2898818

| Question | Answer |

| filtration | |

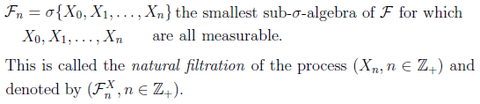

| natural filtration | |

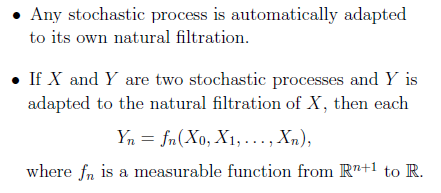

| adapted | |

| blank | |

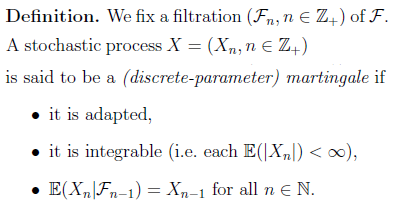

| Martingale (discrete parameter) | |

| submartingale property | |

| supermartingale property | |

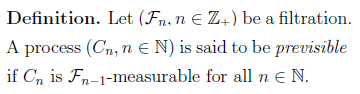

| previsible (filtration) | |

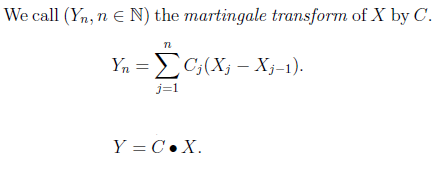

| martingale transform | |

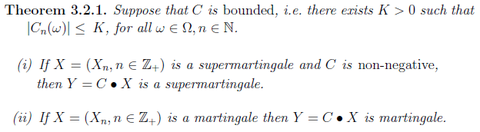

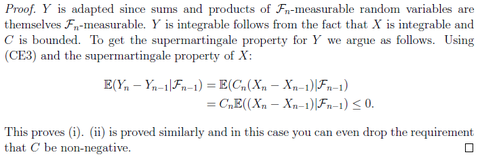

| conditions for the martingale transform being a supermartingale / martingale | |

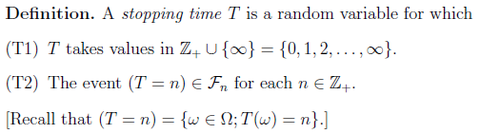

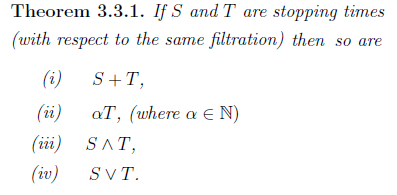

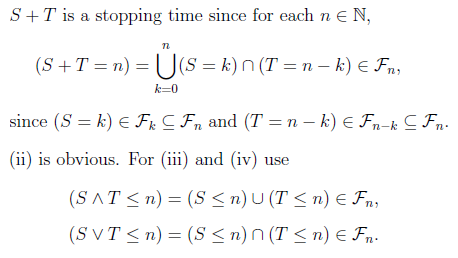

| stopping time | |

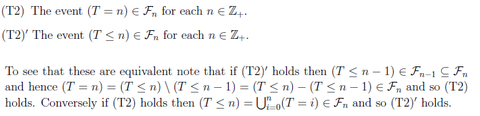

| these are equivalent | |

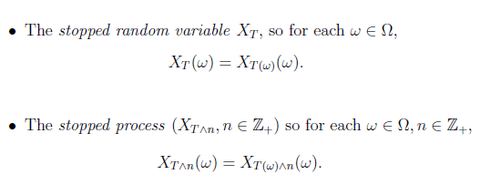

| stopped random variable stopped process | |

| N.B. cannot always take the limit as n tends to infinity and conclude that | |

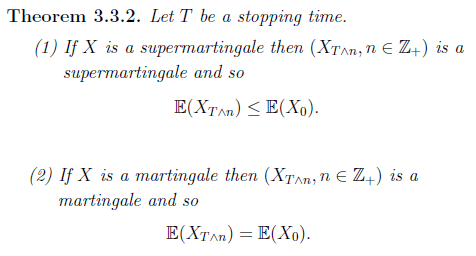

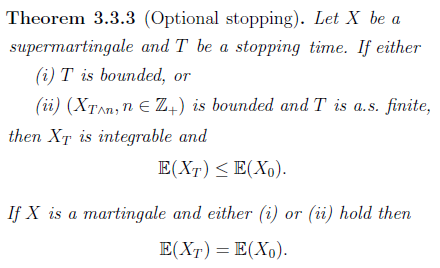

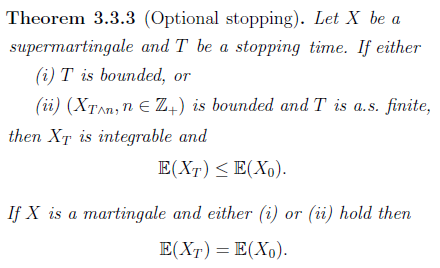

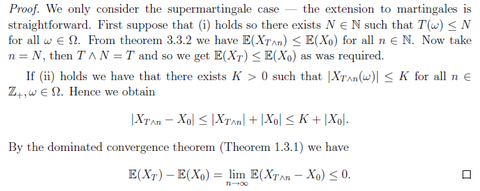

| Doob's Optional Stopping Theorem | |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.