23190990

Description

Flashcards by Sophia Lynch, updated more than 1 year ago

|

|

Created by Sophia Lynch

over 5 years ago

|

|

| Question | Answer |

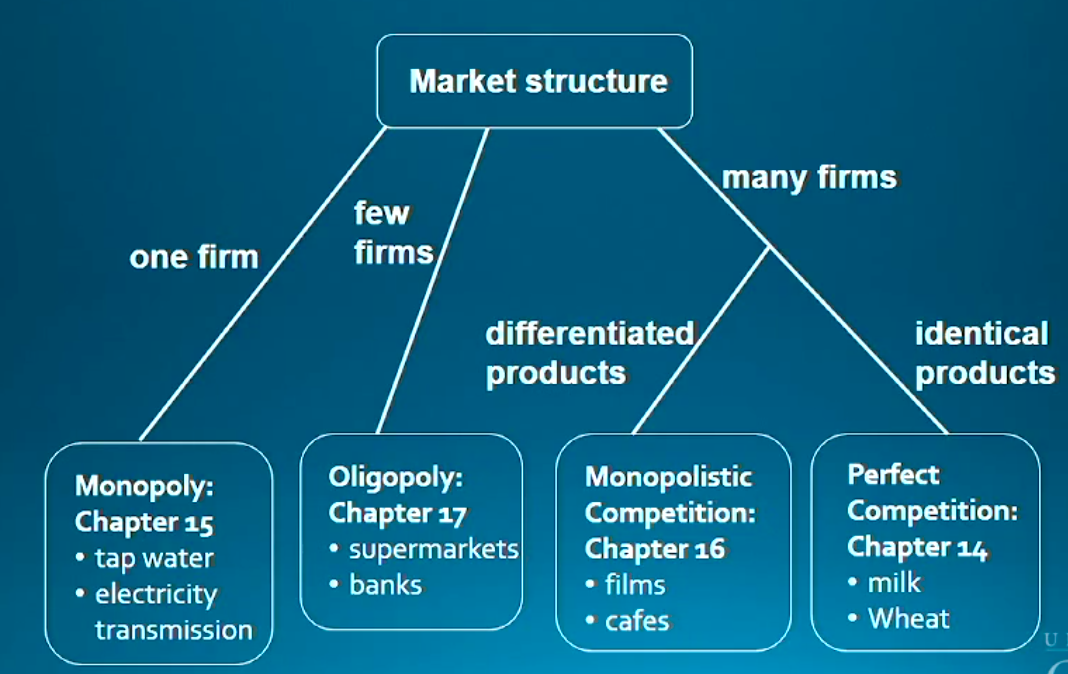

| Highly competitive markets (HCM) have... | Low barriers to entry hence zero economic profit in the long run. |

| (HCM) Homogenous product means... | Perfect competition |

| (HCM) Differentiated product means... | Monopolistic competition |

| Less competitive market (LCM) means... | High barriers to entry hence potential long-run profitability. |

| (LCM) One supplier and no good substitutes means it's a... | Monopoly |

| (LCM) 'Few' suppliers, same or close substitutes means it's a... | Oligopoly (Lots of strategic interaction) |

| Economic efficiency occurs when... | There is no deadweight loss (DWL). |

| Name an example of a monopoly, oligopoly, monopolistic competition and perfect competition. | |

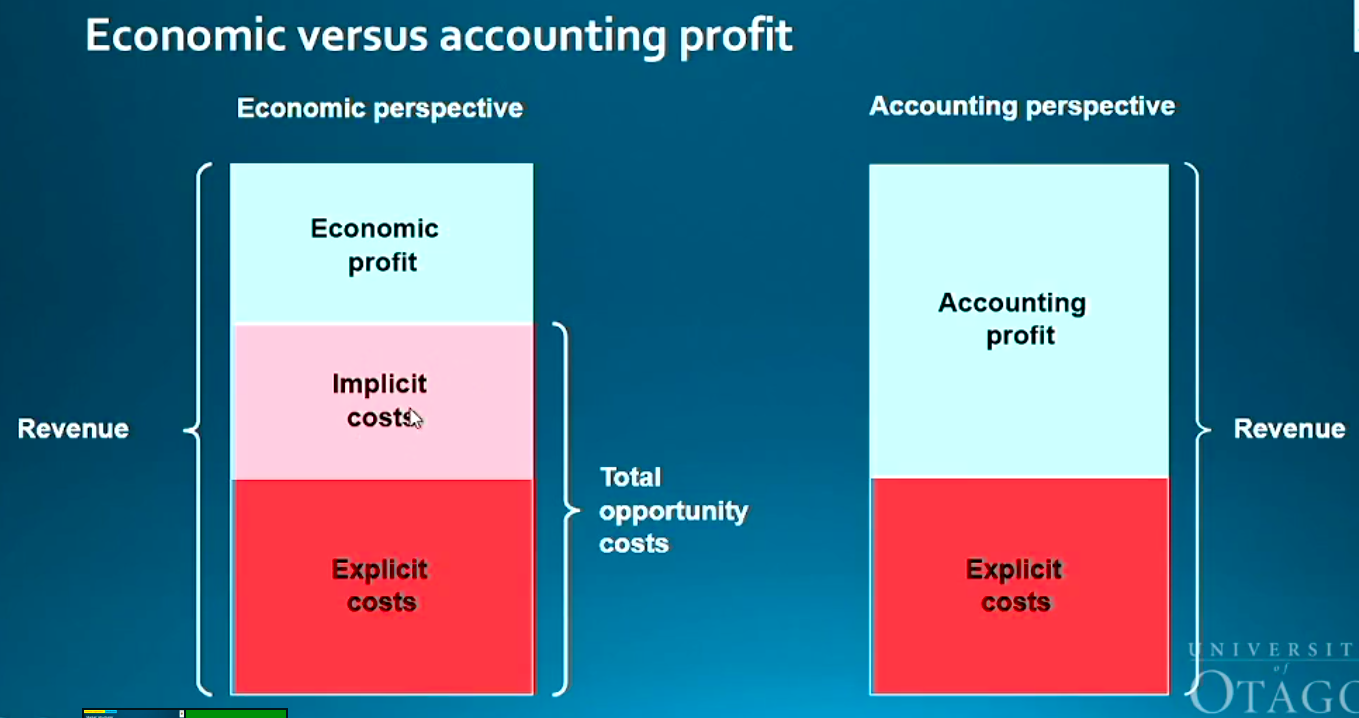

| What is 'Total Revenue' (TR)? | The amount a firm receives for it's sale of output. |

| What is 'Total Cost' (TC)? | The amount a firm pays for inputs into production. |

| The 'Cost Structure' is the same... | Irrespective of what market structure the firm is in. |

| What is an 'Explicit Cost'? | A physical cost paid for by a direct outlay of money by a firm, for e.g. it might have an invoice. Accounting |

| What costs does economics take into consideration? | Both explicit and implicit. It looks at what you could've done and your costs of doing so. |

| What is an 'opportunity cost'? | The next-highest-valued alternative. |

| What is an 'Implicit Cost'? | Costs that do not require any outlay of money. (i.e. you use your savings to pay for business expenses so your input cost is the fact you are no longer receiving that interest on your savings) |

| Opportunity Costs are = to or > than ... | Explicit Costs. |

| Why is 'Economic Profit' less than 'Accounting Profit'? | |

| Total Opportunity Costs = | Implicit Costs + Explicit Costs |

| In 'qt = f (K, L, N)' what do the inputs stand for? | K = Capitol L = Labour N = Natural Resources |

| A 'Production Function' is... | The output obtainable from any combination of inputs. |

| In the 'Short-run' ... | At least one input is fixed. |

| In the 'Long-run'... | All inputs are fixed. |

| In the 'Very Long-run'... | Technological advancements means that 'f' (what is being produced) can change. |

| Explain 'Diminishing Marginal Product' | The marginal product of an input declines as the quantity of the input increases. |

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.