Page 1

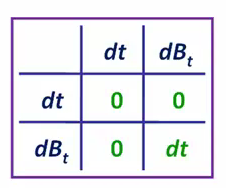

Introduction:In this unit, we are going to be looking at how to find stochastic differential equations or SDE's for functions of standard brownian motion. SDE's for f(Bt):In order to be able to work out SDE's for functions of standard brownian motion, we need to be aware of this 2 * 2 multiplication grid. In this 2 * 2 multiplication grid, we have a very small change in time dt and we have a change in standard brownian motion over that very small period of time dbt. Now the change in time dt is so small that when you multiply it by some thing else very small, you just get 0. change in a standard brownian motion over a very small preriod of time dbt is also very small. But its not so small that when you multiply it by itself, you get 0. When you square dbt, you get dt. The mathematics behind this 2 * 2 multiplication grid, you dont have to worry about in subject CT8. But you do need to able to be aware of its result.

{kind=link}

Want to create your own Notes for free with GoConqr? Learn more.