increase in expenditure in the economy will equal the increase in income in economy.

-

• The increase in expenditure in the economy will exceed the increase in income in the economy

-

• The increase in income in the economy will exceed the increase in expenditure in the economy.

-

• It is impossible to tell whether the increase in income in the economy will equal the increase in expenditure.

Question 126

Question

8. A circular- flow diagram is used to describe

Answer

-

• How weather patterns affect the economy.

-

• The most efficient organization of the work process.

-

• The flow of income and expenditures in an economy.

-

• How banks create money.

Question 127

Question

9. In the real economy, expenditure and income are always the same

Answer

-

• Only if households spend all of their income and buy all the goods and services produced in the economy

-

• Only if households spend all of their income.

-

• Only if households buy all the goods ad services produced in the economy.

-

• Regardless of whether households spend all of their income or buy all of the goods and services produced in the economy.

Question 128

Question

10. Which of the following statements best explains the total income and total expenditure in an economy?

Answer

-

• Government taxes firms and redistributes the money to households until household income is high enough to equal total expenditures.

-

• Total income and total expenditure are always equal in an economy because only households purchase goods and services.

-

• Total income and total expenditure are equal in an economy because firms use the money they receive in sales to pay for workers' wages, landowners' rent, and firm owners' profit.

-

• All of the above are correct explanations

Question 129

Question

11. Gross domestic product is defined as

Answer

-

• The market value of all final goods and services produced within a country in a given period of time.

-

• The market value of all final goods and services produced by a country’s citizens in a given period of time

-

• The market value of all goods and services producedwithin a country in a given period of time.

-

• The market value of all goods and services producedby a country’s citizens in a given period of time.

Question 130

Question

12. The real economy is more complicated than the one illustrated in a simple circular-flow diagram because

Answer

-

• Households do not buy all goods and services produced in the economy, and households do not spend all of their income on goods and services.

-

• Saving should be counted as part of expenditure.

-

• Taxes should be included as part of expenditure.

-

• The income government gives poor people should be counted as government production of human capital.

Question 131

Question

13. In order to include many different products in a summary or aggregate measure gdp

Answer

-

• Uses a combination of weights and measures.

-

• Uses a combination of price indexes and costs of productions

-

• Uses only cost of production of the products.

-

• Uses market prices.

Question 132

Question

14. A nation’s standard of living is measured by its

Answer

-

• Nominal GDP.

-

• Real GDP.

-

• Nominal GDP per person.

-

• Real GDP per person.

Question 133

Question

15. Which of the following is a store of value?

Answer

-

• U.S. government bonds.

-

• Currency

-

• Fine art.

-

• All of the above correct.

Question 134

Question

• Which of the following is a store of value?

Answer

-

• Currency

-

• U.S. government bonds

-

• Fine art

-

• All of the above are correct

Question 135

Question

• When you put money in a cookie jar, which function of money are you using?

Answer

-

• Store of value

-

• Medium of exchange

-

• Unit of account

-

• None of the above is correct

Question 136

Question

• Which of the following best illustrates the medium of exchange function of money?

Answer

-

• You pay for your textbooks with currency

-

• You mark prices of CDsat your music store in dollars

-

• You keep a jar of pennies

-

• None of the above is correct

Question 137

Question

• Liquidity refers to

Answer

-

• A measurement of the intrinsic value of commodity money

-

• The stability of an asset to serve as a store of value

-

• None of the above refers to liquidity

-

• The ease with which an asset is converted to the medium of exchange

Question 138

Question

• Fiat currency

Answer

-

• Is used as a medium of exchange.

-

• Is equivalent to wealth

-

• Is backed by gold

-

• Both b and c are correct

Question 139

Question

• Commodity money is

Answer

-

• More commonly used than fiat money

-

• Backed by gold

-

• Money with intrinsic value

-

• All of the above are correct

Question 140

Question

• Inflation can be measured by the

Answer

-

• Percentage change in the consumer price index

-

• Change in the consumer price index

-

• Percentage change in the price of a specific commodity

-

• Change in the price of a specific commodity

Question 141

Question

• The rate of inflation measures

Answer

-

• The rate of increase in nominal GDP

-

• The rate of increase in the price of particular good

-

• The rate of change in nominal interest rates

-

• The rate of increase in the overall level of prices

Question 142

Question

• Deflation is a time period during which

Answer

-

• Inflation falls

-

• Prices fall

-

• Output and prices fall

-

• Output falls

Question 143

Question

• An extraordinarily high rate of inflation is called

Answer

-

• Deflation

-

• Disinflation

-

• Classical inflation

-

• Hyperinflation

Question 144

Question

• The quantity theory of money

Answer

-

• Argues that inflation is caused by too little money in the economy

-

• Can explain both moderate and hyperinflations

-

• Is a fairly recent addition to economic theory

-

• All of the above are correct

Question 145

Question

• The price level

Answer

-

• Refers to the price of individual goods

-

• Is high when the value of money is high

-

• All of the above are correct

-

• Is measured by a price index like the CPI or GDP deflator

Question 146

Question

• When the price level rises, the number of dollars needed to buy a representative basket goods

Answer

-

• Increases, so the value of money rises

-

• Increases, so the value of money falls

-

• Decreases, so the value of money rises

-

• Decreases, so the value of money falls

Question 147

Question

• The value of money

Answer

-

• Is positively related to the price level

-

• Is constant

-

• Is determined by the supply and demand of money

-

• Is not explained by the quantity theory of money

Question 148

Question

1. The word economy comes from the Greek word for

Answer

-

a) “Environment”

-

c) “One who manages a household”

-

b) “One who participates in a market”

-

d) “Conservation”

Question 149

Question

2. Economics deals primarily with the concepts of

Answer

-

a) Poverty

-

b) Scarcity

-

c) Change

-

d) Power

Question 150

Question

3. Which of the following is NOT included in the decisions that every society must make?

Answer

-

a) What goods will be produced

-

b) What determines consumer preferences

-

c) Who will produce goods

-

d) Who will consume the goods

Question 151

Question

4. Scarcity exists when

Answer

-

a) There is less than an infinite among

-

b) There is less of a good or resources

-

c) Society can meet the wants (доконцаневидно)

-

d) невидно

Question 152

Question

5. Economics is defines as

Answer

-

a) The study of business

-

b) The study of how society manages its scarce resources

-

c) The study of central planning

-

d) The study of government regulation

Question 153

Question

6. Which of the following is NOT a major area of study for economists?

Answer

-

a) How people make decisions

-

b) How people interact with each other

-

c) How forces and trends affects the overall economy

-

d) How countries choose national leaders

Question 154

Question

7. Daniel decides to spend an hour playing basketball rather than working at $6 dollar per hour. His tradeoff is

Answer

-

b) the increase in skill he obtains from playing basketball for that hour.

-

a) Nothing, because he enjoys playing basketball more than working.

-

c) the $6 he could have earned.

-

d) nothing, because he spent $6 for admission into the sports complex to play basketball.

Question 155

Question

8. When society requires that firms reduce pollution,

Answer

-

a) there is no tradeoff, since everyone benefits from reduced pollution.

-

b) there is no tradeoff for society as a whole, since the cost of reducing pollut(доконцаневидно)

-

c) there is a tradeoffonly if some firms are forced to close.

-

d) there is no tradeoff because of reduced incomes o the firm (доконцаневидно) customers

Question 156

Question

9. A good definition of equity would be

Answer

-

a) everyone receiving the same income

-

b) fairness

-

c) efficiency

-

d) (доконцаневидно)

Question 157

Question

10. Вопроса не видно

Answer

-

a) the out-of-pocket expense of obtaining it

-

b) what you give up to get it

-

c) always measured in units of time

-

d) always higher than people think

Question 158

Question

11. The opportunity cost of going to college is

Answer

-

a) the total spent on food, clothing, books, transportation tuition, lodging, and other expenses.

-

b) zero for studens who are fortunate enough to have all of their college expenses paid by someone else.

-

c) the value of the best opportunity a student gives up to attend college.

-

d) zero, since a college education will allow a student to earn a larger income after graduation.

Question 159

Question

12. For most students, the largest single cost of a college education is

Answer

-

a) transportation, parking, and entertainment

-

b) tuition, fees, and books.

-

c) room and board.

-

d) the wages given up to attend school.

Question 160

Question

13. Carolyn decides to spend an additional hour working overtime rather than watching a video with her friends. She earns $8 for her hour's work. Her opportunity cost of working is

Answer

-

a) the $8 she earns

-

b) the enjoyment she would have received had she watched the video

-

c) the $8 minus the enjoyment she would have received from watching the video

-

d) nothing, since she would have received less than $8 of enjoyment from the video

Question 161

Question

14. College-age athletes who drop out of school to play professional sports

Answer

-

a) are making a bad economic decision, since they can't play forever.

-

b) are unaware of their opportunity cost of attending college.

-

c) underestimate the value of a college education.

-

d) are well aware that their opportunity cost of attending college is very high.

Question 162

Question

15. People make decisions at the margin by

Answer

-

a) following tradition

-

b) comparing costs and benefits

-

c) experience

-

d) calculating dollar costs

Question 163

Question

16. Which of the following is the best example of a marginal change?

Answer

-

a) Mark graduates from college and takes a job. His income increases from $10,000 per year to $50,000 per year.

-

b) The price of housing rises in Seattle by 25% in one year.

-

c) Kim works at the college bookstore. She gets a raise from $5.15 per hour to $5.20 per hour.

-

d) A drought hits the upper Midwest and the price of wheat increases from $4.00 per bushel to $8.00 per bushel.

Question 164

Question

17. A rational decision maker takes an action only if

Answer

-

a) The marginal benefit is greater than the marginal cost

-

b) The marginal benefit is less than the marginal cost

-

c) The marginal benefit is greater than the average cost

-

d) The marginal benefit is greater than both the average cost and the marginal cost

Question 165

Question

18. You have spent $500 purchasing and repairing an old car which you expects to sell for $800 once the repairs are complete. You discover that you need an additional part, which will cost $400, including labor. In order to complete the repairs. You can sell the car as it is now for $300. What should you do?

Answer

-

a) You should complete the repairs and sell the car

-

b) You should cut your losses and take the $300

-

c) You should never sell something for less than it costs

-

d) It doesn’t matter which action you take; the outcome is the same either way

Question 166

Question

19. In the former Soviet Union, producers were paid for meeting output targets, not for selling products. Under those circumstances, what were paid for meeting output targets, not for selling products. Under those circumstances, what were the economic incentives for producers?

Answer

-

b) To conserve on costs, so as to maintain efficiency in the economy

-

a) To produce good quality products so that society benefits from the resources used

-

c) To produce these products that society desires most

-

d) To produce enough to meet the output target, without regard for quality or cost

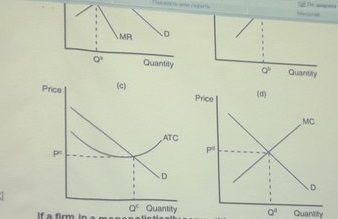

Question 167

{kind=link}

Answer

-

revenue is always maximized along with profit

-

average revenue exceeds marginal revenue

-

marginal revenue exceedsaverage revenue

-

average revenue is equas to marginal revenue

Question 168

Question

if a firm in a monopolistically competetivemarket was producingthe level of output depicted as Qdin panel d, it would

Image:

Losed (image/jpeg)

Answer

-

be minimizing its looses

-

be losing market share to other firms in the market

-

be operating at excees capacity

-

not be minimizing its profit

Question 169

Question

When government policies are being designed,

Answer

-

a. there is usually a tradeoff between equity and efficiency.

-

d. increasing efficiency usually results in more equity.

-

c. equity can usually be achieved without an efficiency loss.

-

b. equity and efficiency goals are usually independent of each other.

Want to create your own Quizzes for free with GoConqr? Learn more.