2876253

Description

Mind Map by jakeyboihc, updated more than 1 year ago

|

|

Created by jakeyboihc

over 9 years ago

|

|

Business Studies (BUSS2)

- USING BUDGETS

- BUDGET DEFINITION:

An agreed plan

establishing the

expected revenue

and expenditure of

an organisation.

- INCOME BUDGET:

Shows the

planned inflows

to the

organisation

over a period of

time.

- EXPENDITURE BUDGET:

Shows the planned

outflows of the

organisation over

period of time.

- PROFIT BUDGET:

Shows the

planned profit

of the

business over

a period of

time.

- INCOME BUDGET:

Shows the

planned inflows

to the

organisation

over a period of

time.

- GOOD BUDGETING

- Consistent with the

aims of the organisation

- Based on the opinions

of as many people as

possible.

- Challenging but realistic targets

- Consistent with the

aims of the organisation

- VARIANCE ANALYSIS:

This is the process

where the actual

figures are compared

to those that were

budgeted for.

- ADVERSE VARIANCE:

When a business has

done worse than

expected.

- Actual costs were

higher than budgeted

for

- Actual revenue

was lower than

budgeted for

- Actual costs were

higher than budgeted

for

- FAVOURABLE VARIANCE:

When a business has

done better than

expected.

- Actual costs were

lower than

budgeted for

- Actual revenue was

higher than

budgeted for

- Actual costs were

lower than

budgeted for

- ADVERSE VARIANCE:

When a business has

done worse than

expected.

- BUDGET DEFINITION:

An agreed plan

establishing the

expected revenue

and expenditure of

an organisation.

- IMPROVING CASH FLOW

- CASH FLOW DEFINITION:

The flow of money in and

out of a business.

- RECAP ON CASH FLOW:

Cash flow forecast is a

prediction. Cash flow

statement is the actual.

Used by managers, owners

& lenders.

- SOLUTIONS

- Increase sales revenue

- Reduce costs

- Increase sales revenue

- CAUSES OF CASH FLOW PROBLEMS

- Seasonality

- Poor financial planning

- Poor debtor management

- Poor creditor management

- Overheads unmanageable

- Seasonality

- CASH FLOW DEFINITION:

The flow of money in and

out of a business.

- MEASURING & INCREASING PROFIT

- RECAP:

- Profit = Revenue - Costs

- Gross Profit = Revenue - Cost of Sales

- Net Profit = Revenue - All Costs

- Profit = Revenue - Costs

- NET PROFIT MARGIN:

The amount of profit

that an organisation is

making expressed as a

%.

- CALCULATED:

Net Profit /

Turnover x100

- The greater the profit margin,

the better the organisation is

performing.

- Need to pick out from the income

statement the figures require to

conduct this.

- CALCULATED:

Net Profit /

Turnover x100

- GROSS PROFIT MARGIN:

The amount of profit an

organisation is making on

each item sold, expressed

as a %

- CALCULATED:

Gross Profit /

Turnover x 100

- The greater the gross profit

magin, the better the

orgainisation is performing

- This profit margin should

always be greater than the net

profit margin

- CALCULATED:

Gross Profit /

Turnover x 100

- RETURN ON CAPITAL: This is the % return on

capital invested. Typically this could be used

to measure the return your getting from your

investment in the business.

- CALCULATED:

Net Profit /

Capital Invested

x 100

- CALCULATED:

Net Profit /

Capital Invested

x 100

- IMPROVING PROFITABILITY

- iNCREASE SELLING PRICE

- Reduce demand

- Depends on price elasticity

- Reduce demand

- REDUCE COSTS

- Reduce quality

- Damage reputation

- Reduce added value

- Reduce quality

- iNCREASE SELLING PRICE

- RECAP:

- OPERATIONAL TARGETS:

QUALITY

- QUALITY DEFINITION:

A quality product is one

that meets the

customers expectations

and would be fit for

purpose.

- QUALITY CONTROL (QC):

This is the process of

inspecting the product at

the end of the production

process. Typically

completed using a

sample of products.

- QUALITY ASSURANCE (QA):

This is the system that ensures

that quality standards are

being met throughout the

production process. Typically

completed using a sample of

products.

- QC OR QA?

- Quality control tends to

be cheaper in the short

term, due to reduced

training requirements &

reduced employee

responsibility.

- Quality control can

lead to more

wastage.

- Quality assurance can

increase motivation.

- Quality assurance can

actually identify specific

problems in the production

process.

- Quality control tends to

be cheaper in the short

term, due to reduced

training requirements &

reduced employee

responsibility.

- QC OR QA?

- QUALITY CONTROL (QC):

This is the process of

inspecting the product at

the end of the production

process. Typically

completed using a

sample of products.

- QUALITY DEFINITION:

A quality product is one

that meets the

customers expectations

and would be fit for

purpose.

- EFFECTIVE OPERATIONS:

CUSTOMER SERVICE

- CUSTOMER SERVICE DEFINITION:

This is the service given to

customers before, during and

after purchase to a standard that

meets the customers

expectations.

- EXAMPLES OF CUSTOMER SERVICE

- Offering advice pre sales

- Ensuring the item about

to be purchased meets

the customer needs

- Help lines to answer

questions after

purchase

- Dealing with customer

issues fairly and

successfully

- Offering advice pre sales

- HOW DO BUSINESSES GO ABOUT

MEETING CUSTOMER

EXPECTATIONS?

- MARKET RESEARCH:

Surveys, questionnaires

focus groups.

- TRAINING:

Staff know

what makes

good

customer

service

- QUALITY, ASSURANCE & CONTROL:

Ensuring staff get it right the first

time.

- MARKET RESEARCH:

Surveys, questionnaires

focus groups.

- MONITORING CUSTOMER SERVICE:

It's important for an organisation to

monitor its levels of customer

service.

- Typically they will use:

- Satisfaction surveys

- Focus groups

- Tracking surveys

- Online/mobile surveys

- Satisfaction surveys

- Typically they will use:

- IMPROVING CUSTOMER SERVICE

- Improve quality of products/service

- Value customers

- Speed of service

- Friendliness of service

- Efficient dealing with complaints

- Staff trained and competent

- Improve quality of products/service

- CUSTOMER SERVICE DEFINITION:

This is the service given to

customers before, during and

after purchase to a standard that

meets the customers

expectations.

- WORKING WITH SUPPLIERS

- SUPPLIERS

- These are organisations

who provide your

business with a product or

service.

- Typically you want to establish a

good relationship with your

suppliers.

- Suppliers can be critical to

the overall success of your

organisation.

- These are organisations

who provide your

business with a product or

service.

- FACTORS TO CONSIDER

WHEN CHOOSING A

SUPPLIER

- Quality of materials/service supplied

- Flexibility

- Reliability

- Value for money

- Technological investment

- Payment terms

- Quality of materials/service supplied

- GOOD SUPPLIERS:

The benefits of a

good supplier

should be

- IMPROVED CUSTOMER SERVICE:

Delivery on time, good quality of

product/service

- LOWER COSTS:

Good discounts

from economies

of scale

- FLEXIBLE:

Able to deal

with changes

in demand

- IMPROVED CUSTOMER SERVICE:

Delivery on time, good quality of

product/service

- SUPPLIERS

- TECHNOLOGY IN OPERATIONS

- ROBOTICS

- PRODUCTION OF PRODUCTS (CAM)

- ADVANTAGES:

Increased production

speed, Improved

quality, Don't get

bored, Don't take

breaks

- DISADVANTAGES:

Expensive to purchase,

Not flexible, Could

demotivate existing

employees

- ADVANTAGES:

Increased production

speed, Improved

quality, Don't get

bored, Don't take

breaks

- PRODUCTION OF PRODUCTS (CAM)

- AUTOMATION STOCK CONTROL

- JUST IN TIME (JIT)

- ADVANTAGES:

Reduced wastage,

Reduced storage

space, Improved cash

flow, More accurate

forecasting

- DISADVANTAGES:

Expensive to setup,

Dependant on good

supplier relationship,

Doesn't take into account

external factors

- ADVANTAGES:

Reduced wastage,

Reduced storage

space, Improved cash

flow, More accurate

forecasting

- JUST IN TIME (JIT)

- COMMUNICATION TECHNOLOGY

- INTERNET/EMAIL

- ADVANTAGES:

Reduced wastage,

Increased efficiency,

Improved

communication

channels, Increased

opportunities for

outsourcing

- DISADVANTAGES:

Training required for

employees, Cost of

investing in equipment,

Increased considerations

in the management of its

use

- ADVANTAGES:

Reduced wastage,

Increased efficiency,

Improved

communication

channels, Increased

opportunities for

outsourcing

- INTERNET/EMAIL

- COMPUTER AIDED DESIGN (CAD)

- DISADVANTAGES:

Training required for

employees, Cost of

investing in software,

Software could be used by

rivals

- ADVANTAGES:

More efficient,

Enables

competitive

advantage,

Reduces lead time

between design

and production,

Reduced need for

physical

prototypes

- DISADVANTAGES:

Training required for

employees, Cost of

investing in software,

Software could be used by

rivals

- BENEFITS OF TECHNOLOGY

- Reduced unit costs

- Improved communication

- Quicker operations processes

- Improved quality

- Reduced wastage

- Reduced unit costs

- ROBOTICS

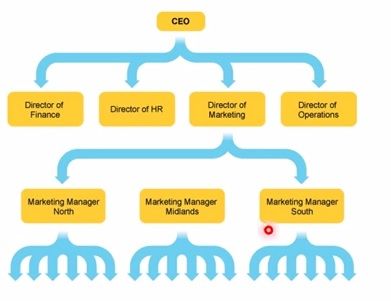

- ORGANISATIONAL STRUCTURE:

- DEFINITION:

The ways jobs,

responsibilities

and power is

organised

within a

business

- LAYERS OF HIERARCHY:

Levels of management

- CHAIN OF COMMAND:

Lines of authority in the

organisation

- SPAN OF CONTROL:

Number of subordinates

who a manager directly

controls

- LAYERS OF HIERARCHY:

Levels of management

- HIERARCHAL:

Tall & flat,

Traditional

methods, provide

promotion

opportunites

- MATRIX:

Based around

projects,

People from

each

functional

area working

as a team

- ENTREPRENEURIAL:

Central control from

owner, Quick decisions

with small team around

them

- WORKFORCE ROLES

- SUPERVISORS:

Employees with control

for one or more

subordinate

- TEAM LEADERS:

Employees responsible

for leading a team of

employees

- MANAGERS:

Employees who are

responsible for the

operation of a specific

area of the business

- DIRECTORS:

Appointed persons

by the share-holders

to run the

organisations

- SUPERVISORS:

Employees with control

for one or more

subordinate

- DEFINITION:

The ways jobs,

responsibilities

and power is

organised

within a

business

- EFFECTIVENESS OF WORKFORCE

- LABOUR TURNOVER:

Number of leavers per year

/ Average of number of

employees for year x 100

- LABOUR PRODUCTIVITY:

Total value of output /

Total number of

employees

- LABOUR TURNOVER:

Number of leavers per year

/ Average of number of

employees for year x 100

- RECRUITMENT, TRAINING & SELECTION

- RECRUITMENT PROCESS

- Identify the vacancy

- Write a job description /

personal specification

- Advertise position

- Receive and process applications

- Identify the vacancy

- TYPES OF RECRUITMENT

- INTERNAL (notice board, promotion)

- EXTERNAL (job adverts, agencies)

- INTERNAL (notice board, promotion)

- SELECTION PROCESS

- Interview

- Presentations

- Assessment centres

- Psychometric tests

- Interview

- TRAINING

- On the job

- Off the job

- Induction

- On the job

- RECRUITMENT PROCESS

- MOTIVATION

- WHAT MOTIVATES

EMPLOYEES IN A

WORKPLACE?

- Pay

- Responsibility

- Praise

- Empowerment

- Rewards

- Pay

- FREDRIK TAYLOR

- Workers enjoy work but

go to work to earn money

- Theory based

all around

payment

- Believes that money

does motivate and

piecework is an

effective method to use

- Workers trained to do

one job well

- Workers enjoy work but

go to work to earn money

- ELTON MAYO

- Believed workers are

motivated by having special

needs met

- Conducted a study known as

the ''hawthorne effect''

- CONCLUSIONS:

Managers &

Employees

communicating

motivates, Managers

taking an interest

motivates, Working in

teams motivates

- CONCLUSIONS:

Managers &

Employees

communicating

motivates, Managers

taking an interest

motivates, Working in

teams motivates

- Believed workers are

motivated by having special

needs met

- ABRAHAM MASLOW

- Devised a hierarchy of needs

- Each level has to

be fulfilled before

the next

motivates

- Physiological needs

(food, water, shelter)

- Safety needs

(security,

protection)

- Social needs

(Sense of

belonging)

- Self esteem

(praise,

recognition)

- Self actualisation (achieve dreams)

- Physiological needs

(food, water, shelter)

- Devised a hierarchy of needs

- FREDERICK HERZBERG

- Believes some factors motivate,

some demotivate.

- Motivators:

Job

enlargement,

Job

enrichment,

Empowerment

- Demotivators:

Anything else

- Motivators:

Job

enlargement,

Job

enrichment,

Empowerment

- Believes some factors motivate,

some demotivate.

- WHAT MOTIVATES

EMPLOYEES IN A

WORKPLACE?

- EFFECTIVE MARKETING

- The purpose of marketing is to meet the

customers needs & wants

- NICHE MARKET:

Small specialised

market

- MASS MARKET:

Larger more general

market

- NICHE MARKET:

Small specialised

market

- The purpose of marketing is to meet the

customers needs & wants

Media attachments

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.