3763437

| Questão | Responda |

| what is economics? | studies the choices that individuals, businesses, governments and entire societies make as they cope with scarcity and the incentives |

| what is the difference between micro and macro? | micro - choices of individuals and businesses macro - national and global |

| 2 big economic questions | 1) how do choices end up determining what, how and for whom g&s get produced? 2) when do choice made in the pursuit of self interest also promote the social interest? |

| what are goods and services? | the objects that people value and produce to satisfy human wants |

| what are the types of goods and services? | agriculture or manufactured goods and services |

| what are the factors of production? | -land (rent) -capital (physical & funds), -labor (human capital) -entrepreneurship (controls all the other factors) |

| what is self interest? | you make choices that are best for you? |

| what is social interest? | choices that are best for society. the 2 dimensions - efficiency and equity |

| when are we efficient? | when it is not possible to make someone better off without making someone worse off |

| what is equity? | fairness |

| what current topics may illustrate tension between self interest and social interest? | globalization, info-age monopolies, global warming, economic instability and political instability |

| a choice is always a _________ | tradeoff |

| ________ is what you gain from something | benefit |

| _____ is what you must give up to get something | cost |

| what is considered a rational choice | when net benefit = net cost |

| what is marginal benefit | the additional satisfaction or utility that a person receives from consuming additional unit of a good or service |

| what is marginal cost? | opportunity cost of pursuing an incremental increase in an activity |

| what is a positive statement? | checking against a fact (ex: gov't provided health care increase public expenditures) |

| what is a normative statement? | an opinion that cannot be tested; values (ex: gov't should provide basic healthcare to all citizens) |

| what is an economic model? | description of aspects of the economic world only including features for that purpose |

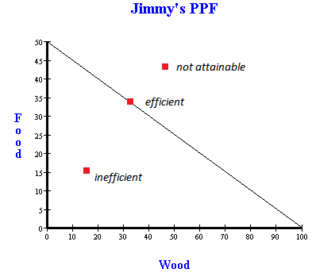

| what is the production possibilities frontier? (PPF) | the boundary between those combinations of goods and services that can be produced and those that cannot |

| describe where on a PPF you are inefficient, efficient and not attainable? | |

| what is production efficiency? | if we cannot produce more or one good without producing less of some other good |

| why is the PPF curved? | because resources are not equally productive in all activities |

| the more we have of a good the ______ the marginal benefit. | smaller |

| what is the optimum point of production? | MB = MC (equal highest potential value for each resource) |

| what causes economical growth? | technological change or capital accumulation |

| what is the cost of economic growth? | ato grow research and development, and produce new capital, we must decrease our production or consumption |

| what is a comparative advantage? | a person has it in an activity if they can perform at a lower opportunity cost |

| what is the absolute advantage? | a person that is more productive |

| what are markets? | any arrangement that enables buyers and sellers to get information and do business |

| what is a competitive market? | many buyers and sellers, no single buyer or seller can influence the price |

| the money price | the amount of money needed to buy a good |

| the relative price | the ratio of its money price to the money price of the next best alternative good - its opportunity cost |

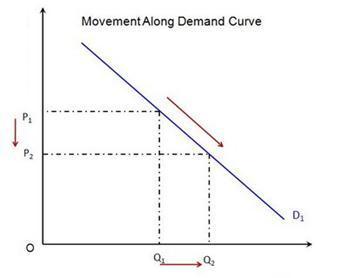

| what is the difference between demand and quantity demanded? | demand = relationship between quantity and money quantity demanded = how much is demanded at a particular point |

| what is the law of demand? | - other things remaining the same, the higher the price of a good, the smaller is the quantity demanded -the lower the price of a good, the larger the quantity demanded |

| what influences a change in quantity demanded? | substitution effect and income effect |

| what is substitution effect? | when the relative price of a good or service rises, people seek substitutes for it, so the quantity demanded decreases |

| what is income effect? | when the price a good and service rises relative to people's incomes, people cannot afford all the things they want therefore quantity demanded decreases |

| what is willingness to pay? | the small the qty, higher the price people are willing to pay --> marginal benefit |

| when there is change in demand what happens to the curve? | it shifts left (D down), shifts right (D up) |

| what are the 6 main factors that change demand? | 1) price of related goods 2) expected future prices 3) income 4) expected future income and credit 5) population 6) preferences |

| in terms of related goods what causes demand to increase? | substitute decreases compliment increases |

| if the price of a good is expected to rise in the future, current demand will ________? | increase |

| when income increases, a normal good will _______ and an inferior good (cheap stuff) will _______. | increase, decrease |

| when income is expected to increase in the future the demand will _______? | increase |

| the larger the population the ________ the demand? | higher |

| if a preferences increases, the demand will ________? | increase |

| what does an increase in demand look like? | |

| what does an increase in quantity demanded look like? | |

| what is the law of supply? | the higher the price of a good, the greater the quantity supplied |

| producers will only produce a good if they can produce ____ or _______ then the MC. | at, higher |

| what are the 6 main factors that change supply? | 1) prices of factors on production 2) prices of related goods produced 3) expected future prices 4) number of suppliers 5) technology 6) state of nature |

| if the price of oil increases the production will ______? | decrease |

| if the production of a substitute decreases, supply will ______. | increase |

| compliments must be produced ________. | together |

| if the price of a good is expected to rise in the future, supply of the good today _____ and the supply shifts ______. | decreases, leftward |

| the larger the number of suppliers of a good, the ________ is the supply of a good? therefore supply shift rightward | greater (supply shift rightward) |

| an increase in technology causes a ______ in supply. | increase |

| if a natural disaster occurs, the supply will _______? | decrease |

| what is the difference between a change in supply and a change in quantity supplied? | change in supply are factors that shift the curve change in quantity supplied is a change in price producers sell at |

| when does market equilibrium occur? | opposing forces balance each other (price and buyer/seller) |

| when does equilibrium price occur? | quantity demanded = quantity supplied |

| what is equilibrium quantity? | the quantity bought and sold at the equilibrium price - price regulates buying and selling plans - price adjusts when plans don't match |

| this is an example of a _______? | surplus - at original price decrease in demand and increase in supply |

| describe a shortage | anything below the equilibrium - at original price an increase in demand and a decrease in supply |

| a surplus forces the price to go ______, whereas a shortage forces the price to go ______. | down, up |

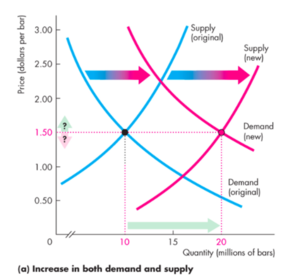

| an increase in demand and an increase in supply _____ the equilibrium quantity. | increase |

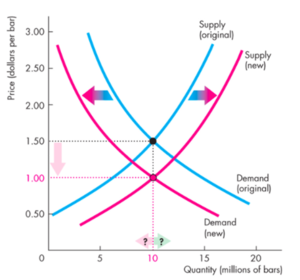

| a decrease in demand and an increase in supply _______ the equilibrium price. | lowers |

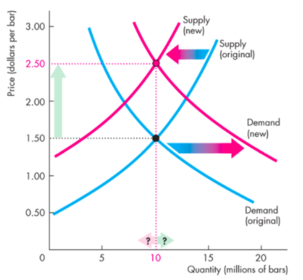

| an increase in demand and a decrease in supply _______ the equilibrium price. | raises |

| the 6 main factors that change the supply of a good | 1) prices of factors of production 2) prices of related goods produced 3) expected future prices 4) the number of suppliers 5) technology 6) state of nature |

| what is a movement along a supply curve? | when the price changes but all other influences remain constant |

| a shift of the supply curve is caused by what? | price stays the same, other determinants change |

| what is equilibrium price? | price at which the quantity demanded equals the quantity supplied |

| what is equilibrium quantity? | the quantity bought and sold at the equilibrium price |

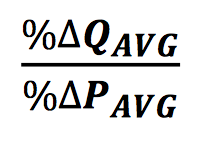

| what is another word for elasticity? | responsiveness |

| YESwhat is the general formula of elasticity? | |

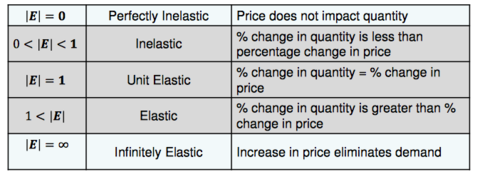

| does you use absolute value for price elasticity? | YES |

| Elasticity is a ratio of percentages, so a change in the units of measurement of price or quantity leaves the elasticity value the ______. | same |

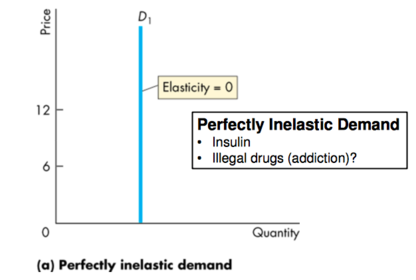

| describe perfectly inelastic demand | buy the same amount no matter what the price is (inelastic starts with an i and "i"s are straight) NO CLOSE SUBSTITUES |

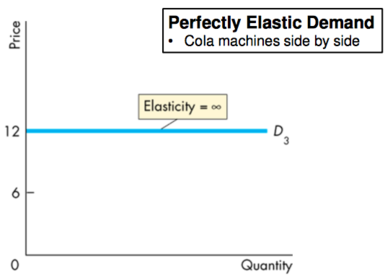

| describe perfectly elastic demand | no matter quantity, same price --> Quantity demanded increases at a infinite faster rate then price |

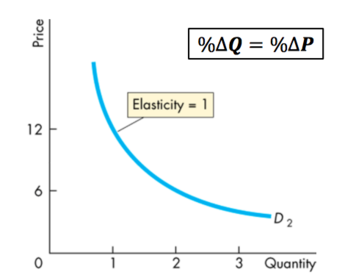

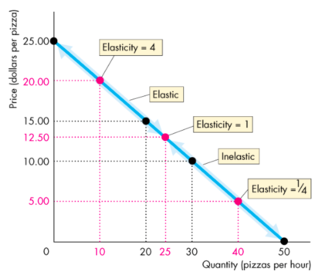

| describe unit elastic demand | when %change in Qd = %change in P |

| what numbers correlate to... -perfectly inelastic -inelastic -unit elastic -elastic -infinitely elastic | |

| what is the main difference between inelastic and elastic? | inelastic - price changes quicker then quantity elastic - quantity quicker then price |

| factors that influence elasticity of demand | - closeness of substitutes - proportion of income spent on good - the time elapsed since a price change |

| where is unit elastic on the demand curve? | the midpoint |

| total revenue and elasticity When the price changes, total revenue also __________. But a rise in price doesn’t always increase ___________. | changes, total revenue |

| what is the total revenue test? |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Quer criar seus próprios Flashcards gratuitos com GoConqr? Saiba mais.