3848466

Descripción

Test por Justin Guy (just, actualizado hace más de 1 año

|

|

Creado por Justin Guy (just

hace más de 10 años

|

|

Pregunta 1

Pregunta

IRC §415 compensation must include elective deferrals to a 401(k) plan.

Respuesta

- True

- False

Pregunta 2

Pregunta

The average percentage of total compensation that is considered for NHCEs must be at least 70 percent of the average percentage of total compensation considered for HCEs in order for the definition of compensation to satisfy IRC §414(s).

Respuesta

- True

- False

Pregunta 3

Pregunta

The plan’s definition of compensation used for allocating contributions must satisfy the nondiscriminatory definition of compensation under IRC §414(s).

Respuesta

- True

- False

Pregunta 4

Pregunta

IRC §414(s) compensation must include elective deferrals to a 401(k) plan to avoid testing that definition for nondiscrimination.

Respuesta

- True

- False

Pregunta 5

Pregunta

IRC §415 compensation must be used to determine HCEs.

Respuesta

- True

- False

Pregunta 6

Pregunta

IRC §414(s) compensation must be used to determine key employees.

Respuesta

- True

- False

Pregunta 7

Pregunta

IRC §415 compensation must not include tips, depending on how IRC §415 compensation is defined.

Respuesta

- True

- False

Pregunta 8

Pregunta

Designated Roth contributions are included in IRC §415 compensation.

Respuesta

- True

- False

Pregunta 9

Pregunta

Excluding nontaxable fringe benefits from IRC §415 compensation is a safe harbor modification to IRC §414(s) compensation, meaning the resulting definition will not need to be tested for nondiscrimination purposes.

Respuesta

- True

- False

Pregunta 10

Pregunta

IRC §415 compensation is based on the plan year.

Respuesta

- True

- False

Pregunta 11

Pregunta

All of the following statements regarding IRC §414(s) compensation are TRUE, EXCEPT:

Respuesta

-

A. A plan using a safe harbor definition of IRC §414(s) compensation for nondiscrimination testing need not perform the compensation ratio test.

-

B. A plan using a nonsafe harbor definition of IRC §414(s) compensation for nondiscrimination testing must apply such definition consistently for all participants.

-

C. A plan may meet the safe harbor definition of IRC §414(s) compensation by including 401(k) elective deferrals and excluding 125 plan elective deferrals.

-

D. A plan may use a 12-month period other than the plan year for purposes of determining IRC §414(s) compensation.

-

E. A plan may use a rate-of-pay definition of compensation for IRC §414(s) purposes.

Pregunta 12

Pregunta

All of the following exclusions are deemed reasonable for defining IRC §414(s) compensation, EXCEPT:

Respuesta

-

A. 20 percent of regular compensation

-

B. Bonuses

-

C. Overtime

-

D. Expense allowances

-

E. Fringe benefits

Pregunta 13

Pregunta

Based on the following information, determine the participant’s IRC §415 compensation:

The employer sponsors a 401(k) plan that allows designated Roth contributions.

The plan excludes overtime for allocation purposes.

The participant’s taxable income, not including elective deferrals, is $58,000.

The participant defers $4,000 as pre-tax elective deferrals and $4,000 as designated Roth contributions.

The participant defers $500 into the employer’s IRC §125 plan.

The participant’s overtime compensation totals $3,000.

Respuesta

-

A. $58,000

-

B. $59,500

-

C. $62,500

-

D. $66,500

-

E. $69,500

Pregunta 14

Pregunta

All of the following statements regarding the calculation of the employer deduction are true, EXCEPT:

Respuesta

-

A. In the case of a short taxable year, the deduction limit for a defined contribution plan is applied to aggregate participant compensation paid for the short period.

-

B. A short taxable year results in a prorated compensation dollar limit under IRC §401(a)(17).

-

C. A short plan year does not directly affect the defined contribution deduction limit because that deduction limit is based on participant compensation for the employer’s taxable year.

-

D. Compensation for deduction purposes is measured on the basis of the employer’s taxable year, whereas compensation for IRC §415 purposes is measured on the basis of the limitation year.

-

E. The definition of compensation used for allocation purposes must be the same as the definition of compensation used for deduction purposes.

Pregunta 15

Pregunta

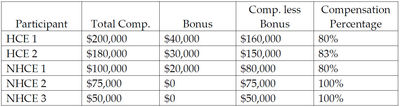

Based on the following information, which of the following statements regarding the compensation ratio is/are TRUE?

I. The plan passes the compensation ratio test.

II. The compensation ratio for the HCEs is 81.5%.

III. The compensation ratio for the NHCEs is 93.3%.

{kind=link}

Respuesta

-

A. I only

-

B. II only

-

C. I and II only

-

D. II and III only

-

E. I, II and III

¿Quieres crear tus propios Tests gratis con GoConqr? Más información.