10286726

Descrição

Mapa Mental por Ngan Ha Nguyen, atualizado more than 1 year ago

|

|

Criado por Ngan Ha Nguyen

mais de 7 anos atrás

|

|

Economics

- Basic definitions

Anotações:

- Studies the ways in which society decides what to produce, how to produce them, who to produce them for and how to apportion them. We are all economic agents and economic activity is what we do to make a living

- Assumptions: people behave

rationally at all times and always

seek to improve their circumstances

- Producers: maximize their

profits

- Consumers: maximize their

benefits from their income

- Governments: maximize the welfare of

their populations

- Producers: maximize their

profits

- Economic

systems

- Centrally planned (command)

Anotações:

- decisions and choices about resource allocation are made by the government Only the government can make fair and proper provision for all members of society

- Free market

Anotações:

- decisions and choices about resource allocation are left to market forces of supply and demand, and the workings of the price mechanism

- Mixed

- Centrally planned (command)

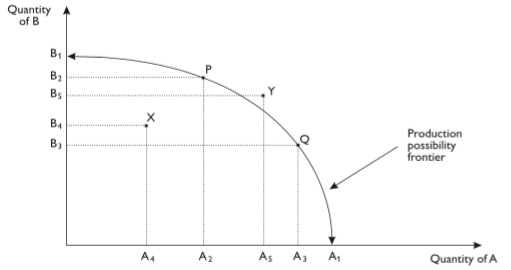

- Scarcity of resource:

human wants exceed

what can be actually

produced

- Production possibility

frontier

- Opportunity cost: the cost of an

item measured in terms of the

alternatives forgone

- Opportunity cost: the cost of an

item measured in terms of the

alternatives forgone

- Absolute advantage vs. comparative advantage

- Market: buyers and sellers come

together to exchange goods/services.

Goods/services has a price if it is both

useful and scarce

- Marginal utility: the extra

satisfaction gained by the

consumption of one additional unit

of goods/services

Anotações:

- consumers use marginal utility to decide to or not to buy one additional unit of goods/services

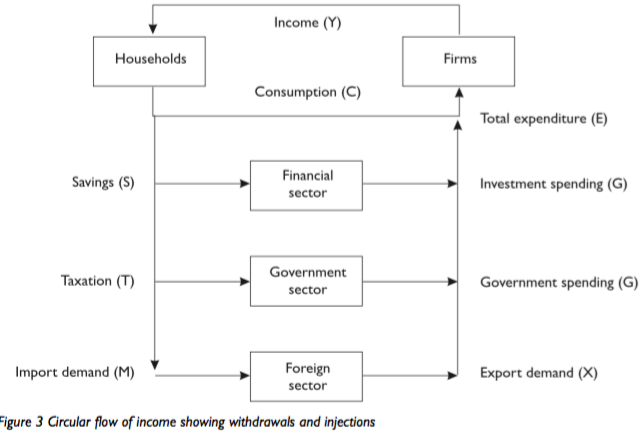

- Macro economics: studies the aggregated

effects of the decisions of economic units,

looks at a complete national economy or

the international economic system as a

whole

- National income (net national product): the sum of all

incomes which arise as a result of economic activity, that

is from the production of domestically owned

goods/services

- Gross domestic product: the total value of income/ production from

economic activities within a country in a given period

- Gross national product: = GDP + net property income from abroad

- Purposes: measure the living standard in a

country, compare wealth between

countries; measure the improvements;

assist the government in economic

planning

- Determine national income

- Gross domestic product: the total value of income/ production from

economic activities within a country in a given period

- Inflation & unemployment

- Policies

- Government intervention and income distribution

- National income (net national product): the sum of all

incomes which arise as a result of economic activity, that

is from the production of domestically owned

goods/services

- Micro economics: studies

individual economic units

(households/firms)

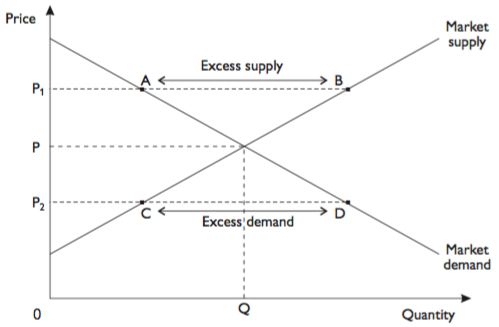

- Demand: the quantity of goods/services that potential purchasers would be

willing and able to buy, or attempt to buy, at any possible price

- Factors: price, income, price of substitute

goods, tastes and fashion, expectations of

future price changes, distribution of income

- Substitute goods (goods that are alternatives to

each other)/ Complements goods (goods that tend

to be bought and used together)

- Factors: price, income, price of substitute

goods, tastes and fashion, expectations of

future price changes, distribution of income

- Supply: the quantity of goods/services that existing suppliers or would-be

suppliers would want to produce for the market at a given price

- Factors: cost of making, prices of other goods,

expectation of price changes, changes in technology,

other factors

- Factors: cost of making, prices of other goods,

expectation of price changes, changes in technology,

other factors

- The equilibrium price: the price at which market supply and market demand quantities are in balance

- Price mechanism

- Price mechanism

- Demand-supply analysis

- Elasticity of demand and supply

- X elasticity of Y: the

responsiveness in the Y of

a good to a change in the X = %change in Y/ %change in X

- X elasticity of Y: the

responsiveness in the Y of

a good to a change in the X = %change in Y/ %change in X

- Elasticity of demand and supply

- Cost/revenue/productivity

- A firm will maximize its profits when

marginal cost equals marginal revenue MC = MR

- A firm will maximize its profits when

marginal cost equals marginal revenue MC = MR

- Demand: the quantity of goods/services that potential purchasers would be

willing and able to buy, or attempt to buy, at any possible price

Anexos de mídia

{kind=link}

{kind=link}

{kind=link}

Quer criar seus próprios Mapas Mentais gratuitos com a GoConqr? Saiba mais.