215937

Description

Flashcards by beth auerbach, updated more than 1 year ago

|

|

Created by beth auerbach

over 11 years ago

|

|

| Question | Answer |

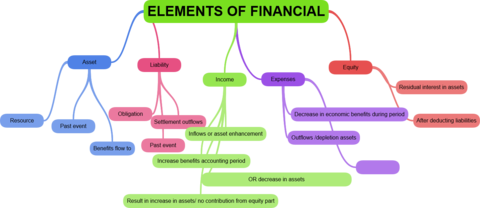

| ASSET | An asset is a resource controlled by the enterprise as a result of a past event and from which future economic benefits are expected to flow to the enterprise |

| LIABILITY | A liability is a present obligation arising from past events, the settlement of which is expected to result in an outflow of resources from the enterprise |

| EQUITY | Equity is the residual interest in the assets of the enterprise after deducting all its liabilities |

| INCOME | Income is increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants |

| EXPENSES | Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrence's of liabilities that result in decreases in equity, other than those relating to distributions to equity participants. |

| cima code of ethics | ICOPP |

| INTEGRITY | Straightforward Honest In all professional &business relationships |

| Objectivity | Not allow Bias Conflict of interest Undue influence to override judgements |

| PROFESSIONAL COMPETENCE AND DUE CARE | Maintain professional knowledge & skills Client to receive competent professional services |

| Confidentiality | Confidentiality of information Do not disclose unless without authority or legal duty No use of info for personal gain |

| Professional Behaviour | Comply with relevant laws and regulations Avoid action that discredit profession |

| Purpose of IFRS framework | 1) Review existing IAS's IFRS's and develop NEW IFRS's 2) harmonize existing accounting standards. 3)Assist national accounting setting boards 4) assist preparers in applying IFRS's 5) assist auditors do statements comply with IFRS |

| IFRS ADVISORY COUNCIL | Forum for groups to give opinions Advises on practical application and implementation of NEW IFRS *composed of wide geograph and jobs |

| IFRIC INTERNATIONAL FINANCIAL REPORTING INTERPRETATIONS COMMITTEE | GUIDANCE APPLICATION&interpretation Complex accounting issues Setting and improving IFRS Produces interpretations that ratified and issued by IASB |

| Complete set of financial statements include | 1. Statement of financial position (bal sheet) 2. Statement of profit and loss and other comprehensive income 3. St tempest of changes in equity 4. Statement of cash flows 5. Management notes |

| PURPOSE OF FINANCIAL STATEMENTS | IAS 1 (revised) states that the objective of financial statements is to provide information about the financial position, performance and cash flows of an enterprise that is useful in making economic decisions |

| A COMPLETE SET OF FINANCIAL STATEMENTS INCLUDES | • a statement of financial position; • either: – a statement of comprehensive income, or – an income statement plus a statement showing other comprehensive income; • a statement of changes in equity; • a statement of cash flows; • accounting policies note and other explanatory notes |

| ELEMENTS OF FINANCIAL STATEMENTS | |

| INTANGIBL ASSET | IDENTIFIABLE NON MONETARY WITHOUT PHYSICAL SUBSTANCE CONTROLLED/FEB FLOW |

| IMPAIRMENT | RECOVERABLE AMT LESS THAN BOOK VALUE |

| RECOVERABLE AMOUNT | HIGHER OF THE FAIR VALUE LSS COSTS TO SELL OR VALUE IN USE |

| CARRYING AMOUNT OF ASSET | THE AMOUNT RECOGNISED IN THE FINANCIAL STATEMENTS |

| IMPAIRMENT LOSS | AMOUNT |

| SUM OF THE DIGITS | N x (N+1) / 2 USE TO APPLY AMOUNT OF INTEREST TO EACH YEAR LAST PAYMETN IS 1 |

| ACTURARIAL METHOD FOR FINANCE LEASE | USE IF INTEREST RATE ISPROVIDED Beg Balance = Initial recognition amount Paid= Amount of the lease payment Subtotal = Beg Bal less lease payment Interest = Int % times Subtotal Closing Balance= Subtotal plus Interest |

| 4 Qualities IASB. FRAMEWORK | RRCU 1. Relevance 2. Reliability 3. Comparability 4. Understandability |

| RELEVANCE (one of IASB Framework Qualities) | Influences economic decisions of users helps to evaluate past present or future events confirming and predictive role |

| RELIABILITY ( one of the IASB Framework qualitative principles) | Free from MATERIAL ERRROR & BIAS INFORMATION CAN BE DEPENDED UPON |

| COMPARABILITY ( one of the IASB Framework Qualitative Principles) | Helps users COMPARE DATA OVER TIME Compare statements of Different Companies Fin Stms must show prior period numbers Accounting Policies must be knoown |

| UNDERSTANDABILITY ( one of the IASB Framework's QualitativePrinciples) | Assume readers have reasonable knowledge of BUSINESS ECONOMIC ACTIVITIES ACCOUNTING Able to study info with reasonable diligence |

| UNDERSTANDABILITY ( one of the IASB Framework's QualitativePrinciples) | Assume readers have reasonable knowledge of BUSINESS ECONOMIC ACTIVITIES ACCOUNTING Able to study info with reasonable diligence |

| 3 THINGS TAX EXPENSE CONSISTS OFl | CURRENT YEARS TAX CHG DEFERRED TAX MOVEMENT UNDER/OVER PROVISION |

| CONSTRUCTIONS WORKINGS | 1) Overall Profit 2) % of Completion 3)Income Statement Extract 4) SOFP ( from and to customer) |

| Constructions Working Amount due to/From Customer | Total Costs + Profit Realised Less Amount Billed |

| 3 tax bases | income - Corp or Personal Asset- Capital Gains Consumption - Sales Tax |

| Adam Smith Taxes Should be: | FACE Fair Absolute Convenient Efficient |

| 3 Major Principles | EEE Equitable Efficient Economic Benefit |

| Types of Taxes: UNIT | Based on the number of items or weight Example: EXISE DUTIES |

| Types of Taxes: Ad Voloren | Based on Value Sales Tax |

| Multi Stage Taxes | Cascade- Everyone Pays ( no refunds) VAT - Charged at all stages - refunds so only the end consumer pays |

| VAT OUTPUT | Tax charged to the customer on the products that the company is putting OUT |

| VAT INPUT | TAX paid on purchases that the company is inputting into their comapny |

| exempt vat | no tax in or out |

| ZERO RATED VAT | Not paid for by consumer - company can claim back |

| trading loss solutions | 1)Carry loss foward )Carry loss Backwards 3)Off set loss against other income/cap gains 4)Offset against porfits of other group company |

| LEASE - JOURNAL ENTRIES (4) | 1) Record Asset & Liability 2) Record Depreciation 3) Allocate and Record Finance Charge 4) Record Lease Payment |

| SHARE ISSUE COSTS | Deduct first from Share Premium Account then from retained earnings |

| The objective of general purpose financial reporting | The objective of general purpose financial reporting is • to provide financial information • about the reporting entity • that is useful to existing and potential investors, lenders and other creditors • in making decisions about providing resources to the entity.’ |

| 2 categories of qualitivative infomration The qualitative characteristics of useful financial information identify the types of information that are likely to be most useful to existing and potential investors, lenders and other creditors for making decisions about the reporting entity on the basis of information in its financial report (financial information). | 3.6 The qualitative characteristics of useful financial information identify the types of information that are likely to be most useful to existing and potential investors, lenders and other creditors for making decisions about the reporting entity on the basis of information in its financial report (financial information). They are categorised into two categories: • Fundamental qualitative characteristics • Enhancing qualitative characteristics. |

| PROFIT | DIFFERENCE BETWEEN COMPANYS BEGINNING CAPITAL AND ENDING CAPITAL |

| TO RECOGNIZE AN ELEMENTS IT MUST (3 THINGS) | *Definition- Meet the definiton of an element * Reliably MeasuredCost or Revenue must be reliably measured *Future Economic benefit will flow. |

| Fundamental QUALITATIVE characteristics (2) | Relevant: Capable of making difference in decisions ( Material) Faithful Representation: Complete, Free From Bias and Error |

| ENHANCING QUALITATIVE Characteristics (4) | C U T V Comparable- time Periods/ Other Companies Understandable- clear, concise Timeliness- Verifiable- verification can be direct or indirect |

| CAPITAL 2 TYPES | 1) FINANCING CAPITAL - Fund attributable to shareholder - wealth of Shareholders 2) OPERATING CAPITAL- Physical operating capital- support business operation. |

{kind=link}

3 comments

about 2 years ago

thank u

almost 10 years ago

thanks

over 10 years ago

great

Want to create your own Flashcards for free with GoConqr? Learn more.