39447369

Description

Flashcards by Dillon Onyemelukwe, updated more than 1 year ago

|

|

Created by Dillon Onyemelukwe

over 1 year ago

|

|

| Question | Answer |

| Approximation of Credit Spread | |

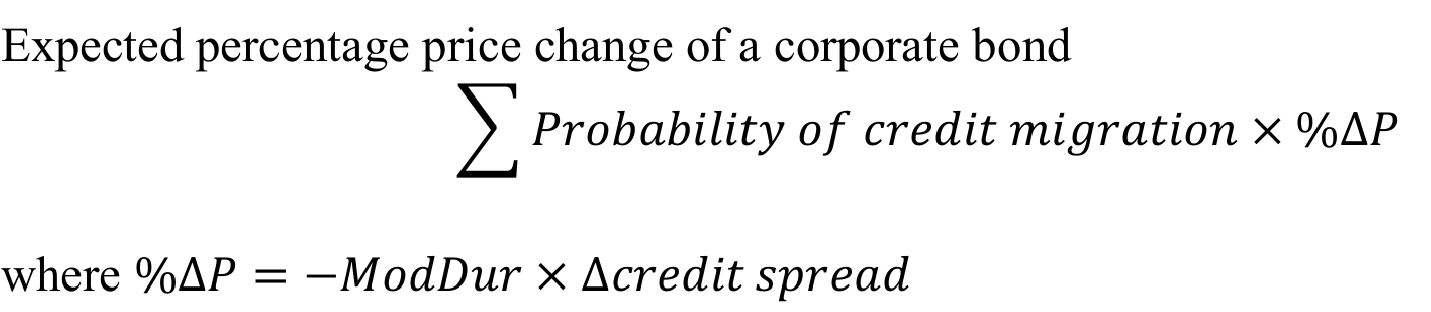

| Price change of bond given credit migration | |

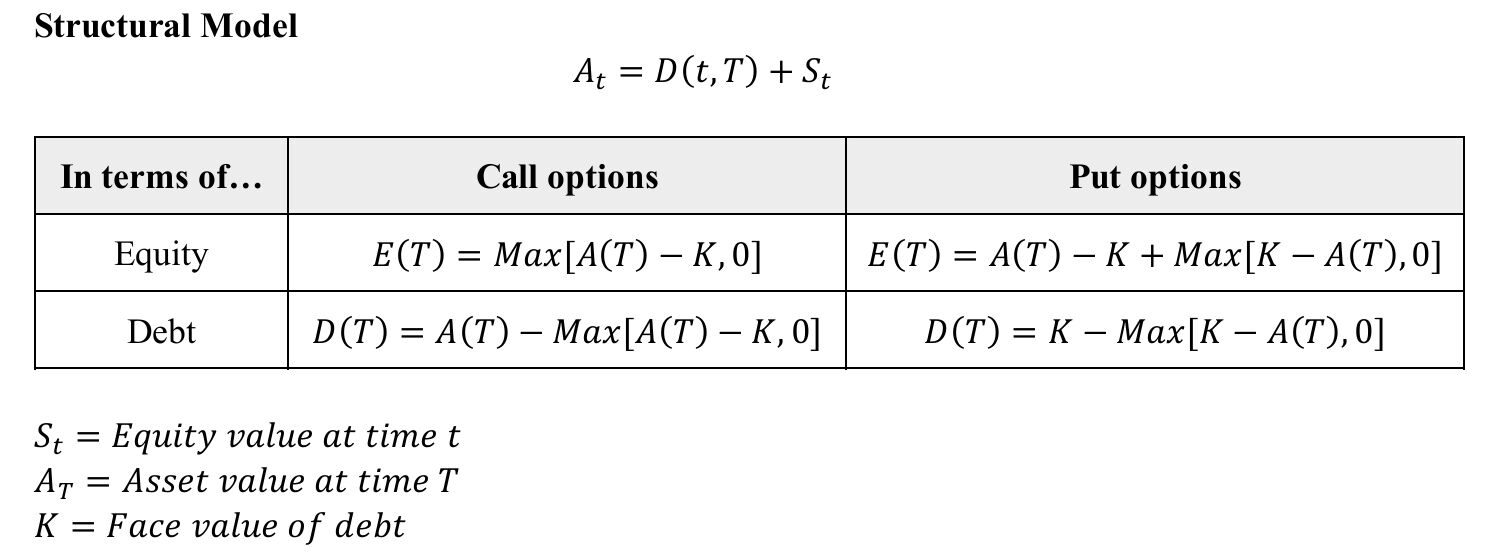

| Structural Model of company debt | |

| CDS Payment Amount | |

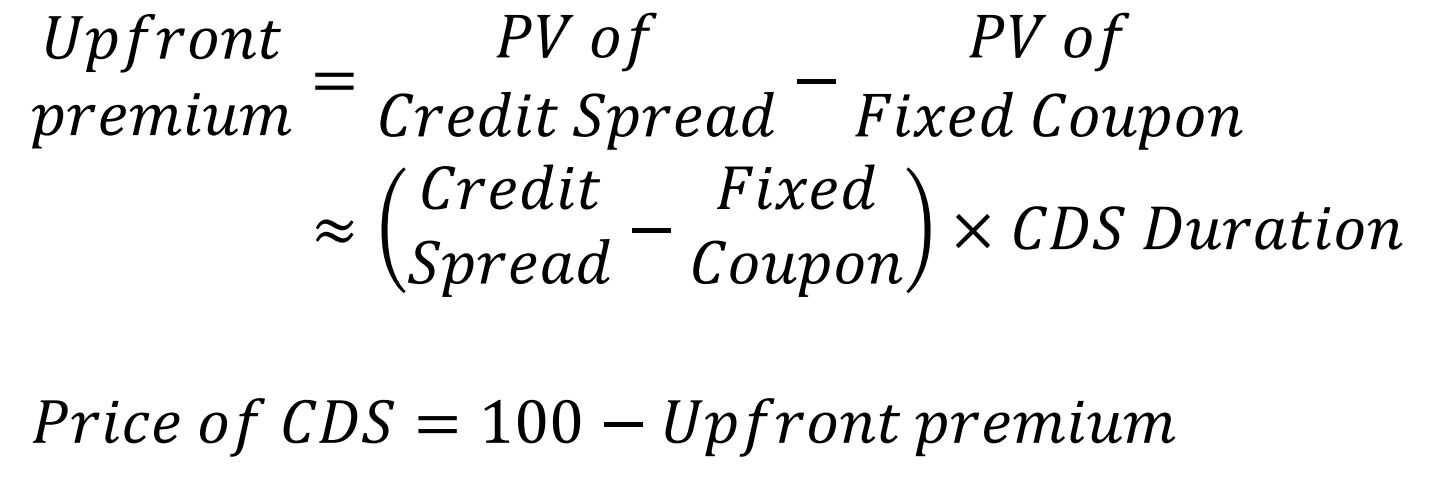

| Price of CDS | |

| % Change in CDS Price | |

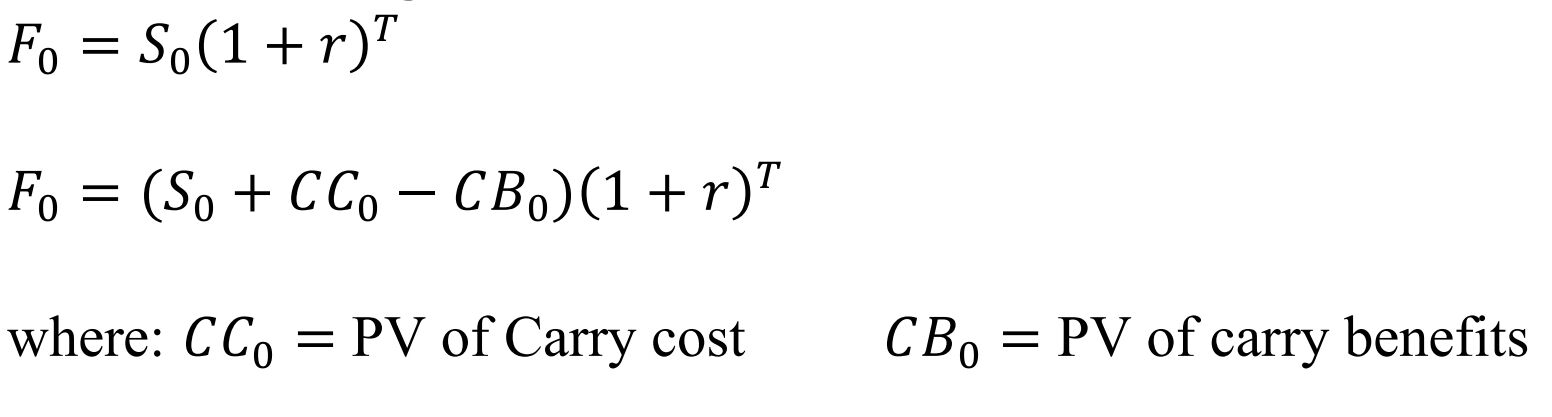

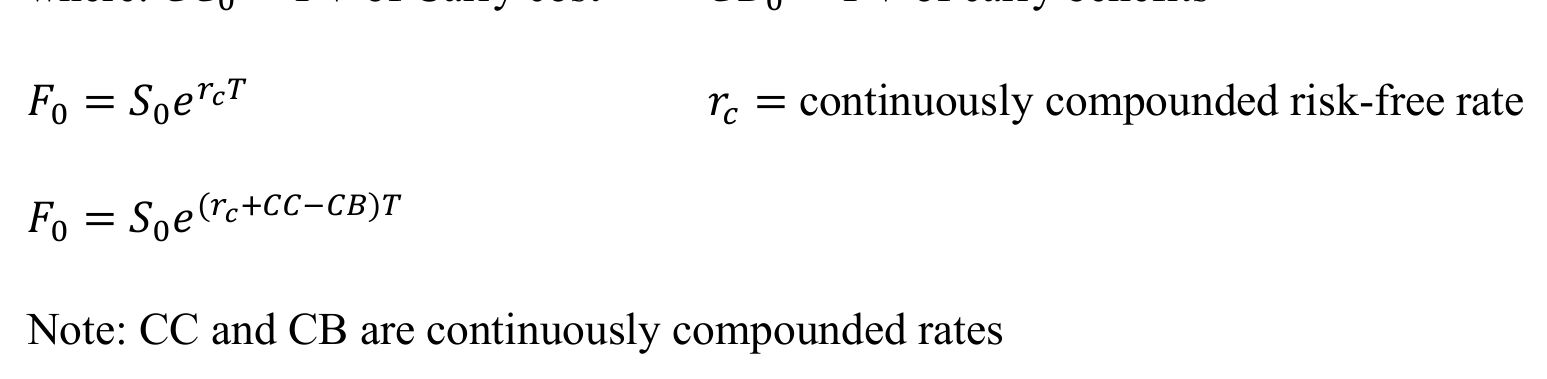

| Forward Pricing | |

| Forward Pricing continuous compounding | |

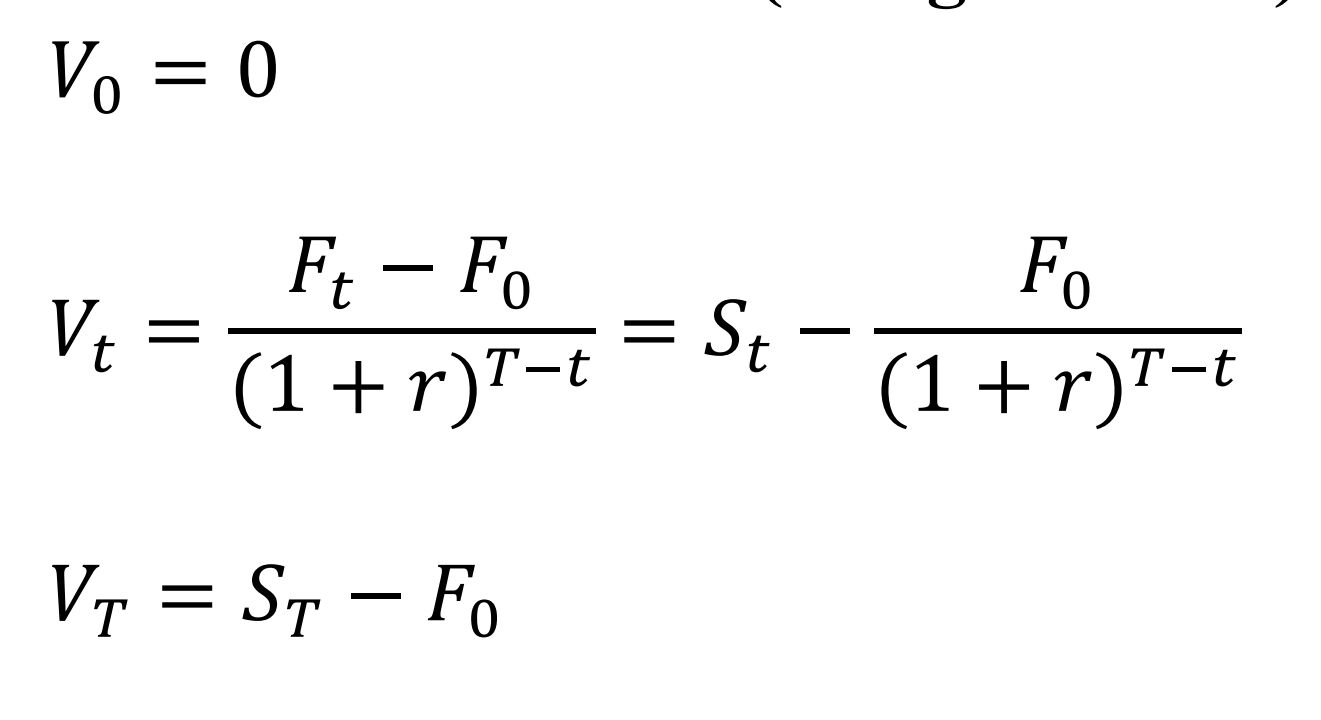

| Forward Valuation Long Position | |

| Long FRA Payoff at expiration | |

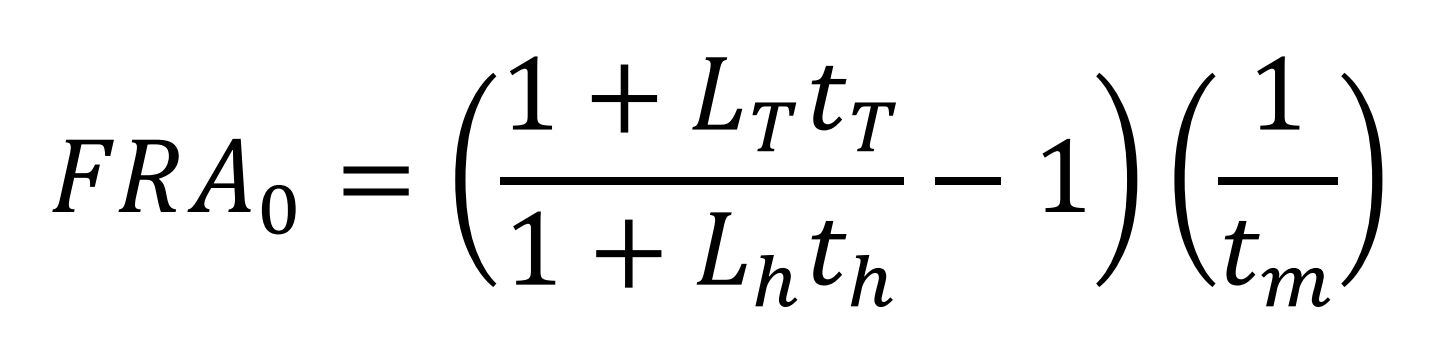

| FRA Price | |

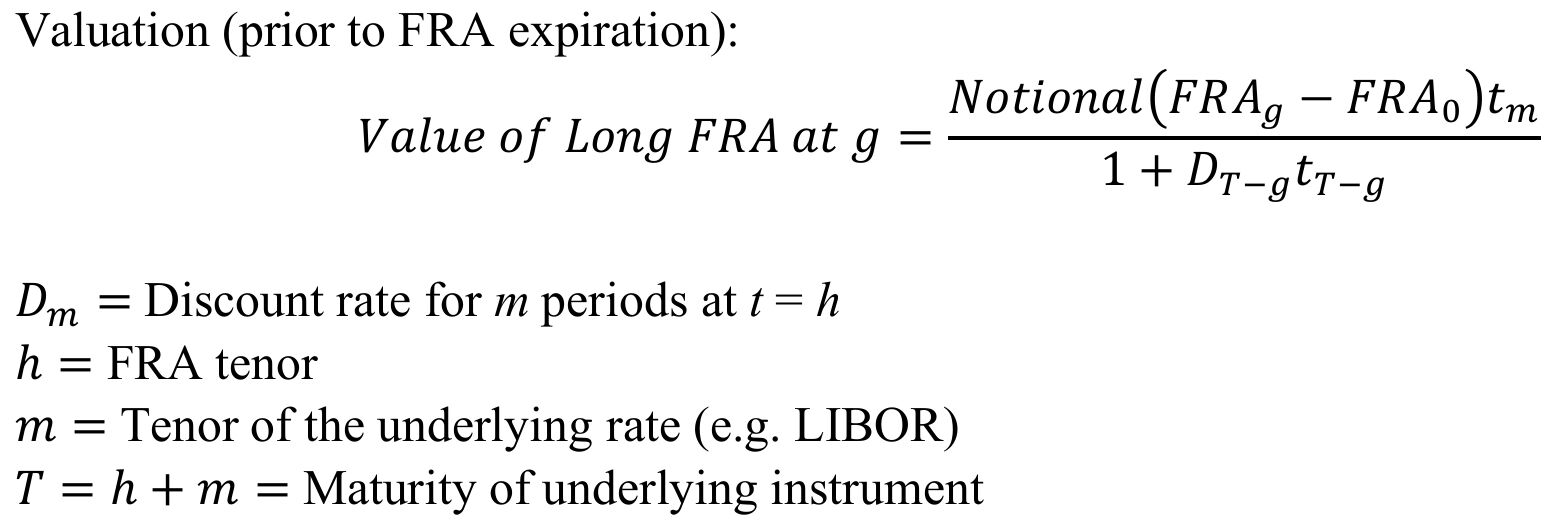

| Value of Long FRA prior to expiration | |

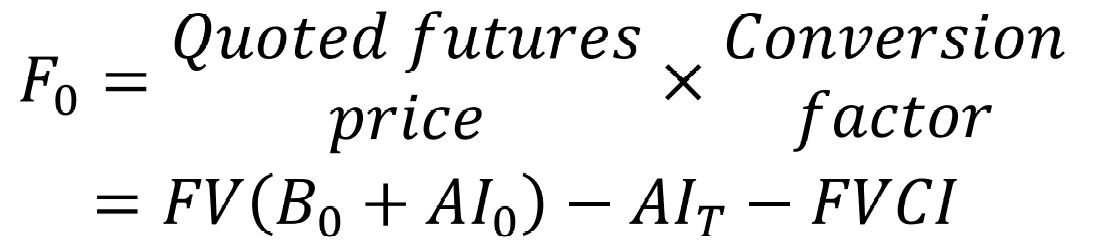

| Price of Bond Forwards | |

| Valuation for bond forward contracts | |

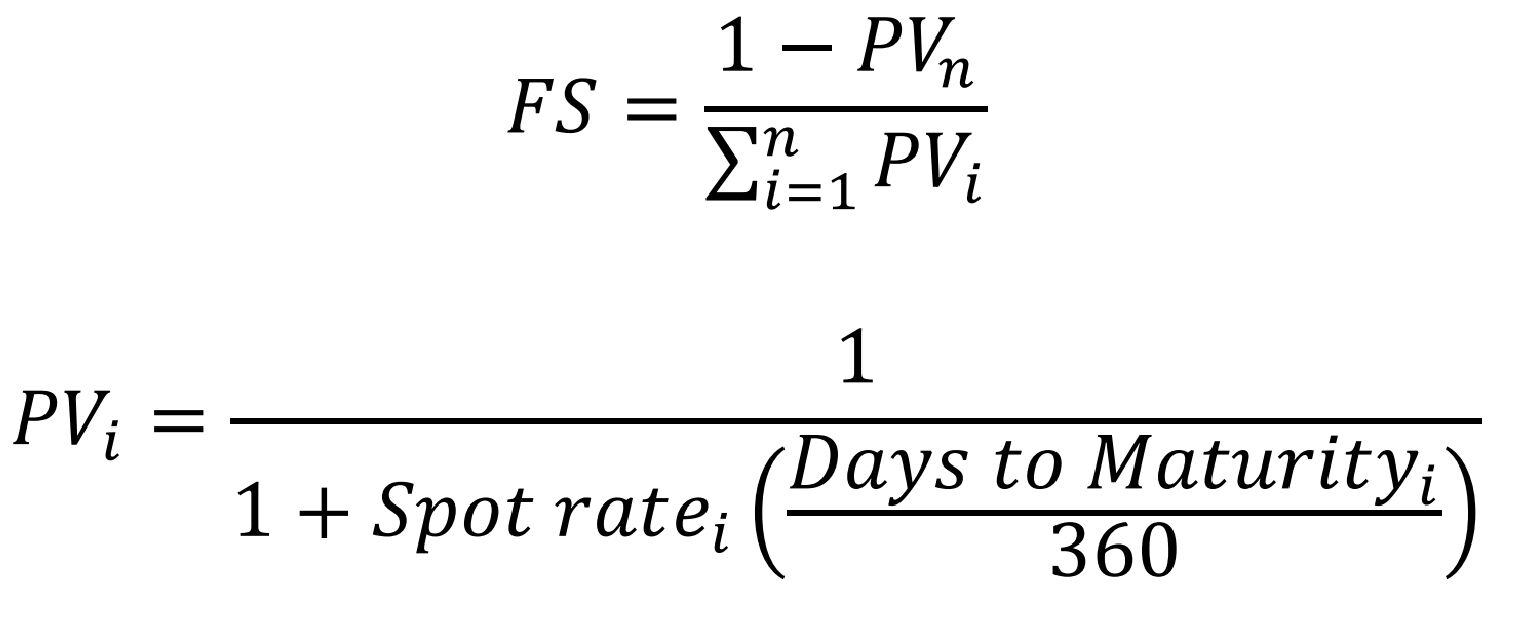

| Pricing of Interest Rate Swaps | |

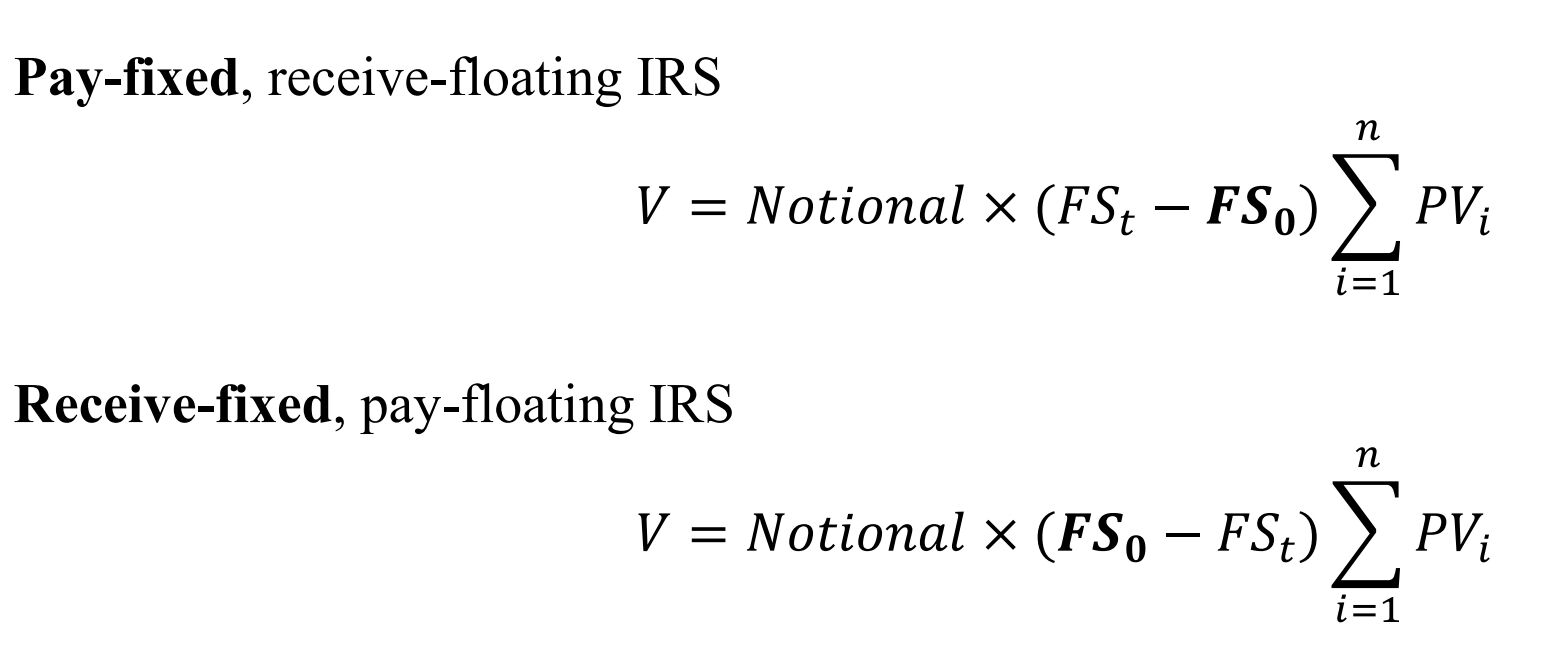

| Valuation of Interest Rate Swaps | |

| Pricing Currency Swap | |

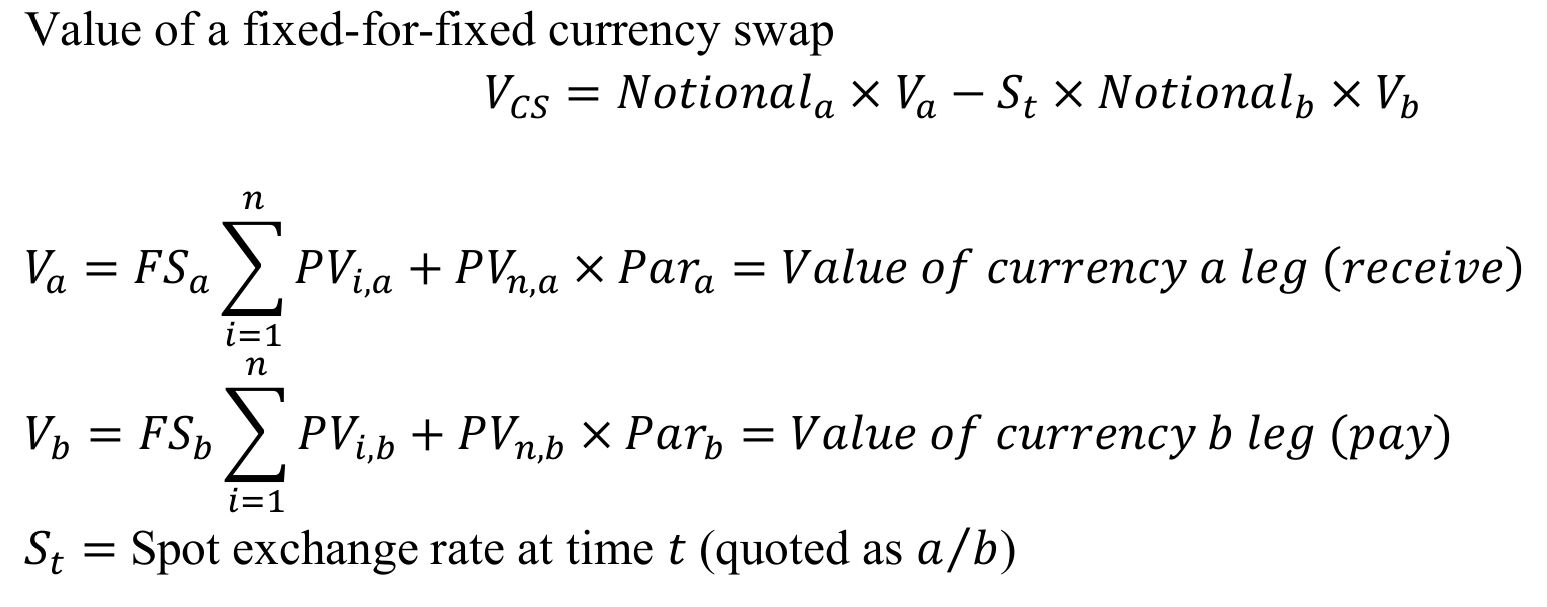

| Valuation of Currency Swap | |

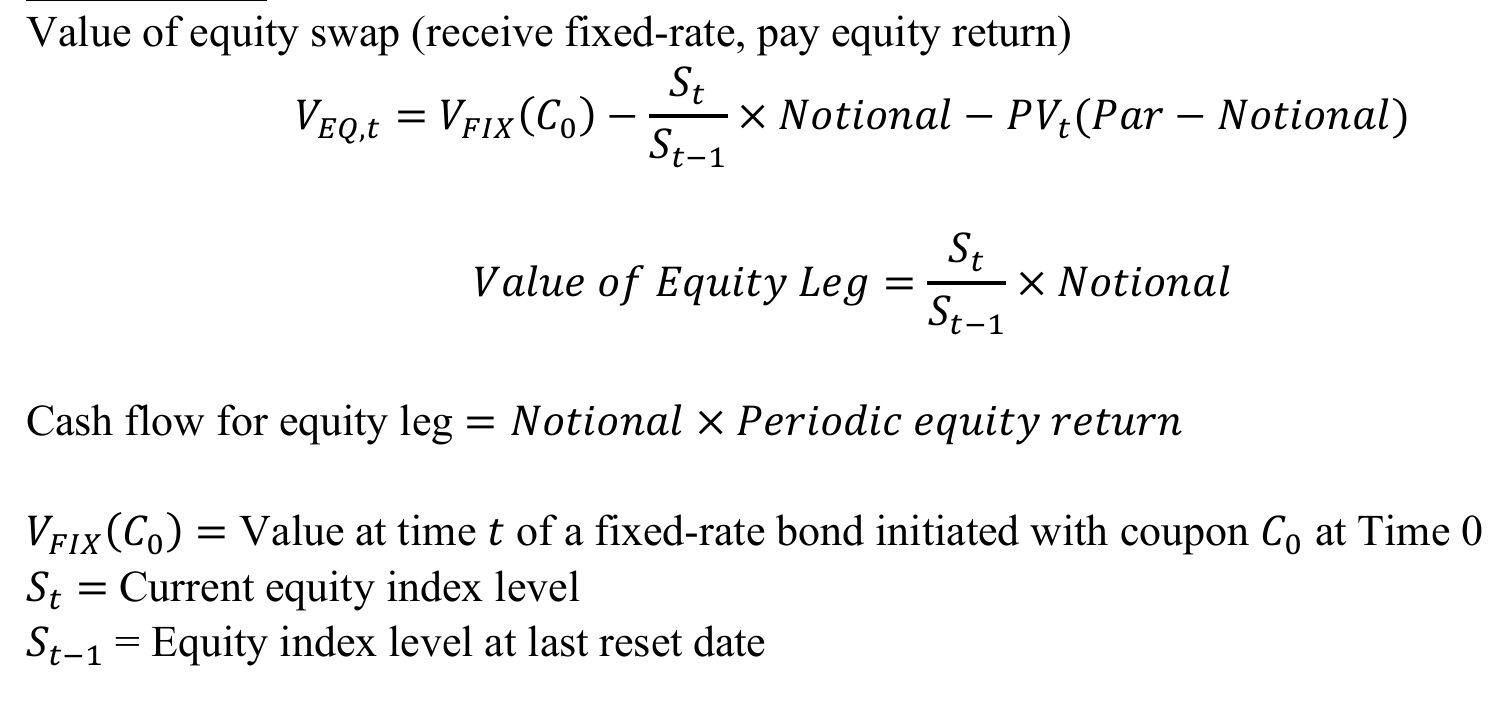

| Value of Equity Swap | |

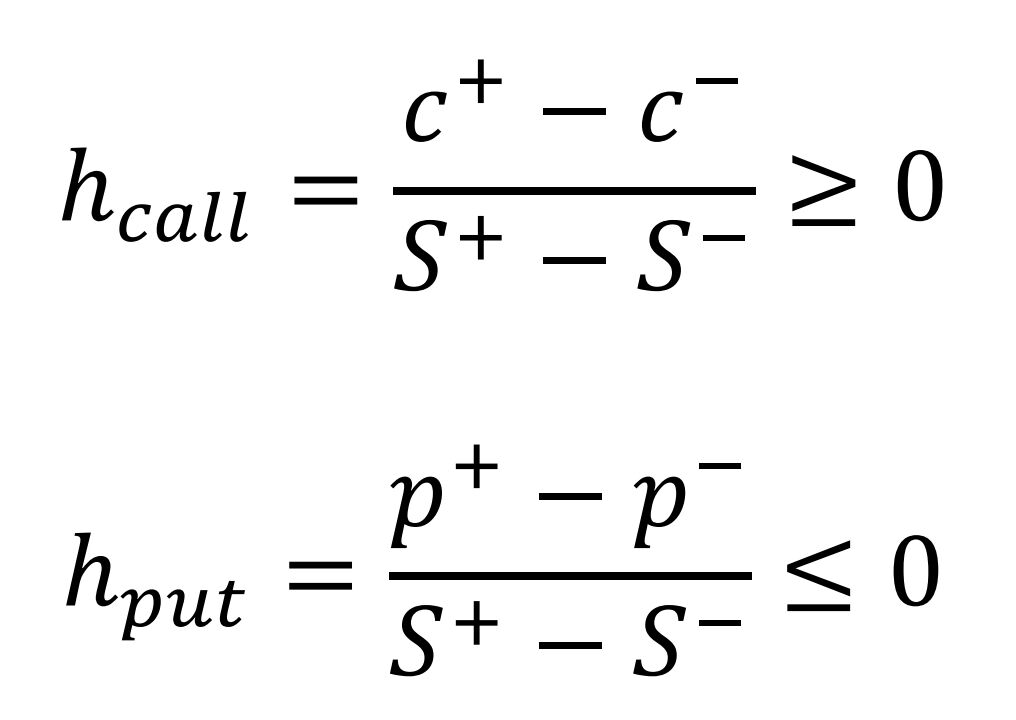

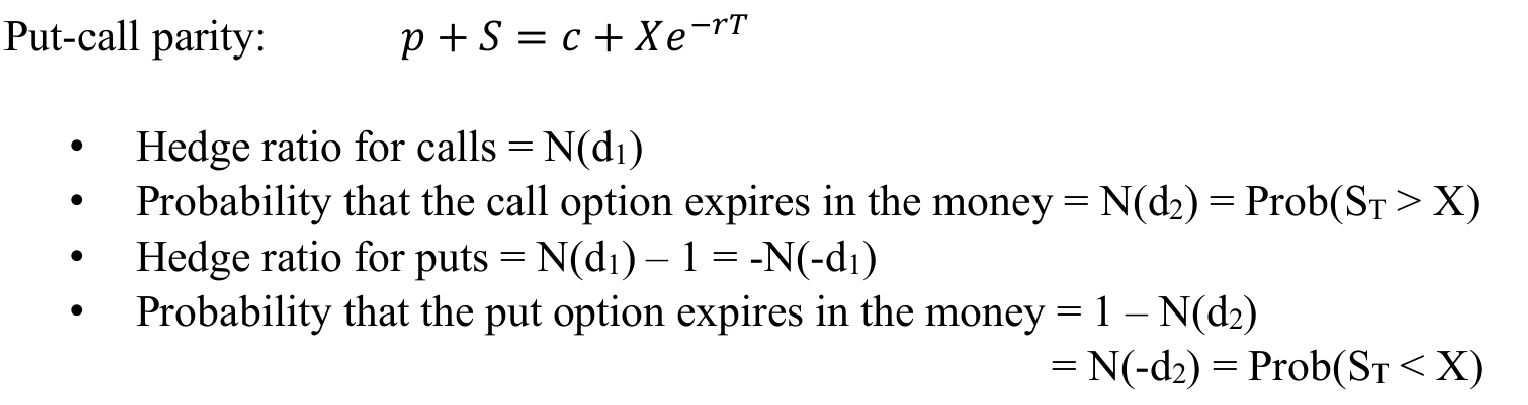

| Hedge Ratio | |

| No arbitrage approach valuing options | |

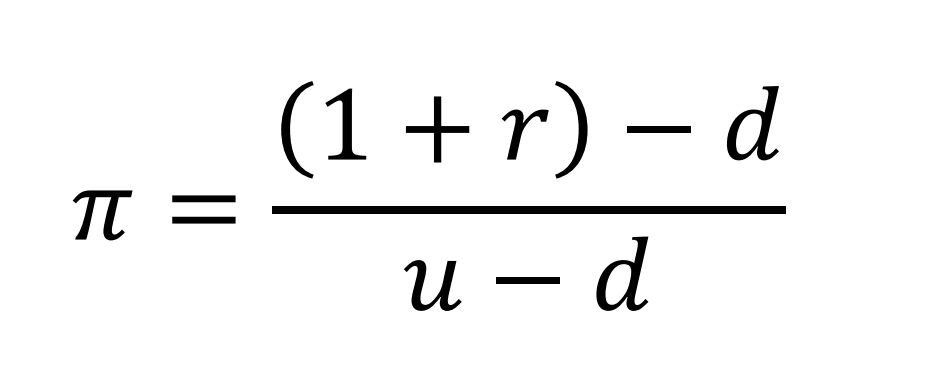

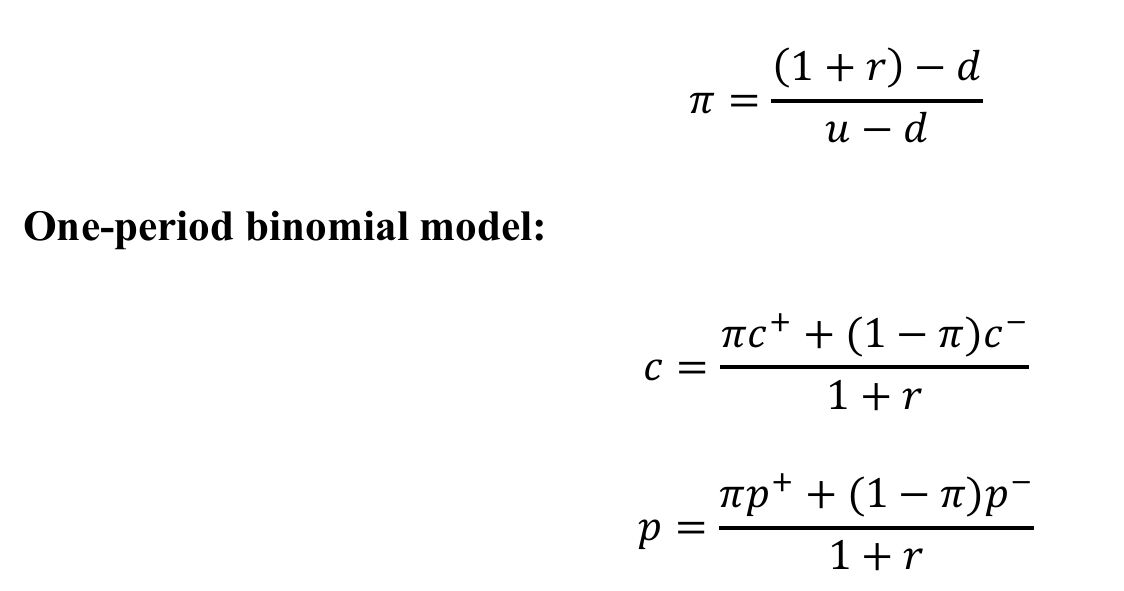

| Risk Free Probability of Default | |

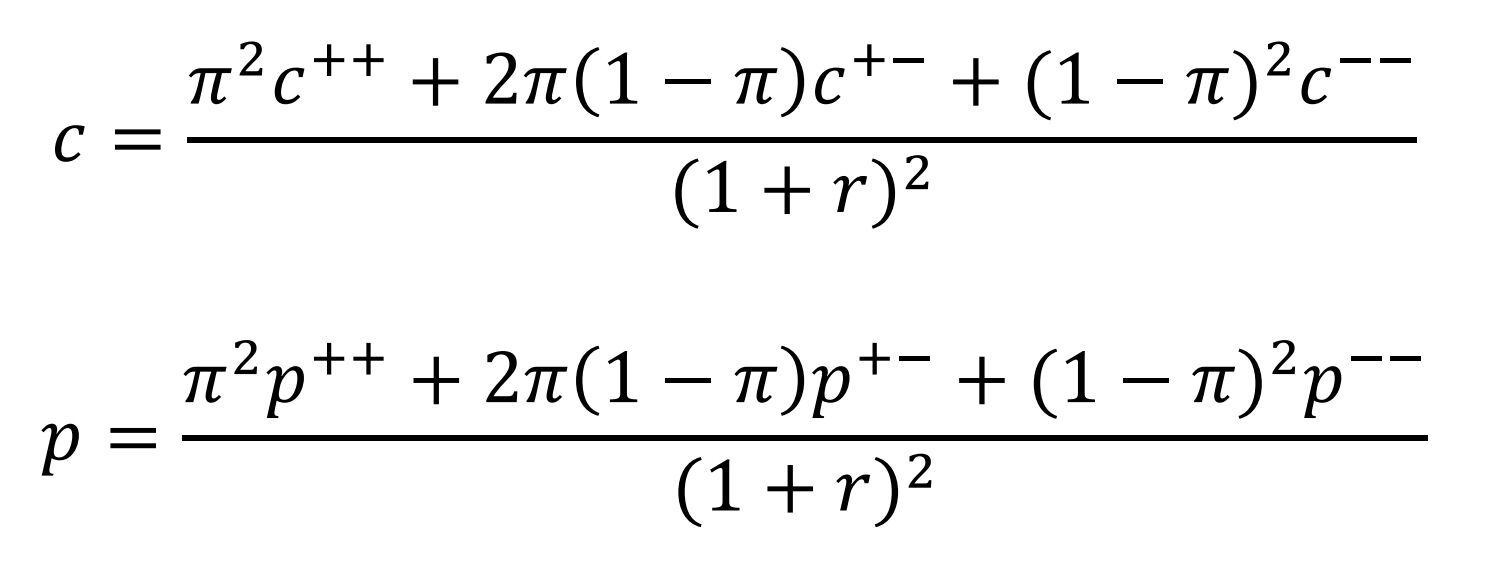

| One period binomial model option | |

| Two period binomial model options | |

| 2 Period America Styled Call Option | |

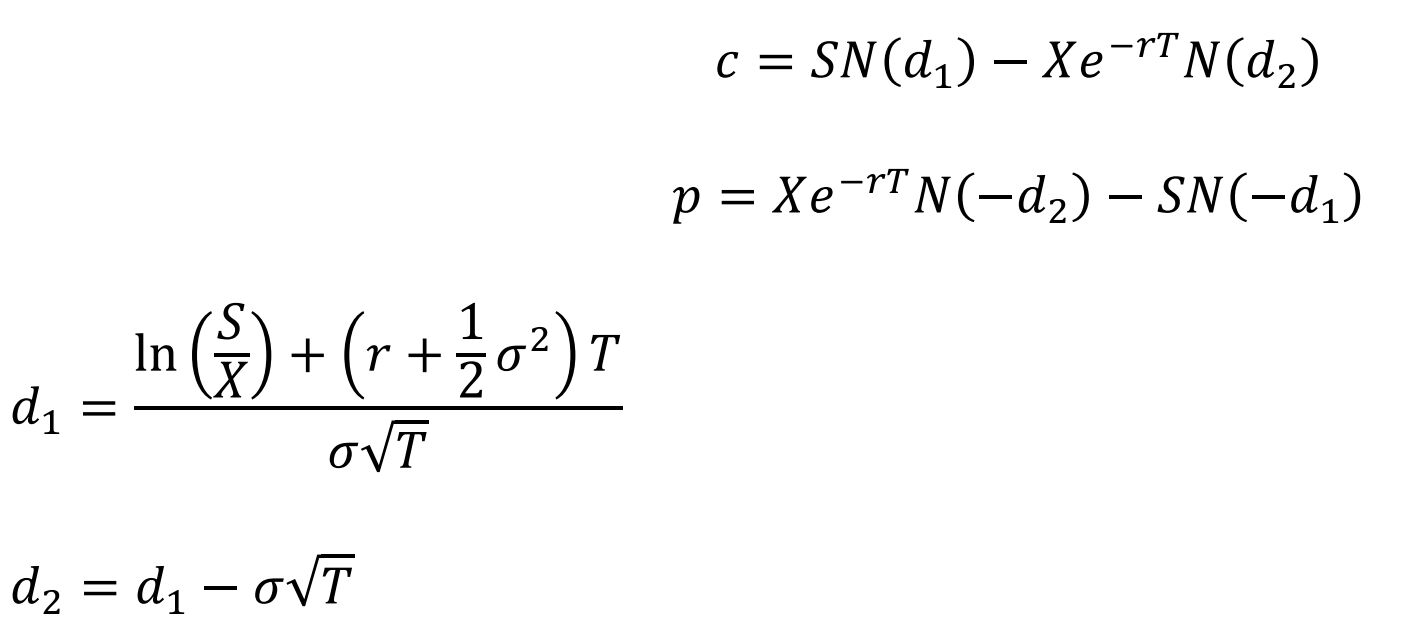

| Black Schools Option Pricing Model | |

| Interpreting BSM | |

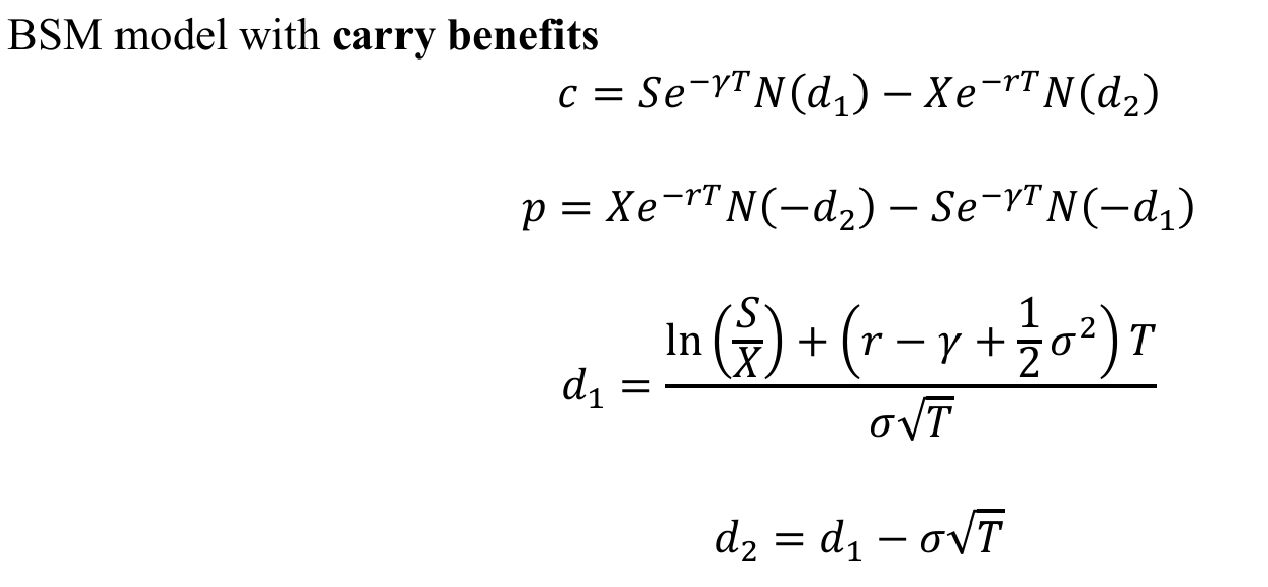

| BSM with carry benefits | |

| Black Option Valuation Model: European Options on Futures | |

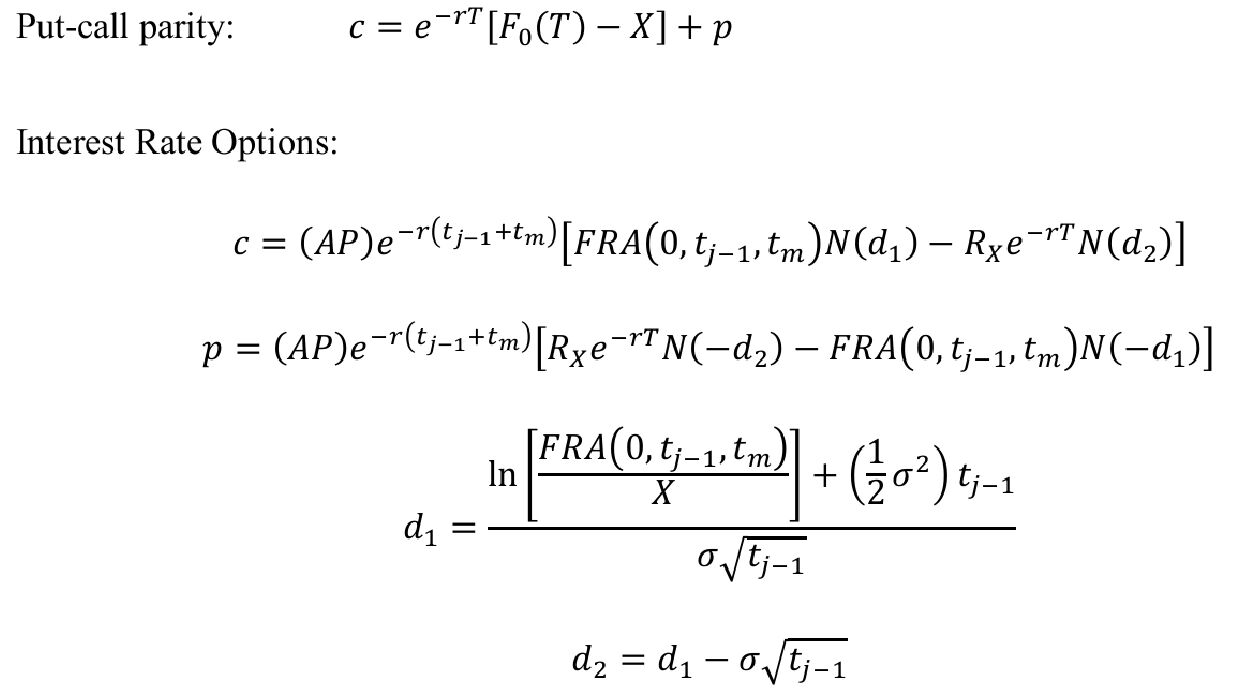

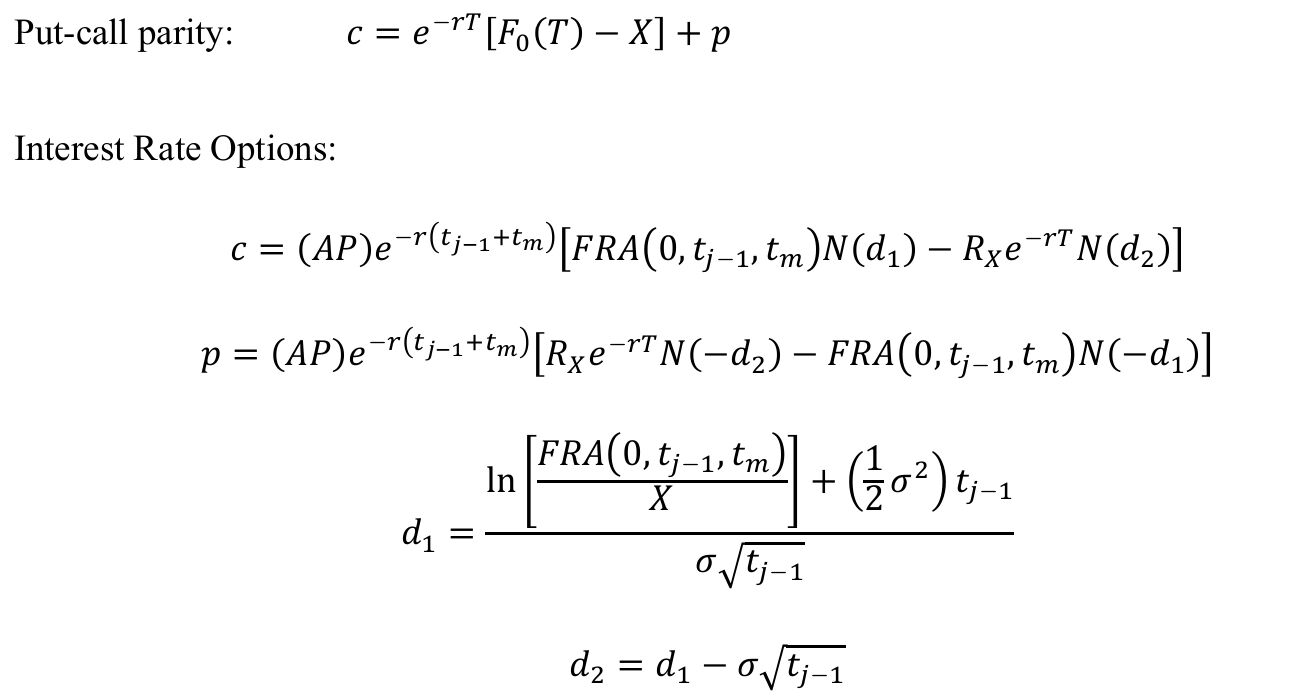

| BSM interest rate options | |

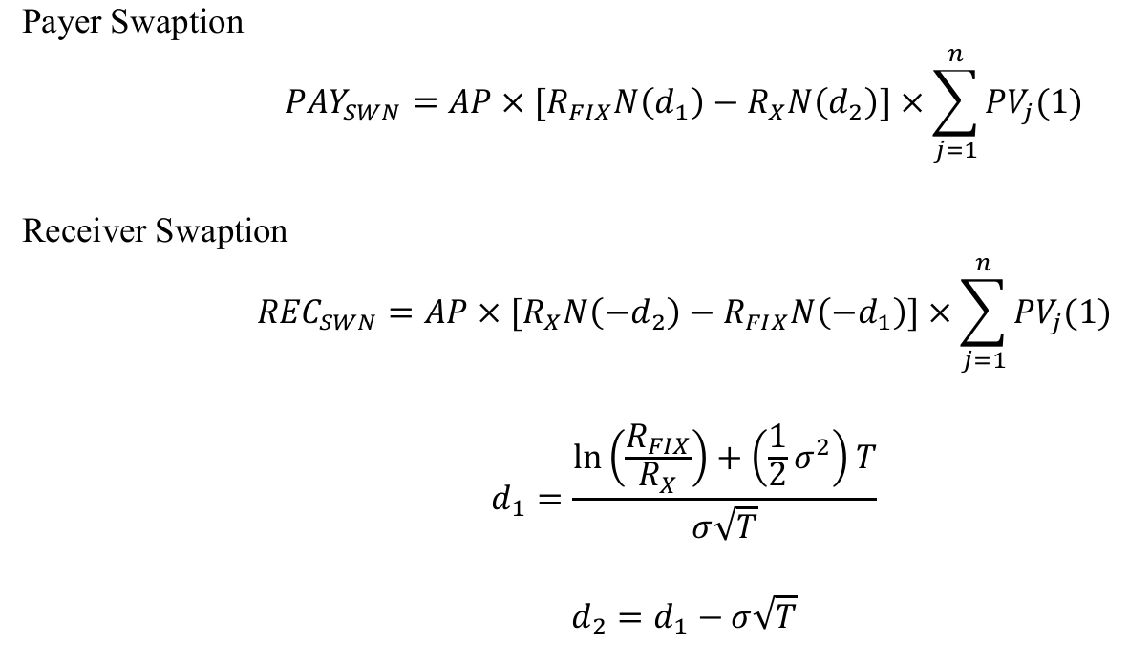

| Swaption | |

| Delta Hedging | |

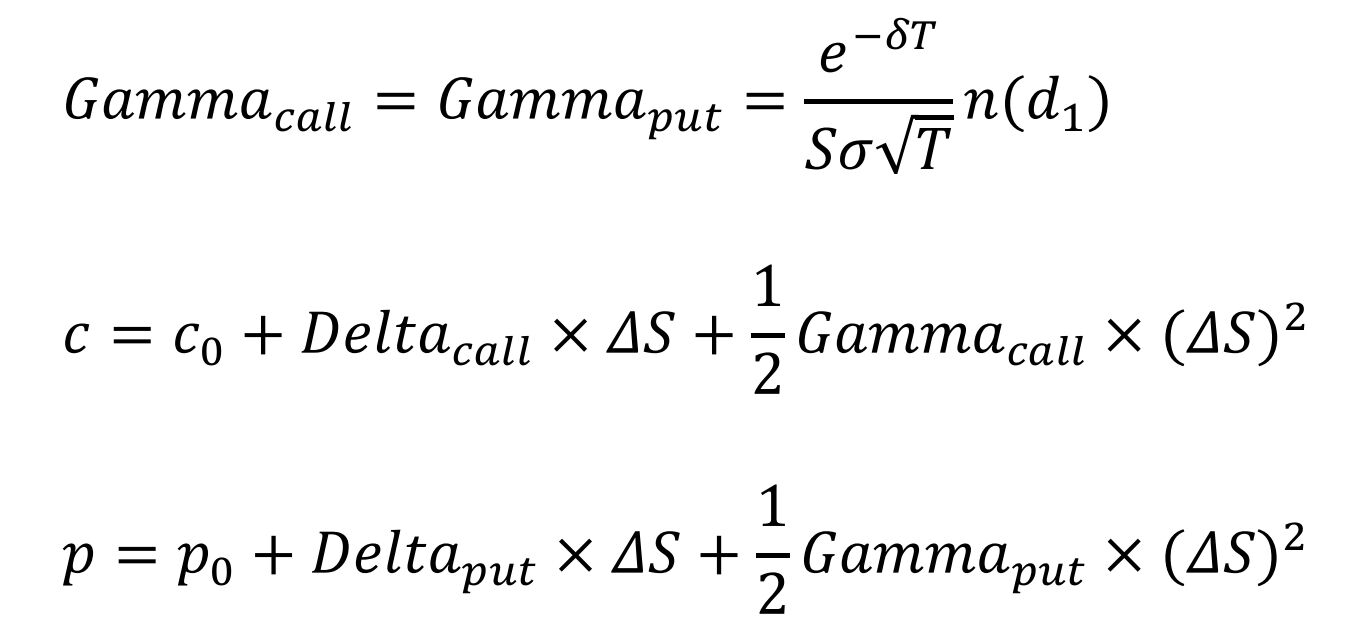

| Valuation of Options with Greeks | |

| Return on Real Estate Investment Index | |

| Implied Land Value | |

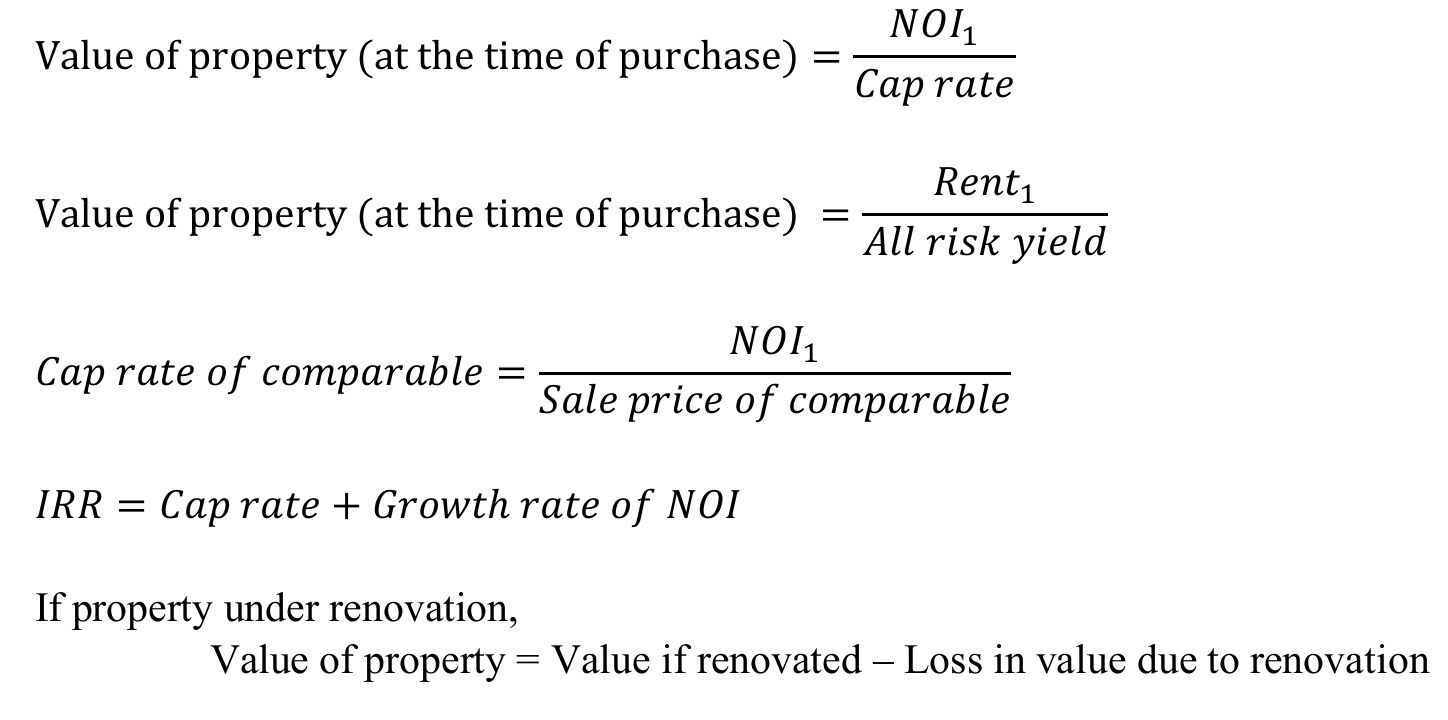

| Direct Capitalization Method | |

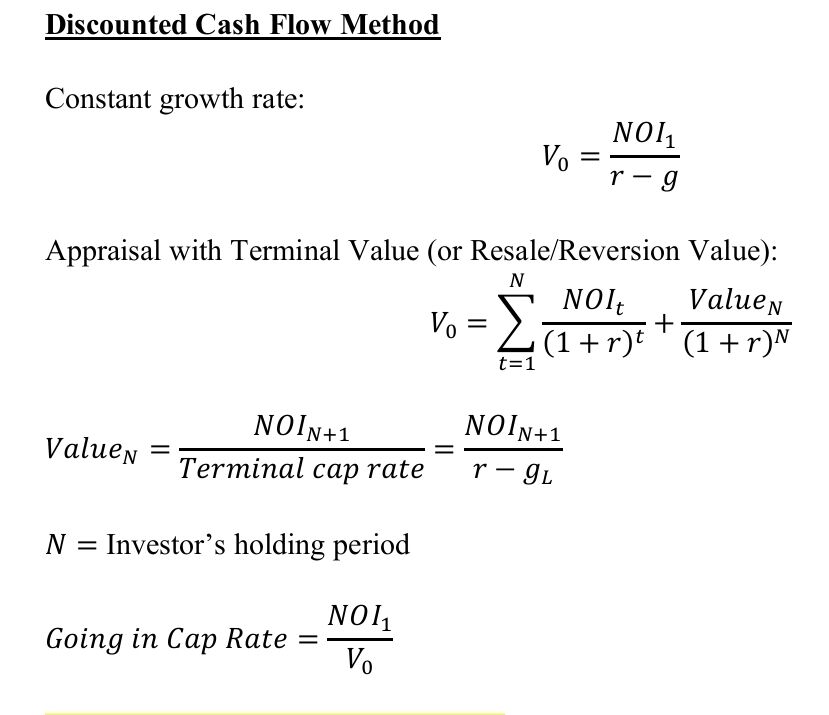

| Discounted Cash Flow Method Valuing real estate | |

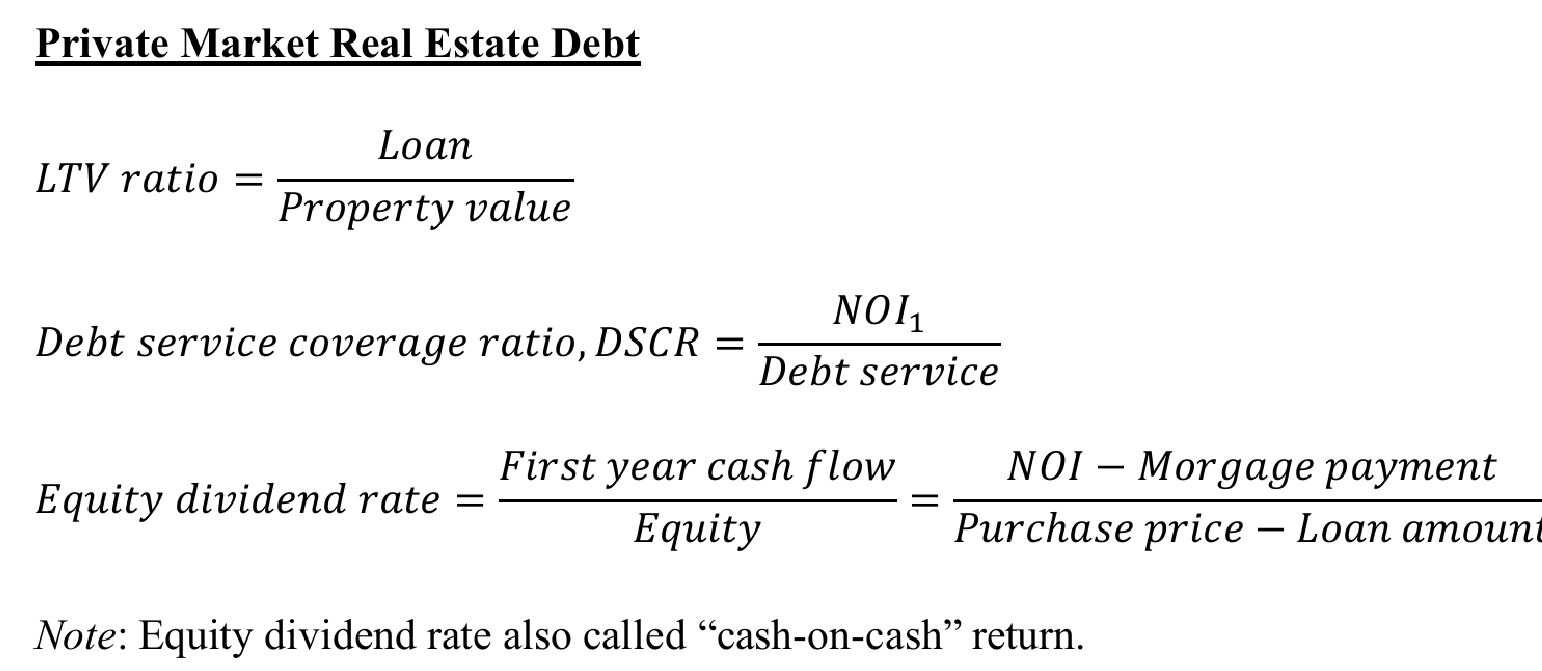

| Private Market Real Estate Debt | |

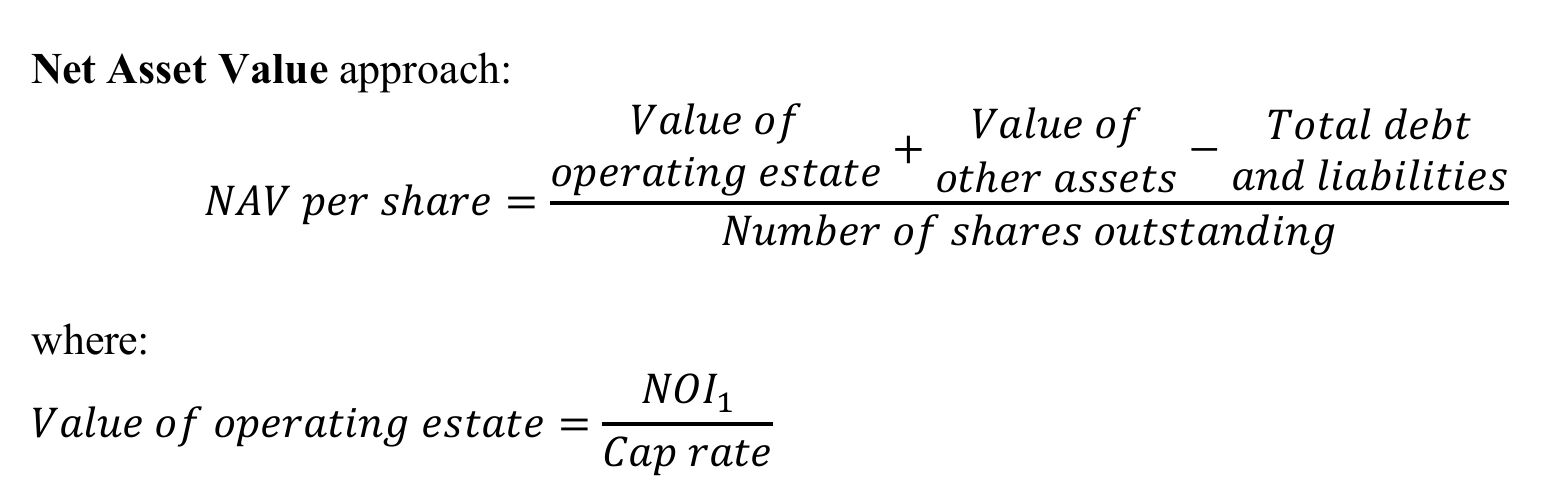

| NAV approach Real Estate | |

| Funds from operations (real estate) | |

| Adjusted Funds From Operations | |

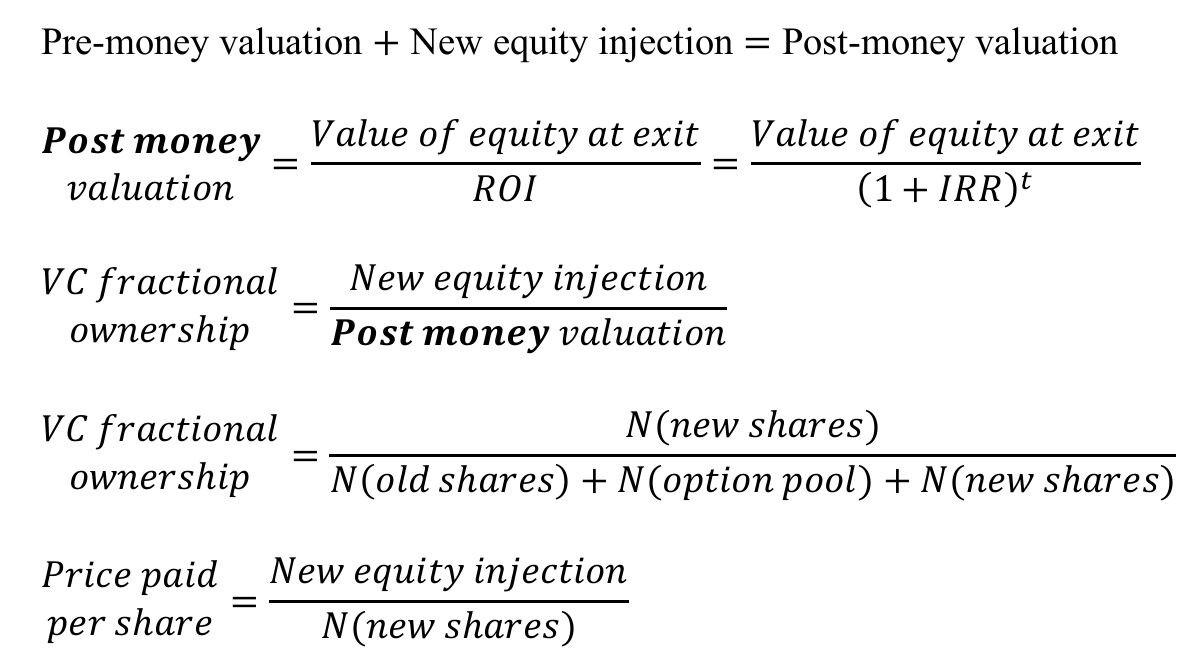

| Venture Capital Method | |

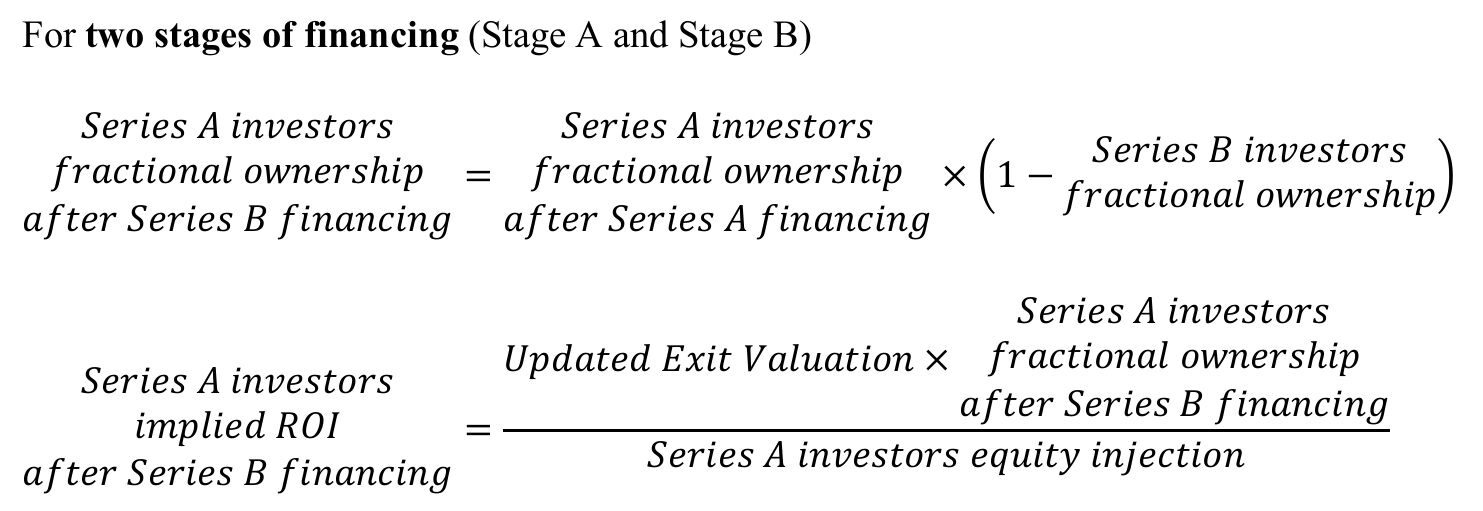

| Two Stages of Financing | |

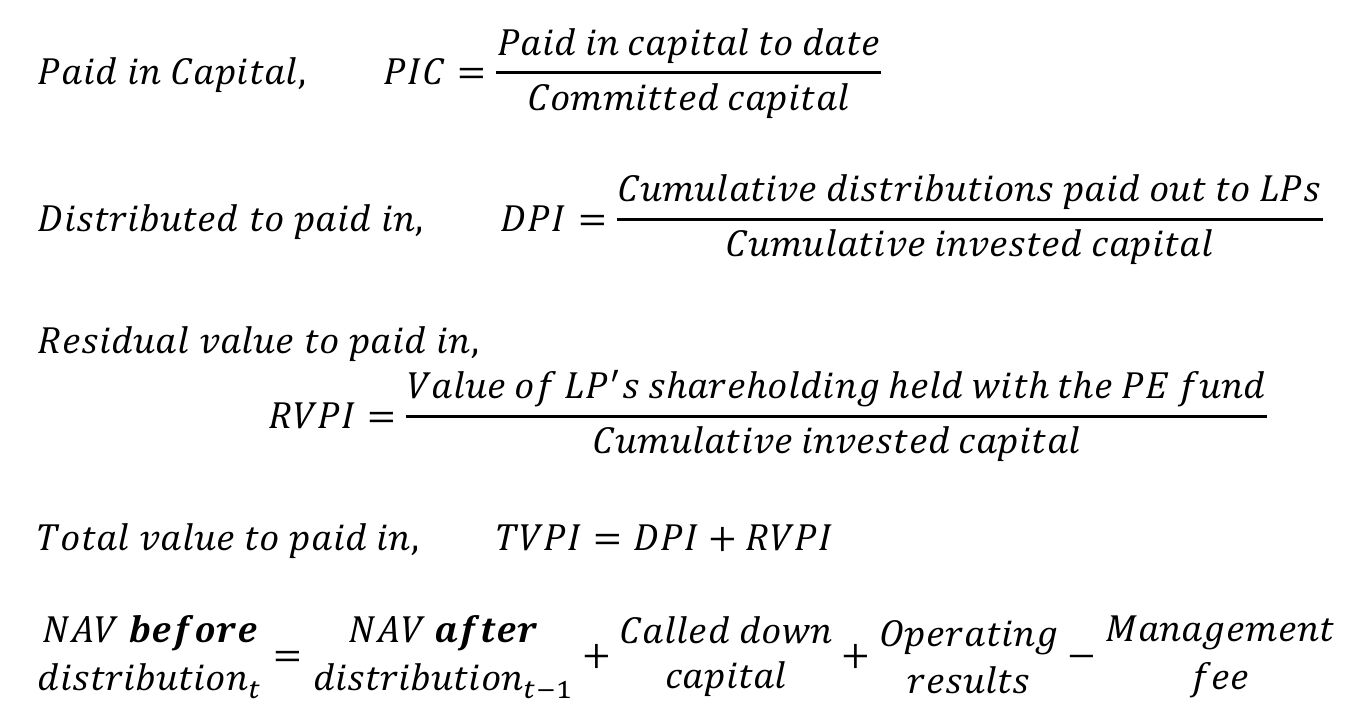

| Return Multiples for Private Equity Funds | |

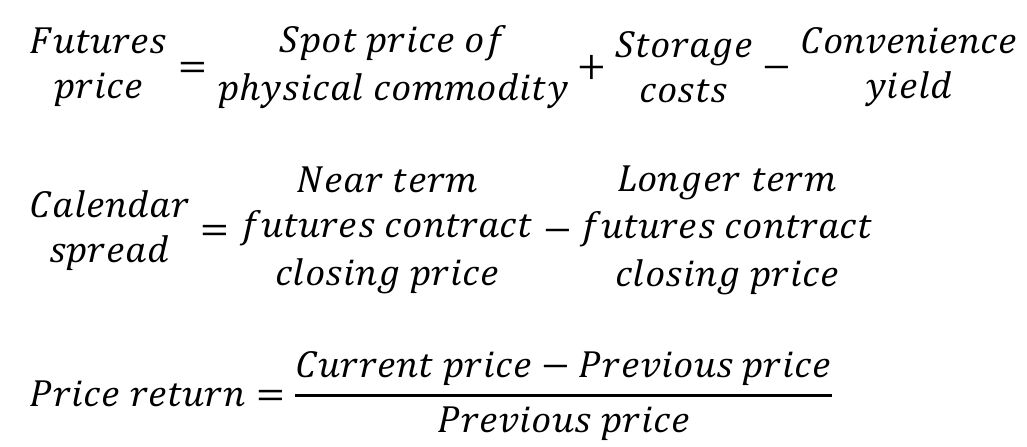

| Commodities Price Return | |

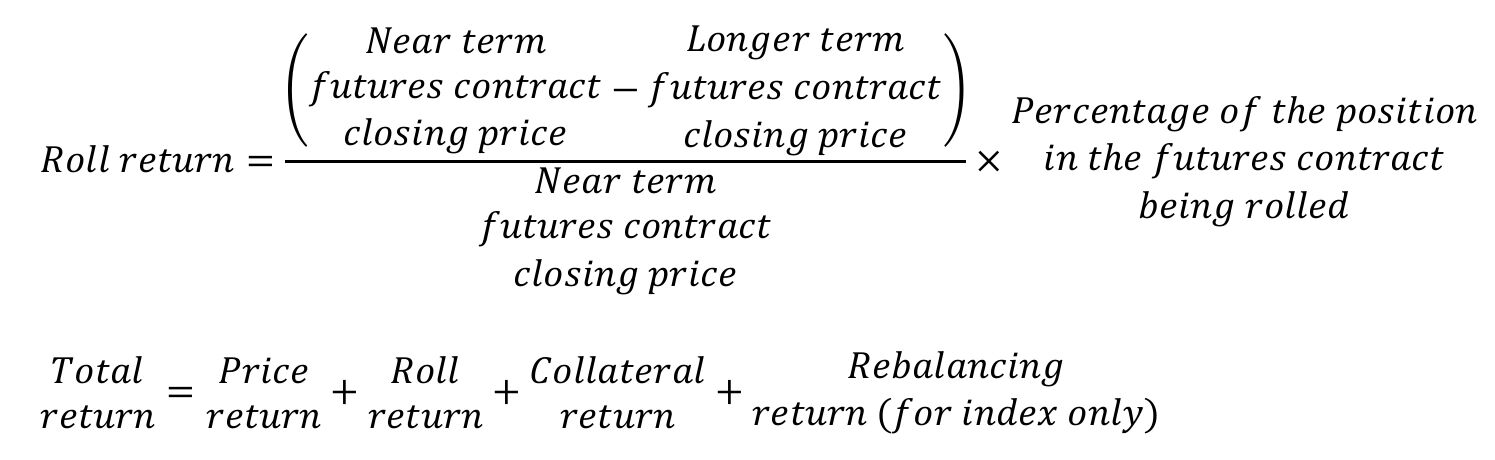

| Commodities Roll Return and Total Return | |

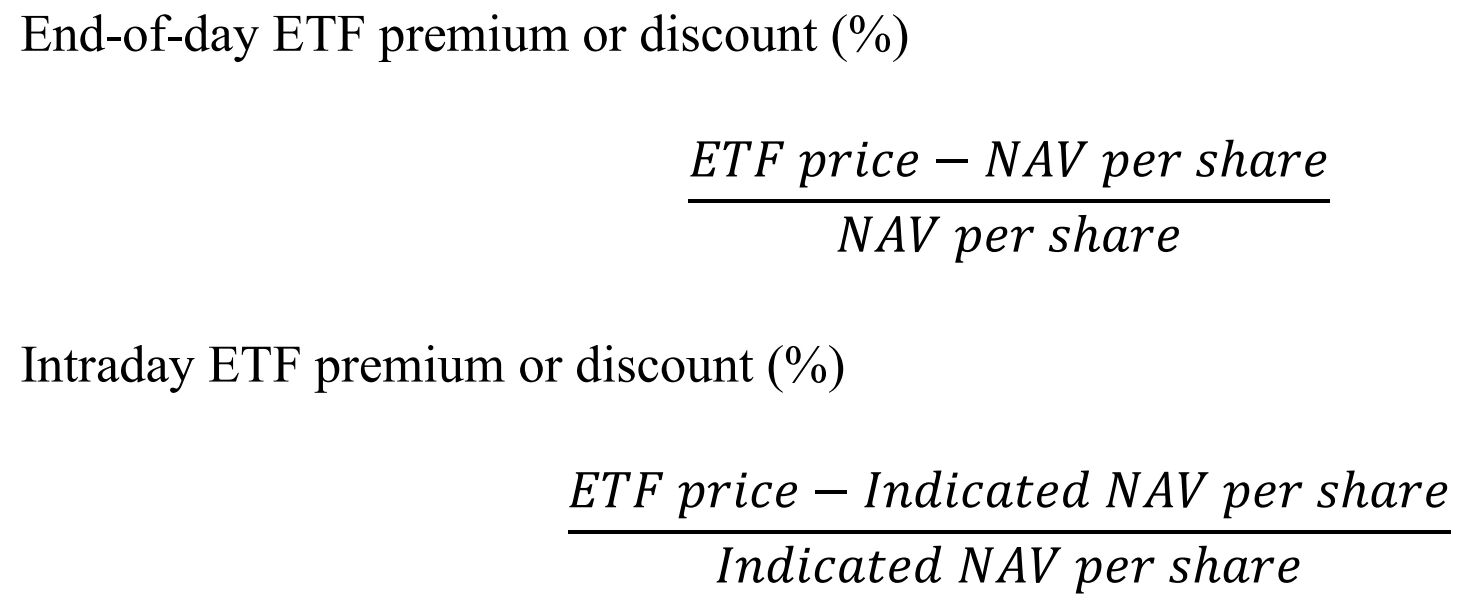

| ETF Premium or Discount |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.