5776246

| Question | Answer |

| 1. What is the best description of the study of economics? | Economics is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity, the incentives that influence those choices, and the arrangements that coordinate them |

| 2. What is included under the topic of microeconomics? | The study of the choices that individuals and businesses make and the way these choices interact and are influenced by governments |

| 3. How do economists characterize choices that are best for the individuals that make them? | Self-interest |

| 4. What is an opportunity cost? | The opportunity cost of something is the best thing you must give up to get it. |

| 5. What do economists call the opportunity cost of a one-unit increase in an activity? | Marginal cost |

| 6. How does the benefit of a one-unit increase in an activity vary as you do more of it? | Marginal benefit is the benefit that arises from a one- unit increase in an activity. The marginal benefit of something is measured by what you are willing to give up to get one additional unit of it. |

| 7. What do economists mean by the term ‘incentive’ | Incentive is a reward or a penalty—a “carrot” or a “stick”—that encourages or discourages an action. |

| 1. What is the difference between consumption and capital goods? | Consumption goods are goods and services that are bought by individuals and used to provide personal enjoyment and contribute to a person’s quality of life. Capital goods are goods that are bought by businesses to increase their productive resources. |

| 2. What are the factors of production? | Land, labor, capital, and entrepreneurship. |

| 3. What is the definition of the phrase ‘factors of production’? | The productive resources that are used to produce goods and services |

| 4. How do developing economies compare to advanced economies in terms of human and physical capital? | The proportion of the population with a degree or that has completed high school is small in developing economies. On-the-job training and experience are also much less extensive in the developing economies than in the advanced economies. The major feature of an advanced economy that differentiates it from a developing economy is the amount of capital available for producing goods and services. The differences begin with the basic transportation system. In the advanced economies, a well-developed highway system connects all the major cities and points of production. |

| 5. In what type of economies does most of the world's population live? | Developing economies |

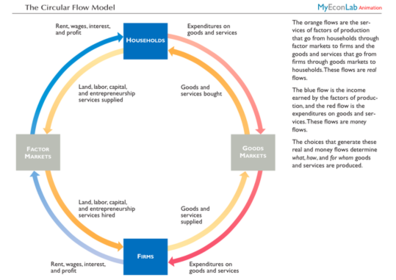

| 6. As shown in the circular flow model, where do the factors of production flow from and to? | |

| 7. What economic decisions are made by firms and what economic decisions are made by households? | |

| 1. How are the attainable production points shown in a production possibilities frontier diagram? | Lies on the curve |

| 2. How is unemployment shown on a production possibilities frontier diagram? | Combinations of the output of consumer and capital goods lying inside the PPF happen when there are unemployed resources or when resources are used inefficiently. |

| 3. (graph) How is opportunity cost calculated, using a production possibility frontier diagram? | Do a ratio between the two products |

| 4. How is the shape of a typical production possibilities frontier related to the opportunity cost of producing a good? | The magnitude of the slope of the PPF measures the opportunity cost. Because the PPF is bowed outward, its slope changes and gets steeper as the quantity of one of the product increases. |

| 5. (graph) How choices leading to economic growth shown on a PPF diagram? | c |

| 6. According to economists, what should a nation do to increase its economic growth? | Decrease consumption, develop better technologies for producing goods and services; improve the quality of labor by education, on-the-job training, and work experience; and acquire more machines |

| 7. What do economists mean by the phrase ‘comparative advantage’? | The ability of a person to perform an activity or produce a good or service at a lower opportunity cost than anyone else. |

| 8. How are the gains from specialization and trade shown on a PPF diagram? | g |

| 1. How are market demand curves are constructed | g |

| 2. What happens to the demand for a good if a complement's price changes? | Its relation is inversely proportional. Lower complement’s price result a left shift of a demand curve. For example, the demand for wrist guards decreases when the price of in-line skates rises. |

| 3. What is the underlying reason for the law of supply? | ? |

| 4. What factors could cause a change in supply | Prices of related goods , Prices of resources and other inputs, Expected future prices , Number of sellers , Productivity |

| 5. (graph) How are shortages and surpluses shown on a demand and supply diagram? | g |

| 6. What factors could cause a change in demand? | Prices of related goods , Expected future prices , Income , Expected future income and credit, Number of buyers, Preferences |

| 7. How are equilibrium price and quantity affected by a change in supply? | ? |

| 1. What does price elasticity of demand measure? | A measure of the responsiveness of the quantity demanded of a good to a change in its price when all other influences on buyers’ plans remain the same. |

| 2. What is the formula for calculating price elasticity of demand? | |

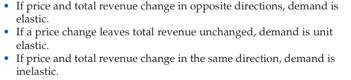

| 3. What happens to a firm’s total revenue when it raises the price of its product? | |

| 4. What is the formula for calculating price elasticity of supply? | |

| graph) How is the elasticity of a supply curve shown graphically? | g |

| 6. What does cross elasticity of demand measure | The cross elasticity of demand is a measure of the responsiveness of the demand for a good to a change in the price of a substitute or complement when other things remain the same |

| 7. How does income elasticity of demand vary between normal and inferior goods | Income elasticity of demand shows how the demand for a good changes when income changes. For a normal good, the income elasticity of demand is positive. For an inferior good, the income elasticity of demand is negative. |

| 1. For economists, what is the difference between value and price? | Value is what people are willing to pay; price is what they must pay |

| 2. What is the definition of consumer surplus | Consumer surplus equals the excess of marginal benefit over price, summed over the quantity consumed |

| 3. What do economists call the cost of producing one more unit of a good or service? | Marginal cost. |

| 4. How do economists define the term ‘cost’? | Cost is what a seller must give up to produce the good, and price is what a seller receives when the good is sold. |

| 5. What determines if a market is efficient? | Marginal benefit equals marginal cost, point where curves intersect. |

| 6. What do we call the loss suffered by society when a market is inefficient? | Deadweight loss |

| 7. To what does the phrase "the big tradeoff" refer? | A tradeoff between efficiency and fairness that recognizes the cost of making income transfers. |

| 1. What do economists use to show the limits to what a consumer can buy? | Budget Line |

| 2. How does a change in price affect a budget line? | If the price of one good rises when the prices of other goods and the budget remain the same, consumption possibilities shrink. If the price of one good falls when the prices of other goods and the budget remain the same, consumption possibilities expand. |

| 3. How does the budget line change if the consumer’s budget increases? | An increase in the budget shifts the budget line rightward. |

| 4. How does total utility change as more of a good is consumed | Total utility is the total benefit that a person gets from the consumption of a good or service. Total utility generally increases as the quantity consumed of a good increases. |

| 5. To what does the phrase ‘marginal utility’ refer? | Marginal utility is the change in total utility that results from a one-unit increase in the quantity of a good consumed. |

| 6. How do economists resolve the paradox of value | Water is more valuable than a diamond because water is essential to life itself. Yet water is much cheaper than a diamond. You can solve this puzzle by distinguishing between total utility and marginal utility. Total utility tells us about relative value; marginal utility tells us about relative price. The total utilities from water are enormous, but remember, the more we consume of something, and the smaller is its marginal utility. We use so much water that its marginal utility—the benefit we get from one more glass of water—diminishes to a small value. Diamonds, on the other hand, have a small total utility relative to water, but because we buy few diamonds, they have a large marginal utility. When a household has maximized its total utility, it has allocated its budget so that the marginal utility per dollar is equal for all goods. Diamonds have a high price and a high marginal utility. Water has a low price and a low marginal utility. When the high marginal utility of diamonds is divided by the high price of a diamond, the result is a marginal utility per dollar that equals the |

| 7. How does marginal utility change as more of a good is consumed? | Marginal utility decreases as we consumer more of a good. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.