6479790

Descripción

Fichas por Hollie Ferris, actualizado hace más de 1 año

|

|

Creado por Hollie Ferris

hace alrededor de 8 años

|

|

| Pregunta | Respuesta |

| Corporate Aims | Long-term targets set to allow the business to develop and achieve it's mission. |

| Internal influences on corporate objectives and decisions | - Business ownership type - Business culture, employees values and influence on decisions - The company's current financial performance - The management team's views, values, priorities and leadership style - New leadership - Firm's stages of it's life-cycle - Stakeholder power - Existing brand image and reputation |

| External influences on corporate objectives and decisions | Sometimes outside the of the control of the business - Government policy and intervention - State of the economy - Rivals Actions - Market structure and changes - Demographic and population changes - Customer needs, wants, expectations, tastes and fashion. |

| Short-Termism | Focusing on Short-Term decisions at the expense of Long-Term |

| What might cause Short-Termisim? | - Financial pressure/Cash shortage - Pressure from shareholders to receive dividends - Poor Publicity |

| Consquences of Short-Termisim | - Conflict with shareholders - Loss of profit - May need extra finance - No future investments |

| Stragetic Decision Making | Decision mad eat corporate, senior management or executive level. These decisions will impact the actions of each of the key departments. |

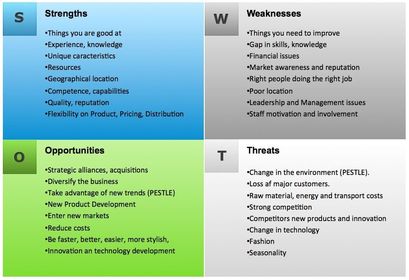

| What is a SWOT Analysis? | A technique that's allows an organisation to assess its overall position. Its a method of analysing the current situation by examining the INTERAL strengths and weaknesses of the business and the EXTERNAL opportunities and threats. |

| SWOT ANALYSIS | |

| Advantages of SWOT Analysis | - Understand the business better - Address weaknesses - Deter threats - Capitalise on opportunities - Advantage of strengths - Develop business goals and strategies |

| Disadvantages of SWOT Analysis | - Doesn't prioritise issues -Provide solutions or offer alternative options - Generate too many ideas - Produce a lot of information but not all of it is useful |

| Return On Capitial Employed | Operating Profit ------------------------------------- X 100 Capital Employed |

| Capital Structure Objectives | How a firm finances its overall operations and growth by using different sources of funds. |

| What is Gearing? | The percentage of capital invested into the business that has come from loans. |

| Gearing % | Non-Current Liabilities --------------------------------------------------X100 Share Capital + Non-Current Liabilities |

| Rewards of High Gearing | - Opportunities to expand - Able to respond quickly in a market - Low interest rates |

| Risks of High Gearing | - Not being able to repay - No extra money -High interest rates - Struggle for future loans |

| Non-Current Liabilites | - Loans (long term) - Mortgages - Debentures |

| Share Capital | + Doesn't need to be repaid - Dividends - Ownership - Dilution |

| Loans | + Instant + Control and Ownership - Has to be repaid with interest |

| What is a Balance Sheet? | A document describing the financial position of a company at a particular point in time. A financial snapshot |

| Non-Current assets | What the business owns with a lifespan of more than a year. They are used repeatedly as part of the firm's operations and will not regularly be sold. |

| Current Assets | Assets owned by the business that are likely to be turned into cash within one year. These assets constantly change form. |

| Current liabilities | Short-term debts of the business, will have to be repaid within one year |

| Long-term liabilities | Debts that needs to be repaid, but not within a year. Also known as creditors. |

| Capital and reserves | Shows how the assets and businesses have been financed. |

| Net current assets | Also known as working capital, this figure is important as it gives an idea of the firms liquidity. |

| Liquidity | A firms ability to pay its short term loans |

| Current ratio | Current Assets : Current Liabilities |

| Net assets | The figure shows what the business is worth at the moment the balance sheet was produced. (Non-current assets + current assets) - (Non-current liabilities + current liabilities) it should always be the same as total equity. |

| What is an income statement? | This statement describes the income and expenditure of a business over a period of time, usually a year. |

| Income statement | |

| Revenue | Turnover or sales income generated from sales |

| Cost of sales | Costs linked directly to the production of the product or service. E.g. Raw materials and variable costs |

| Gross profit | Revenue minus cost of sales. Gross profit shows how efficiently a business is converting its raw material or stock into finished products. |

| Expenses (overheads) | Indirect costs that are not directly related to producing the product or service. |

| Operating profit | Gross profit - expenses The profit earned from normal trading activities minus the costs involved in carrying out these activities. |

| Exceptional items | Items that have a one-off effect on profits. These are listed separately from other costs and sources of income as they aren't part of the business's normal activities and cannot be expected to happen again. |

| Finance income | Any interest paid to the company on money lent or saved. |

| Finance expenses | Any payments of interest on loans held. |

| Profit before tax | Operating profit - finance expenses (plus any finance income) |

| Profit for the year | Profit before tax - taxation |

| Earnings per share | Profit for the period/number of shares |

| What is ratio analysis? | A technique used to analyse a business's financial performance by comparing different pieces of data from company accounts. |

| Uses of ratio analysis | - Gives a more in-depth look at a company's financial performance. - Allows stakeholders to assess an organisation's performance. - Allows stakeholders to place key figures into context and provides good quality information to aid decision making. - Helps stakeholders to better understand a firm's performance in a number of key assets. |

| Limitations of ratio analysis | - Historical data, does not mean results will carry onto the future - Operational changes - Interpretation - Point in time |

| Profitably | Most firms' main aim is to make a profit for the owners. |

| How might a firm measure its size? | Market Share |

| Gross profit margin % | Gross Profit/Total revenue X 100 |

| Operating profit margin % | Operating profit/total revenue X 100 |

| What does ROCE do? | Lets owners or potential investors understand how efficient the business is at producing profit based on the capital invested in the business. |

| I | costs of goods sold/average inventory held measures how quickly inventory is converted into sales |

| Receivables days | Receivables/revenue X 365 |

| Payable days | Payables days/ cost of sales X 365 |

| What are the main ways a business can measure its performance and success? | - Labour productivity - Capacity utilization - Unit Cost - Profit - ROCE - Current ratio analysis - Market capital - Working capital |

{kind=link}

{kind=link}

¿Quieres crear tus propias Fichas gratiscon GoConqr? Más información.