2286391

Description

Flashcards by BryanTurner, updated more than 1 year ago

|

|

Created by BryanTurner

almost 10 years ago

|

|

| Question | Answer |

| Define a 'market' | A place or an arrangement where buyers and sellers exchange goods and services. |

| Define 'demand' | The quantity that buyers want to buy at a reasonable price. |

| Define 'supply' | The quantity of a good that sellers want to sell at a price that should make them profit. |

| Define 'equilibrium price' | The price at which supply meets demand. |

| What's the difference between excess demand and excess supply? | Excess demand is when demand for the item exceeds the supply. Excess supply is when supply for the item exceeds the demand. |

| What's the difference between a 'substitute' and a 'complement'? | A substitute is the best valued alternative e.g. if the price of petrol increases, there's always public transport. A complement is something that works with the good i.e. petrol works with your car. |

| Define an 'inferior good' | Usually, a cheap good that's low quality that some people would buy and others would spend a little more on the normal good. |

| What is 'price control'? | Government rules/laws setting price floors and ceilings. |

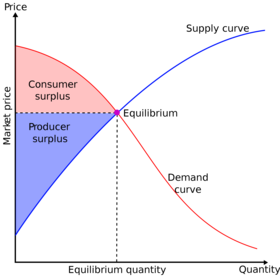

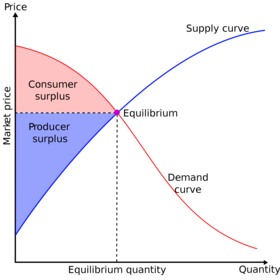

| Define 'Economic Surplus' | The sum of the consumer and the producer surplus. |

| Define 'Consumer Surplus' | The area below the market demand but ABOVE the equilibrium line. |

| Define 'Producer Surplus' | The area above the market demand but BELOW the equilibrium line. |

| Define 'Price Ceiling' | Reduces the quantity supplied to lead to excess demand. Must be placed below equilibrium price for maxiumum effectiveness. |

| Define 'Price Floor' | Reduces the quantity demanded, unless the government intervenes with another plan for the demand. Must be placed above equilibrium price for maxiumum effectiveness. |

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.