10461247

Descripción

Mapa Mental por Ryan Beard, actualizado hace más de 1 año

|

|

Creado por Ryan Beard

hace más de 7 años

|

|

Business Studies

- Chapter 1: Introduction to small Businesses

- What is a business?

- A business is any organisation that makes goods or provides services.

- There are many types of businesses. These range from small businesses in towns to large worldwide businesses

- Businesses exist to provide goods or services.

- Goods are physical products such as burgers or cars.

- Services are non-physical items such as hairdressing.

- Customer needs are the wants and desires of buyers

- Nearly half a million businesses start up each year. A business start- up is a new firm operating in a

market for the first time. The vast majority of businesses are very small and operate in the service

sector.

- What is the service sector?

- The tertiary sector of the economy (also known as the service sector or the service industry) is one of

the three economic sectors, the others being the secondary sector (approximately the same as

manufacturing) and the primary sector (agriculture, fishing, and extraction such as mining).

- The tertiary sector of the economy (also known as the service sector or the service industry) is one of

the three economic sectors, the others being the secondary sector (approximately the same as

manufacturing) and the primary sector (agriculture, fishing, and extraction such as mining).

- What is the service sector?

- Businesses buy the products they need from suppliers – firms selling products to other businesses -

and sell to customers. The individual who uses the product is called a consumer. Sometimes the

customer and consumer are different people - for example, parents buy a pen for their child to use

at school.

- Businesses sell to customers in markets. A market is any place where buyers and sellers meet to

trade products - this can be a high street shop or a website.

- In order to create goods and services, a business buys or hires inputs such as raw materials,

equipment, buildings and staff. These inputs are transformed into outputs called products. These

products are the goods and services used by consumers. Production is the business activity of using

resources to make goods and services.

- Value is added to all products that a business makes. An example of this is

designer clothes They may be made for only 15 ponds but they will be sold for

about 200 pounds

- Value is added to all products that a business makes. An example of this is

designer clothes They may be made for only 15 ponds but they will be sold for

about 200 pounds

- Goods are physical products such as burgers or cars.

- A business is any organisation that makes goods or provides services.

- There are three main types of industry in which firms operate. These sectors form a chain of

production which provides customers with finished goods or services.

- Primary production

- this involves acquiring raw materials. For example, metals and coal have to be mined, oil drilled from

the ground, rubber tapped from trees, foodstuffs farmed and fish trawled. This is sometimes known

as extractive production.

- this involves acquiring raw materials. For example, metals and coal have to be mined, oil drilled from

the ground, rubber tapped from trees, foodstuffs farmed and fish trawled. This is sometimes known

as extractive production.

- Secondary production

- this is the manufacturing and assembly process. It involves converting raw materials into

components, for example, making plastics from oil. It also involves assembling the product, eg

building houses, bridges and roads.

- this is the manufacturing and assembly process. It involves converting raw materials into

components, for example, making plastics from oil. It also involves assembling the product, eg

building houses, bridges and roads.

- Tertiary production

- this refers to the commercial services that support the production and distribution process, eg

insurance, transport, advertising, warehousing and other services such as teaching and health care.

- this refers to the commercial services that support the production and distribution process, eg

insurance, transport, advertising, warehousing and other services such as teaching and health care.

- A business needs other sectors to keep working. This means that they are interdependent

- Primary production

- Why would you set up a business?

- First of all, there is massive profit to be made If the business becomes successful.

- Some people like the feeling of feeling independent

- This is not always the case as some businesses have partnerships

- This is not always the case as some businesses have partnerships

- Being able to make a difference by offering a service to the community such as a charity shop or

hospice.

- Every new business has to have a brand name or product

- Example

- Starbucks

- Logo known worldwide

- Specific trend only found in starbucks

- Writing name on cups

- Other actions that are only found there

- Writing name on cups

- Logo known worldwide

- Starbucks

- IKEA

- Certain furniture design

- Logo known everywhere

- Yellow and blue associated with IKEA

- Yellow and blue associated with IKEA

- Bags to advertise

- Adverts

- Fun Fact: Ikea's catalogue actually doesn't have any photos. Its all graphic design as its ten times cheaper

- Adverts on tv are used to promote company and products

- Billboards

- Websites are also used to promote their newest products

- Fun Fact: Ikea's catalogue actually doesn't have any photos. Its all graphic design as its ten times cheaper

- Adverts

- Certain furniture design

- Example

- A new business starts out with few, if any, customers and is likely to face competition from existing firms. To succeed

it needs to plan its launch carefully and work out how to create a competitive advantage over its rivals. To gain this

advantage, it needs to offer a product which customers prefer to a rival's product.

- Setting up a business involves risks and reward. Profit is the reward for risk-taking. Losses are the

penalty of business failure.

- An owner may decide to close a business if losses are being made, or if the level of profit is not

enough to make trading risks or hours worked worthwhile.

- Most small businesses have very limited resources. Research is costly and can seem like a poor use

of time. Some entrepreneurs ignore planning and analysis and instead rely on their gut instinct. They

launch products they believe customers want and competitors cannot match. Poor planning is a

major cause of business failure.

- There is an alternative. A business plan is a report by a new or existing business that contains all of

its research findings and explains why the firm hopes to succeed. A business plan includes the

results of market research and competitor analysis. Analysis is when a business interprets

information.

- Drawing up a business plan forces owners to think about their aims, the competition they will face,

their financial needs and their likely profits. Business plans help to reduce risk and reassure

stakeholders, such as banks.

- Drawing up a business plan forces owners to think about their aims, the competition they will face,

their financial needs and their likely profits. Business plans help to reduce risk and reassure

stakeholders, such as banks.

- Drawing up a business plan forces owners to think about their aims, the competition they will face,

their financial needs and their likely profits. Business plans help to reduce risk and reassure

stakeholders, such as banks.

- Competitive and changing markets

- In order to attract and satisfy customers, businesses need to be competitive and make products that

are superior to their rivals.

- This is not easy because businesses operate in a dynamic and challenging market place. Business

rivals are likely to be at work creating new products or improving operations to reduce costs and

drive down prices. Businesses may need to adapt their products because ever-changing fashion

trends mean that customer requirements evolve over time. Success today is no guarantee of future

profits.

- A competitive market will have many businesses trying to win the same customers. A monopoly is

either the only supplier in a market, or a large business with more than 25% of the market.

- Competition can make markets work better by improving these factors:

- Price: if there is only one retailer, products may not be competitively priced. If there are several

retailers, each retailer will lower their prices in an attempt to win customers. It is illegal for retailers

to agree between themselves to fix a price - they must compete for business.

- Product range: in order to attract customers away from rivals, businesses launch new varieties of

products they believe to be superior to their competitors.

- Customer service: retailers that provide a helpful and friendly service will win customer loyalty.

- Price: if there is only one retailer, products may not be competitively priced. If there are several

retailers, each retailer will lower their prices in an attempt to win customers. It is illegal for retailers

to agree between themselves to fix a price - they must compete for business.

- Competition can make markets work better by improving these factors:

- A competitive market will have many businesses trying to win the same customers. A monopoly is

either the only supplier in a market, or a large business with more than 25% of the market.

- This is not easy because businesses operate in a dynamic and challenging market place. Business

rivals are likely to be at work creating new products or improving operations to reduce costs and

drive down prices. Businesses may need to adapt their products because ever-changing fashion

trends mean that customer requirements evolve over time. Success today is no guarantee of future

profits.

- In order to attract and satisfy customers, businesses need to be competitive and make products that

are superior to their rivals.

- Drawing up a business plan forces owners to think about their aims, the competition they will face,

their financial needs and their likely profits. Business plans help to reduce risk and reassure

stakeholders, such as banks.

- There is an alternative. A business plan is a report by a new or existing business that contains all of

its research findings and explains why the firm hopes to succeed. A business plan includes the

results of market research and competitor analysis. Analysis is when a business interprets

information.

- Most small businesses have very limited resources. Research is costly and can seem like a poor use

of time. Some entrepreneurs ignore planning and analysis and instead rely on their gut instinct. They

launch products they believe customers want and competitors cannot match. Poor planning is a

major cause of business failure.

- An owner may decide to close a business if losses are being made, or if the level of profit is not

enough to make trading risks or hours worked worthwhile.

- Setting up a business involves risks and reward. Profit is the reward for risk-taking. Losses are the

penalty of business failure.

- Product differentiation – standing out from the crowd

- Businesses operate in competition with each other. If the market is large enough to support many

firms, a new business can open which imitates an existing idea. ‘Me too’ products can sometimes be

successful.

- However, businesses become more competitive by making products that stand out from the

competition in terms of price, quality or service. This is called product differentiation.

- Methods of creating

product differentiation

include:

- A strong brand image

- A unique selling point

- Competitive factors

- A strong brand image

- Methods of creating

product differentiation

include:

- However, businesses become more competitive by making products that stand out from the

competition in terms of price, quality or service. This is called product differentiation.

- Businesses operate in competition with each other. If the market is large enough to support many

firms, a new business can open which imitates an existing idea. ‘Me too’ products can sometimes be

successful.

- First of all, there is massive profit to be made If the business becomes successful.

- Forms of business ownership

- Sole traders

- A sole trader describes any business that is owned and controlled by one person - although they may

employ workers. Individuals who provide a specialist service like plumbers, hairdressers or

photographers are often sole traders.

- Sole traders do not have a separate legal existence from the business. In the eyes of the law, the

business and the owner are the same. As a result, the owner is personally liable for the firm's debts

and may have to pay for losses made by the business out of their own pocket. This is called unlimited

liability.

- A sole trader describes any business that is owned and controlled by one person - although they may

employ workers. Individuals who provide a specialist service like plumbers, hairdressers or

photographers are often sole traders.

- Partnership

- Doctors, dentists and solicitors are typical examples of professionals who may go into partnership

together and can benefit from shared expertise. One advantage of partnership is that there is

someone to consult on business decisions

- The main disadvantage of a partnership comes from shared responsibility. Disputes can arise over

decisions that have to be made, or about the effort one partner is putting into the firm compared

with another. Like a sole trader, partners (who have not registered as an LLP) have unlimited liability.

- Doctors, dentists and solicitors are typical examples of professionals who may go into partnership

together and can benefit from shared expertise. One advantage of partnership is that there is

someone to consult on business decisions

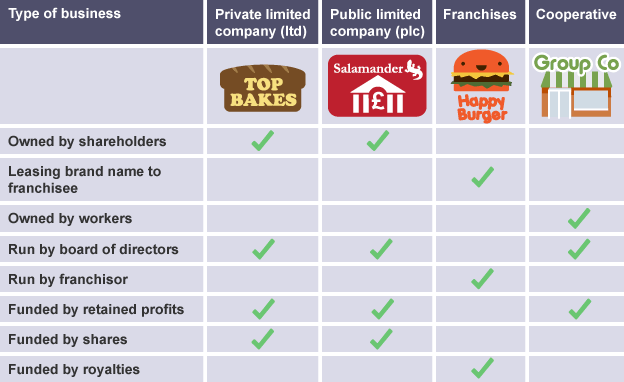

- Limited companies

- A limited company has special status in the eyes of the law. These types of company are incorporated,

which means they have their own legal identity and can sue or own assets in their own right. The

ownership of a limited company is divided up into equal parts called shares. Whoever owns one or

more of these is called a shareholder.

- Because limited companies have their own legal identity, their owners are not personally liable for the

firm's debts. The shareholders have limited liability, which is the major advantage of this type of

business legal structure.

- Unlike a sole trader or a partnership, the owners of a limited company are not necessarily involved in

running the business, unless they have been elected to the Board of Directors.

- Two main types of limited company

- Public limited company PLC

- Private limited company LTD

- Public limited company PLC

- A limited company has special status in the eyes of the law. These types of company are incorporated,

which means they have their own legal identity and can sue or own assets in their own right. The

ownership of a limited company is divided up into equal parts called shares. Whoever owns one or

more of these is called a shareholder.

- Sole traders

- What is a business?

Recursos multimedia adjuntos

{kind=link}

¿Quieres crear tus propios Mapas Mentales gratis con GoConqr? Más información.