6299423

Descripción

Fichas por Marinda Steenkamp, actualizado hace más de 1 año

|

|

Creado por Marinda Steenkamp

hace alrededor de 8 años

|

|

| Pregunta | Respuesta |

| Define 'Risk' | Risk relates to the chance of loss; to the variability of returns associated with a given asset. The more certain the return, the less variability and the less risk. |

| Give an example of a risk-free asset | Government Bonds |

| Define 'Return' | It is the total gain or loss experienced on an investment over a given period of time. |

| How is 'return' calculated? | the asset's cash distributions during the period + change in value / its beginning-of-period investment value |

| Provide the formula for calculating the rate of return earned on any assets over a period of time | rt = Ct + Pt - Pt-1 / Pt-1 rt -actual, expected or required rate of return Ct - cash flows received from the investment Pt - price (value) of asset at time t Pt-1 - price (value) of asset at time t-1 |

| Explain the difference between a realised and unrealised return. | Realised return - asset is purchased and sold during the time measured. Unrealised return - return that could have been realised if an asset had been purchased and sold during the period measured. |

| What does CAPM stand for? | Capital Asset Pricing Model |

| Explain the a 'risk-averse' financial manager, which most managers are. | The increase in possible return does not justify the higher risk because these managers shy away from risk and seek stability. |

| Explain the a 'risk-indifferent' financial manager. | They require no change in return for an increase in risk. |

| Explain the 'rational investor' type of financial manager | The required return increases for an increase in risk. These mangers require higher expected returns to compensate them for taking greater risk. |

| How do we assess risks? | By looking at expected-returns, as well as scenario analysis and probability distribution |

| How do we measure risk quantitatively? | Using statistical formulas such as the standard deviation the coefficient of variation it measures the variability of assets return. |

| Explain scenario analysis | it throws several scenarios at the risk to determine its worst, expected and best outcomes and returns. |

| How is an asset's risk measured through the use of 'the range'? | You would take the optimistic outcome and subtract the pessimistic outcome. The higher the range, he riskier the investment |

| Explain probability distributions | It indicate the probability/chance that an outcome could occur. It gives a more quantitative insight into an asset's risk. |

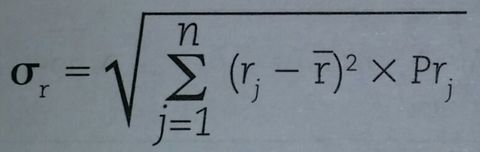

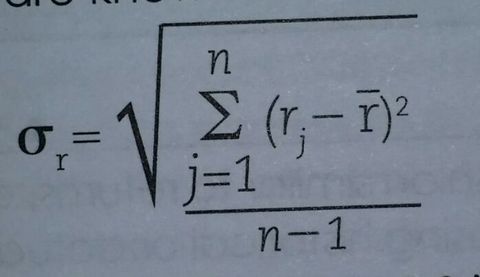

| Explain the statistical indicator, Standard Deviation (σr) Formula included | it measures the dispersion around the expected value the higher the standard deviation, the greater the risk |

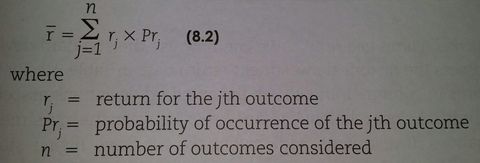

| Explain the expected value of return. Formula included | It is the most likely return on an asset. |

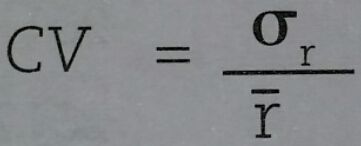

| Explain Coefficient of variation. Formula included | It is a measure of relative dispersion that is useful in comparing the risks of assets with differing expected returns the higher the CV, the greater the risk, the greater the expected return. |

| Explain the financial manager's goal with regards to creating an efficient portfolio. | He needs to create a portfolio that maximises return for a given level of risk or minimises risk for a given level of return. |

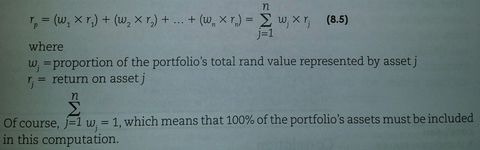

| Explain the return on a portfolio. formula included | It is a weighted average of the returns on the individual assets from which it is formed. |

| Explain Standard Deviation of a portfolio's returns. Formula included | You apply the normal formula for a single asset when probabilities are known. The following formula is used when the outcomes are known and their related probabilities are assumed to be equal. |

| Provide the definition of correlation | it is a statistical measure of the relationship between any two series of numbers representing data of any kind. |

| Explain positive correlation | It describes two series that move in the same direction. |

| Explain negative correlation | Describes two series that move in the opposite directions. |

| Explain Correlation Coefficient. | A measure of the degree of correlation between two series. +1 = perfectly positively correlated -1 = perfectly negatively correlated |

| What is the purpose of Diversification? | It assist in reducing the risk in the portfolio. "Not having all your eggs in one basket scenario" |

| Explain Capital Asset Pricing Model (CAPM) | It is the basic theory that links risk and return for all assets. |

| Explain the difference between 'diversifiable risk' and 'non-diversifiable risk' | Diversifiable risk - Strikes, litigation, loss of key contracts, etc Non-diversifiable risk - Ware, inflation, political events, etc |

| Explain Beta or Beta Coefficient (b) | It measures non-diversifiable risk. It is and index of the degree of movement of an asset's return in response to a change in the market return. |

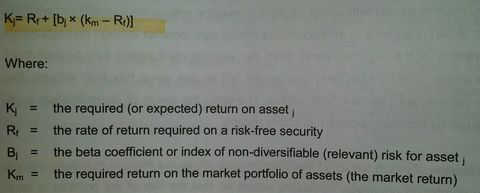

| The equation for the CAPM is |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

¿Quieres crear tus propias Fichas gratiscon GoConqr? Más información.