461597

Descrição

Methods of Government

Intervention to Correct

Distortions to Individual

Markets

- Pollution Permits

- POLLUTION PERMIT= a

permit sold to firms by the

government, allowing them to

pollute up to a certain limit

- A method using the

market to address the

problem, rather than

through regulation

- The permits can be traded,

creating an incentive for firms

to be relatively 'clean so that

if they don't use up their full

allocation of permits they can

sell any remaining allocation

to other less 'clean' firms

- This provides firms with an

incentive to reduce their

negative externalities and

consider external costs

- This provides firms with an

incentive to reduce their

negative externalities and

consider external costs

- System must be enforced

by factory inspectors and

government must decide

the level of fines sufficient

to penalise firms and deter

further pollution beyond the

permitted level

- POLLUTION PERMIT= a

permit sold to firms by the

government, allowing them to

pollute up to a certain limit

- State provision

- This is where the

government directly

provides goods and

services to

consumers, using

money from taxation.

- e.g. the government

pays private sector

firms to operate

prisons and maintain

our road network

- The main

state-owned

businesses in

the UK is

Network Rail,

strategically

publicised after

WW2

- This is where the

government directly

provides goods and

services to

consumers, using

money from taxation.

- Regulation

- Pass laws

- e.g. ban of smoking in public places

- e.g. prohibiting

the sale of

cigarettes to

under-18s

- Make it illegal

to do certain

things, this

should control

demand and

supply

- e.g. employment laws (to do with minimum wage)

- e.g. ban of smoking in public places

- Regulators

- Government appointed regulators

exist who can impose price controls

in most of the main utilities like gas

and electricity (Ofgem), water (Ofwat),

communications (Ofcom) and others

- Introduced in Margaret Thatcher's time

in parliament (1980s) when firms were

re-privatised after being in the public

sector after WW2

- oversee firms to

ensure they're

doing the right

thing

- Government appointed regulators

exist who can impose price controls

in most of the main utilities like gas

and electricity (Ofgem), water (Ofwat),

communications (Ofcom) and others

- Pass laws

- Financial Intervention

- Indirect Taxation

- INDIRECT TAX= a tax on spending

- Can be used to raise the price of demerit goods

and products that generate negative externalities

- This will reduce quantity demanded to a socially optimal level

- Imposed on producers (suppliers) by the government

- Examples~ excise duties (on cigarettes, alcohol and fuel) and VAT

- Examples~ excise duties (on cigarettes, alcohol and fuel) and VAT

- Imposed on producers (suppliers) by the government

- This will reduce quantity demanded to a socially optimal level

- effects supply

(leftward shift

when applied)

- Opposite to

a direct tax

(placed on

incomes)

- When demand is elastic, most is paid by the producer

- When demand is inelastic, most is paid by the consumer

- e.g. a minimum price

per unit of alcohol at

50p was requested in

Scotland in 2012

- Should ration demand

- Should ration demand

- INDIRECT TAX= a tax on spending

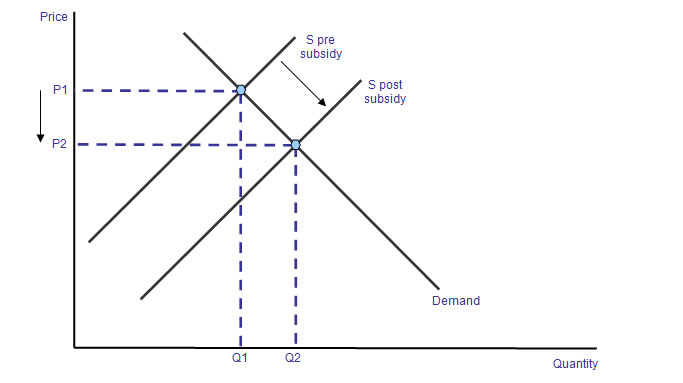

- Subsidies

- Will lower the price of merit goods to consumers

- e.g. EMA allowances to students

in further education to reduce

the private costs of education

- e.g. subsidies to companies

employing workers on the

New Deal programme

- Designed to boost consumption and output of products with positive externalities

- Designed to boost consumption and output of products with positive externalities

- e.g. subsidies to companies

employing workers on the

New Deal programme

- e.g. EMA allowances to students

in further education to reduce

the private costs of education

- effect supply

(rightward shift

when applied)

- Will lower the price of merit goods to consumers

- Indirect Taxation

- Price Intervention

- Price Controls

- Maximum prices

- 'price ceiling'

- Suppliers

cannot

exceed

this price

- It's an attempt to prevent the

market price from rising

above a certain level

- It's an attempt to prevent the

market price from rising

above a certain level

- Only have an effect

if set below the

equilibrium (below the

free market price)

- e.g. when shortage of essential foodstuffs

threatens large rises in the free market price

- e.g. rent controls still in place in Manhattan in the USA

- 'price ceiling'

- Minimum prices

- 'price floor'

- Only have an

effect if set

above the

equilibrium

(above the free

market price)

- Suppliers cannot

go below this price

- e.g. national minimum wage, first imposed in the UK in 1999

- Intervention into the labour market designed to

increase the pay of lower-paid workers and therefore

influence the distribution of income in society

- Intervention into the labour market designed to

increase the pay of lower-paid workers and therefore

influence the distribution of income in society

- 'price floor'

- The government can set legally imposed

maximum or minimum prices on goods and

services

- Involves a

normative

judgement

on behalf

of the

government

about what

the price

should be

- Maximum prices

- Buffer Stocks

- Governments may intervene when

markets suffer from considerable

volatility in the free market price

- They'll try to manipulate the

free market price by the use

of buffer stock schemes

- They'll try to manipulate the

free market price by the use

of buffer stock schemes

- e.g. often used in agricultural

and commodity markets as

they're notorious for huge price

instability due to unpredictable

weather and relatively inelastic

demand and supply curves

- The method...

- Select a price to keep to (the

average long-term equilibrium price)

- Use a buffer stock; in years of a bumper (good) harvest, store

some stock away so that in years of poor harvest more stock

can be released, the government will buy up excess

supply (stock) so the income of farmers stays constant)

- this should avoid the price effects of fluctuating supply

- this should avoid the price effects of fluctuating supply

- Use a buffer stock; in years of a bumper (good) harvest, store

some stock away so that in years of poor harvest more stock

can be released, the government will buy up excess

supply (stock) so the income of farmers stays constant)

- Select a price to keep to (the

average long-term equilibrium price)

- Governments may intervene when

markets suffer from considerable

volatility in the free market price

- Price Controls

Anexos de mídia

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Quer criar seus próprios Mapas Mentais gratuitos com a GoConqr? Saiba mais.