5034600

Description

Mind Map by Kevin Reynolds, updated more than 1 year ago

|

|

Created by Kevin Reynolds

over 9 years ago

|

|

Adjusting Entries

- Multi-period items / Accrued items

Annotations:

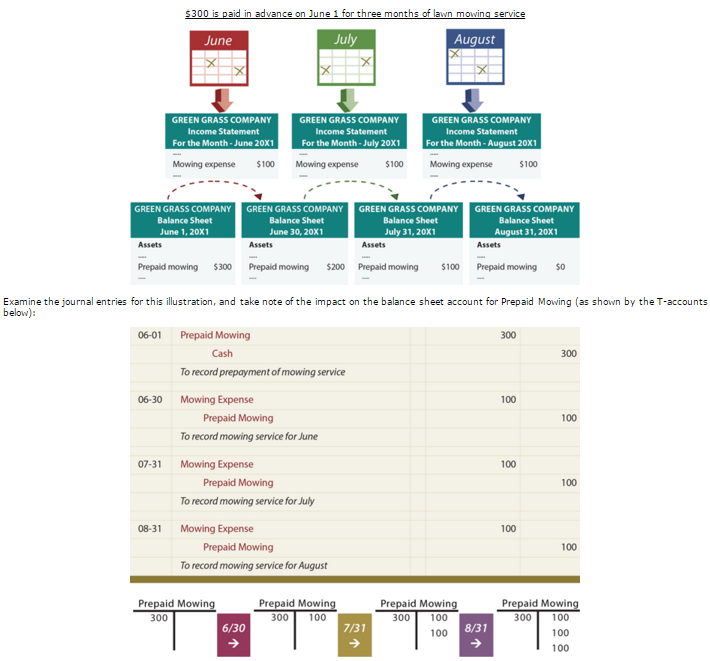

- Adjustments should be made every time financial statements are prepared, and the goal of the adjustments is to correctly assign the appropriate amount of expense to the time period in question (leaving the remainder in a balance sheet account to carry over to the next time period(s)).

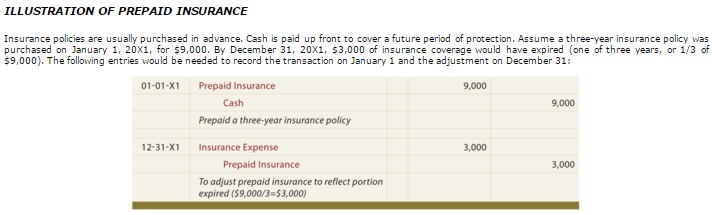

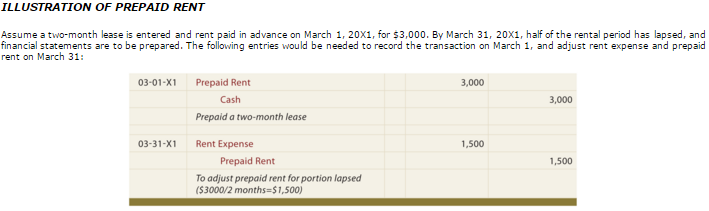

- Prepaid Expenses

Annotations:

- Prepaid expenses are not recognized as expenses, but as assets until one of the qualifying conditions is met resulting in a recognition as expenses.

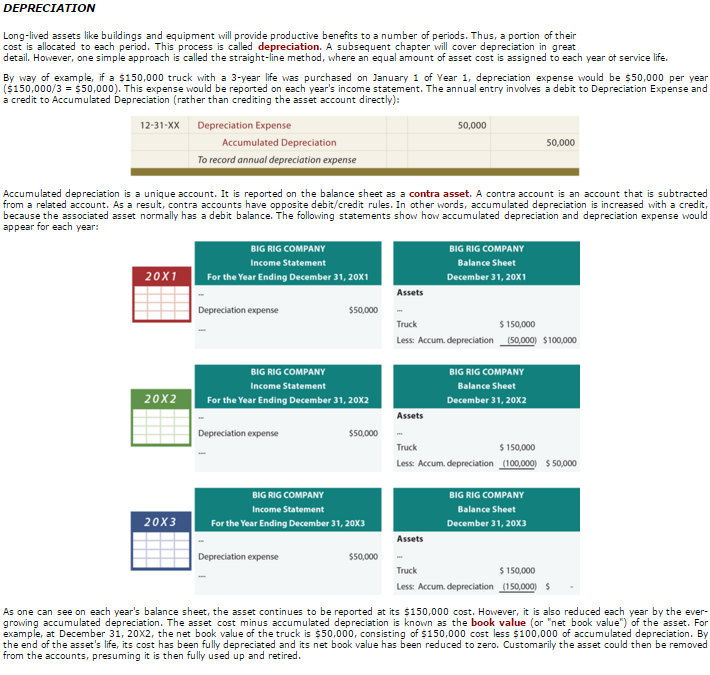

- Depreciation

Annotations:

- Straight-line method: an equal amount of asset cost is assigned to each year of service life Other methods include (see resource - Depreciation Methods): * Units of Output * Double declining balance

- Unearned revenue

- Unrecorded expenses

- Unrecorded revenues

- Alternative: balance sheet and income statement approach

Annotations:

- Has an advantage if the entire prepaid item or unearned revenue is fully consumed or earned by the end of an accounting period. No adjusting entry would be needed because the expense or revenue was fully recorded at the date of the original transaction.

- Expense Recognition

- Also know as the matching principle

Annotations:

- Expenses should be recorded during the period in which they are incurred, regardless of when the transfer of cash occurs

- Also know as the matching principle

- Revenue Recognition

Annotations:

- Revenues must be recognized in the period in which they occur

- Adjusting process

Media attachments

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.