25937932

Descrição

Quiz por Cindy Nguyen, atualizado more than 1 year ago

|

|

Criado por Cindy Nguyen

aproximadamente 4 anos atrás

|

|

Questão 1

Questão

What qualifies as a tax?

Tax - a payment [blank_start]required[blank_end] by a government agency that is unrelated to any specific benefit or service received from the government agency

- payment is required

- by a [blank_start]government[blank_end] agency

- payment must not be tied directly to the benefit received by the [blank_start]person[blank_end]

Examples:

- Speeding and got a ticket - [blank_start]not a tax[blank_end], components met/not met: [blank_start]3[blank_end]

- Building a home & need to get permits worth $500 - [blank_start]not a tax[blank_end], components met/not met: [blank_start]3[blank_end]

- Visited a hotel & got a bill charging 1% for "local gov't various city projects" - [blank_start]a tax[blank_end], component met/not met: [blank_start]all[blank_end]

Responda

-

required

-

not required

-

government

-

nongovernmental

-

person

-

government

-

not a tax

-

a tax

-

3

-

2

-

1

-

all

-

not a tax

-

a tax

-

3

-

2

-

1

-

all

-

a tax

-

not a tax

-

all

-

1

-

2

-

3

Questão 2

Questão

How to calculate a tax?

Tax base x tax rate = tax [blank_start]liability[blank_end]

Tax base – federal [blank_start]taxable[blank_end] income, amount on which tax rate is applied

Tax rate- depends on who taxpayer is

Proportional tax – tax rate does not change irrespective of whether tax base increases or [blank_start]decreases[blank_end]

Ex. Sales tax

Progressive tax – as tax base goes up, your tax rate goes [blank_start]up[blank_end]

Responda

-

liability

-

taxable

-

decreases

-

up

Questão 3

Questão

What do you think is harder to determine, tax base or tax rate?

Responda

-

Tax base

-

Tax rate

Questão 4

Questão

Formula for federal income tax on individuals:

Income – exclusions = [blank_start]gross[blank_end] income

gross income - deductions = [blank_start]taxable[blank_end] income

taxable income - (tax calculated – tax credits) = tax due/refund

Responda

-

gross

-

taxable

Questão 5

Questão

A tax credit allowed for electricity produced from renewable sources - [blank_start]Economic Justification[blank_end]

A tax credit allowed for the purchase of a motor vehicle that operates on alternative (i.e., nonfossil fuels) energy sources - [blank_start]Economic justification[blank_end]

Favorable treatment accorded to research and development expenditures - [blank_start]Economic justification[blank_end]

The deduction allowed for contributions to qualified charitable organizations - [blank_start]Social justification[blank_end]

An election that allows certain corporations to avoid the corporate level income tax and pass losses through to their shareholders - [blank_start]Economic Justification[blank_end]

Responda

-

Economic Justification

-

Social Justification

-

Administrative feasibility

-

Equity concerns

-

Economic justification

-

Administrative feasibility

-

Social Justification

-

Equity Concerns

-

Economic justification

-

Administrative feasibility

-

Social Justification

-

Equity Concerns

-

Social justification

-

Administrative feasibility

-

Economic Justification

-

Equity Concerns

-

Economic Justification

-

Administrative feasibility

-

Social Justification

-

Equity Concerns

Questão 6

Questão

Economic Justification - help control the [blank_start]economy[blank_end] in some manner or encourage certain activities, industries, or businesses

- research and development

- small businesses

- foster technological progress

- encouraging investment in business capital

- clean air & environmental resources

- agriculture

Social Considerations - desire to encourage certain [blank_start]social[blank_end] results.

- accident and health insurance plans

- pension plans

- qualified charities

- obtain or extend education

- care for minors or disabled dependents

Responda

-

economy

-

social

Questão 7

Questão

Equity Considerations - fairness, progressive, regressive, or [blank_start]proportional[blank_end] taxes

- alleviate effect of multiple taxation

- postpone recognition of gain when lacking ability to pay the tax

wherewithal to pay - inequity of taxing a transaction when the taxpayer lacks the [blank_start]means[blank_end]

involuntary conversion - property is destroyed by casualty or taken by a [blank_start]public[blank_end] authority through condemnation

Political Considerations - political considerations often influence tax law

- special interest legislation

- state/local government influences

Responda

-

proportional

-

means

-

public

Questão 8

Questão

Tax law sources

Primary authorities – official tax authorities from the [blank_start]3[blank_end] branches of government (legislative, judicial, executive)

Legislative – statutes, internal revenue code (THE source for [blank_start]tax[blank_end] law)

- Enacted by congress & signed into law by president

Judicial – cases on tax [blank_start]issues[blank_end], look at these cases for research

- Interpret or [blank_start]explain[blank_end] internal revenue code/law

Administrative (Executive) – treasury department, IRS, private letter rulings, tax advice [blank_start]memos[blank_end]

Secondary authorities – comes from publishers, tax articles, [blank_start]unofficial[blank_end] tax sources

- Interpret and [blank_start]explain[blank_end] tax law from publisher’s perspective

- Good starting point for your [blank_start]research[blank_end]

- Carry little to no weight in court system, cannot [blank_start]cite[blank_end] them in memos or in practice

Responda

-

3

-

tax

-

issues

-

explain

-

memos

-

unofficial

-

explain

-

research

-

cite

Questão 9

Questão

Primary or Secondary?

i. Internal revenue code – [blank_start]primary[blank_end]

ii. Tax article in usa today – [blank_start]secondary[blank_end]

iii. Article on supreme court opinion – [blank_start]secondary[blank_end]

iv. Supreme court opinion – [blank_start]primary[blank_end]

v. Ria federal tax coordinator – [blank_start]secondary[blank_end]

vi. Treasury regulations – [blank_start]primary[blank_end]

Responda

-

Primary

-

Secondary

-

secondary

-

primary

-

secondary

-

primary

-

secondary

-

primary

-

primary

-

secondary

-

primary

-

secondary

Questão 10

Questão

Statutory authorities

U.S. Constitution

- [blank_start]16th[blank_end] amendment – grants congress to tax income from whatever source derived

Tax treaties - Enables congress to create tax treaties with other companies

- Negotiated agreements between two different [blank_start]countries[blank_end] on how they’re going to tax a person or business entity

- Sometimes will conflict with [blank_start]domestic[blank_end] law, whatever comes out last prevails

Organization of Internal revenue code

- Subtitle, chapter, [blank_start]subchapter[blank_end], sec, [blank_start]subsection[blank_end], paragraph, [blank_start]subparagraph[blank_end], clause

- Example of code citation:

Section, section #, subsection, paragraph designation

Committee reports

- Explanation of [blank_start]current[blank_end] law, what the proposed change & justification

- Takes a long time for guidance to come out so people look at committee reports to [blank_start]interpret[blank_end] the legislation

Responda

-

16th

-

countries

-

domestic

-

subchapter

-

subsection

-

subparagraph

-

current

-

interpret

Questão 11

Questão

Legislative process for tax bills

1. Begins in [blank_start]house[blank_end] of reps, in house ways of means committee, debated it and draft a bill

2. Send it to the whole house & vote on it, cannot [blank_start]modify[blank_end] bill

3. Goes to [blank_start]senate[blank_end] and if passes bill becomes an act

4. Passed to senate [blank_start]finance[blank_end] committee to debate & amend, send it back to senate

5. Senate debates, votes, and modify

6. Passes and goes to [blank_start]joint[blank_end] conference committee, takes house & senate version, choose whatever version provision, compromise & combine, or strike the provisions

7. Goes back to house & [blank_start]senate[blank_end] for vote

8. If passed, go to [blank_start]president[blank_end] for signature & president signs it, becomes a public law & incorporated into internal revenue code of 1986

9. If president vetoes it, it’ll go back to house & senate, they can [blank_start]override[blank_end] if they have 2/3 positive majority vote in each house & senate

Responda

-

house

-

modify

-

senate

-

finance

-

joint

-

senate

-

president

-

override

Questão 12

Questão

Judicial Sources: The Courts

Supreme court – [blank_start]highest[blank_end] court in the land, all decisions in lower courts must be followed by supreme court

Court of appeals – 2nd highest level, [blank_start]13[blank_end] circuit courts, 11 based on region, 1 in DC, 1 is court of appeals in federal circuit

- Different court of appeals do not have to follow other circuits decisions in appellate courts, not compelled to, can be persuaded & influenced but not required to

Responda

-

highest

-

13

Questão 13

Questão

What circuit court of appeals?

New Jersey - [blank_start]3[blank_end]

California - [blank_start]9[blank_end]

New York - [blank_start]2[blank_end]

Responda

-

3

-

1

-

2

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

9

-

1

-

2

-

3

-

4

-

5

-

6

-

7

-

8

-

10

-

11

-

12

-

13

-

2

-

1

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

Questão 14

Questão

Trial level courts: [blank_start]3[blank_end] trial level courts – lowest levels, where litigation is initiated

- Have to strategize where they’ll bring their claim

- Trial level courts [blank_start]don’t[blank_end] have to follow other courts decisions, only have to follow higher court decisions with appellate jurisdiction

Us district court

- Local court

- Typically has [blank_start]1[blank_end] judge, judges are [blank_start]generalist[blank_end]

- Can hear tax, criminal, a variety of cases

- Taxpayer has to pay tax [blank_start]first[blank_end] & then sue for refund

- The only trial level court where a [blank_start]jury[blank_end] trial is available

- Can appeal to court of [blank_start]appeals[blank_end]

Responda

-

3

-

don’t

-

1

-

generalist

-

first

-

jury

-

appeals

Questão 15

Questão

Us Tax court – national court, [blank_start]19[blank_end] judges of tax [blank_start]experts[blank_end]

- the only court where the taxpayer doesn’t have to pay tax [blank_start]first[blank_end] in order to be heard by the court

- if someone doesn’t agree with decisions, it can go to court of [blank_start]appeals[blank_end]

- depends on taxpayer’s residence which court region to go to

Only court with small case division

- hears cases that are [blank_start]50000[blank_end] or less

- more informal preceding

- don’t need an [blank_start]attorney[blank_end], can represent themselves

- can’t be cited as [blank_start]precedent[blank_end]

- not open to [blank_start]appeals[blank_end]

Us court of federal claims

- Has [blank_start]16[blank_end] judges, national court, usually 1 judge hear a case at a time

- Judges are [blank_start]generalists[blank_end]

- Hears case that are brought against the [blank_start]government[blank_end]

- Taxpayer has to pay tax [blank_start]first[blank_end] & then sue for refund

- Have to appeal to Court of appeals for [blank_start]federal[blank_end] circuit, not based on geography/taxpayer’s residence

Tax court decisions

- Regular tax decisions have [blank_start]novel[blank_end] tax issues that have not come up before

- Memorandums involve decisions that is based on [blank_start]existing[blank_end] law

Responda

-

19

-

experts

-

first

-

appeals

-

50000

-

attorney

-

precedent

-

appeals

-

16

-

generalists

-

government

-

first

-

federal

-

novel

-

existing

Questão 16

Questão

Practice Problem:

Tax Court - [blank_start]19[blank_end] Judge(s)

Federal Claims - [blank_start]16[blank_end] Judge(s)

District Court - [blank_start]1[blank_end] judge(s)

Trial jury available - only in the [blank_start]district[blank_end] court

Don't have to pay tax first - [blank_start]tax[blank_end] court

1. No cash to pay for litigation of IRS tax claim - [blank_start]tax[blank_end] court since you don't have to pay money beforehand

2. Complicated tax issue - [blank_start]tax[blank_end] court for tax experts

3. Issue is not complicated but want people sympathetic to their plight - [blank_start]district[blank_end] court because there's a jury trial option

Responda

-

19

-

16

-

1

-

district

-

tax

-

tax

-

tax

-

district

Questão 17

Questão

Writ of certiorari – request to be heard by [blank_start]supreme[blank_end] court

- Rare that they’ll hear a tax case

- Do not hear all cases that are appealed to them

Stare decisis: Latin for “to stands by things decided”

- If taxpayer brings a case to tax court, the tax court has to follow its own [blank_start]prior[blank_end] rulings as precedent & has to follow prior ruling of [blank_start]higher[blank_end] court w/ appellate jurisdiction

Golsen rule - Decided that [blank_start]tax[blank_end] court must follow stare decisis

- Similar controlling facts but two different taxpayers with different circuits

1. One court has favorable vs other court is unfavorable

2. Even though the facts are the same, higher court rulings are [blank_start]different[blank_end] and results are different

Possible to have conflicting decisions within tax courts themselves

Responda

-

supreme

-

prior

-

higher

-

tax

-

different

Questão 18

Questão

Practice Problems:

a. Found a case for court of appeals for federal circuit with favorable decision for your client - Bring case to court of federal claims since it’ll follow court of appeals federal circuit [blank_start]prior[blank_end] ruling

b. Resident of NJ, there’s a case in 1st circuit & 3rd circuit that’s on point - [blank_start]3rd[blank_end] circuit, the court of appeals would have to follow that decision when going to tax or district court

c. Resident of NJ, bring it before tax court, found 1st circuit & 9th circuit on point, one favorable & one unfavorable

- Both will have [blank_start]equal[blank_end] weight since there’s no prior decision in 3rd circuit

- Look at case that supports taxpayer and argue that, the case that’s unfavorable try to [blank_start]distinguish[blank_end] the difference from that one

Discuss significance of following taxpayer’s issue

1. Decision from district court of Wyoming, taxpayer lives in Wyoming - Follow [blank_start]prior[blank_end] ruling

2. Court of federal claims, taxpayer lives in Wyoming - Follow [blank_start]prior[blank_end] ruling

3. 2nd circuit court of appeals, taxpayer lives in California - Doesn’t have to follow [blank_start]prior[blank_end] ruling

4. Decision by supreme court - follow [blank_start]prior[blank_end] ruling

Responda

-

prior

-

3rd

-

equal

-

distinguish

-

prior

-

prior

-

prior

-

prior

Questão 19

Questão

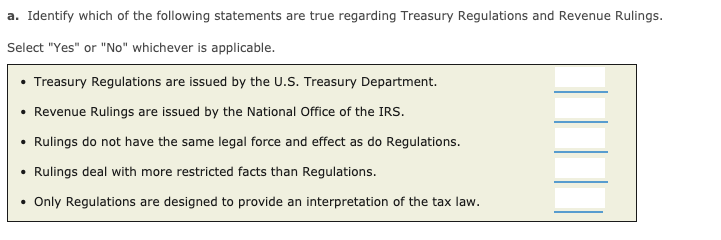

Administrative Sources: The US Treasury

- IRS is Division of US Treasury

3 Different Type of treasury regulations w/ 3 Different Purposes

Purposes

1. Interpretive – is interpreting the internal revenue code, providing further [blank_start]guidance[blank_end] & explanation

2. Procedural – explains the IRS own [blank_start]practice[blank_end] and procedures in administration of tax law

3. Legislative – congress directs the treasury department to [blank_start]issue[blank_end] regulations about a specific tax area, actually writing laws instead of interpreting

- Pretty rare to do

Forms

1. Final – [blank_start]highest[blank_end] administrative authority, official interpretation of internal revenue code by treasury department & IRS

- Same force & effect as law

- Considerable [blank_start]weight[blank_end] in court system, judges will defer to these

2. Temporary – a tax issue comes up and needs more [blank_start]immediate[blank_end] attention & guidance and will issue a temporary regulation

- issued concurrently with [blank_start]proposed[blank_end] regulations

- you need proposed regulation for comments to get final regulations

- the normal process to make final regulations takes a long time

- expires automatically in [blank_start]3[blank_end] years

- given deference by [blank_start]court[blank_end] & follow it, taxpayers can rely on temporary regulations if ever litigated

3. Proposed – issue regulations & open to public [blank_start]comments[blank_end], practitioners, academics will review & make suggestions, IRS take suggestions, takes them/rejects them and draft regulations

- the government’s view

- tentative

- carry less [blank_start]weight[blank_end] than final & temporary in court

- Are not [blank_start]binding[blank_end] on taxpayer & IRS

Responda

-

guidance

-

practice

-

issue

-

highest

-

weight

-

immediate

-

proposed

-

3

-

court

-

comments

-

weight

-

binding

Questão 20

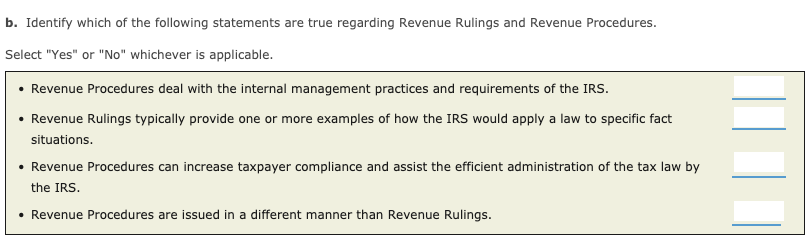

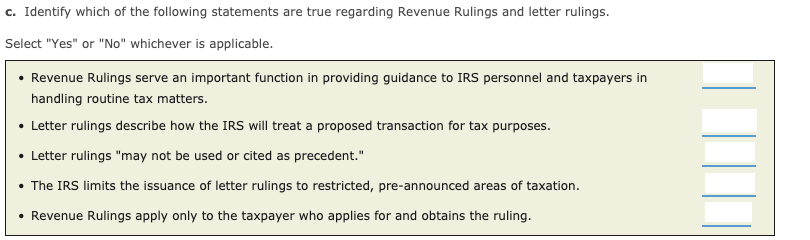

Questão

Revenue Rulings

- Official pronouncement that comes out of national office

- The IRS is applying tax law to a specific factual situation

- Do not carry as much [blank_start]weight[blank_end] as final or temporary treasury regulation

- Good for providing [blank_start]insight[blank_end] on IRS tax position they’ll take

- Often [blank_start]overruled[blank_end]

Revenue procedures

- Does not carry much [blank_start]weight[blank_end] as treasury regulations

- Explains IRS practices & [blank_start]procedures[blank_end]

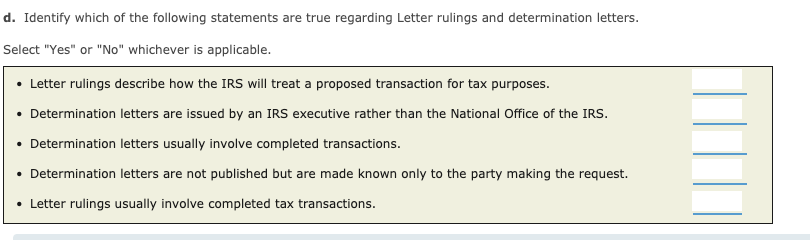

Private letter rulings

- Taxpayer requests from IRS a decision based on their specific proposed tax [blank_start]situation[blank_end]

- Cannot be cited as [blank_start]precedent[blank_end] by any other taxpayer in litigation

- Applies to the specific [blank_start]taxpayer[blank_end] and specific situation

- Can be cited to avoid substantial understatement penalty & tax preparer penalty

- Acquiescence or non-acquiescence

i. Acquiescence – although IRS [blank_start]disagrees[blank_end] with court decisions, but will no longer continue litigate tax issue

ii. Non-acquiescence – disagree with court decision and continue to [blank_start]litigate[blank_end] court decision

g. Actions on decisions - Explains [blank_start]reasoning[blank_end] for acquiescence or non-acquiescence

Technical advice memorandum - IRS agent, area director, appeals officer, etc. asks IRS national office for further [blank_start]guidance[blank_end] for specific tax technical issue

IRS publications

- Cannot [blank_start]cite[blank_end] in memo or in practice

- Carry no [blank_start]weight[blank_end] in court system

Responda

-

weight

-

insight

-

overruled

-

weight

-

procedures

-

situation

-

precedent

-

taxpayer

-

disagrees

-

litigate

-

reasoning

-

guidance

-

cite

-

weight

Questão 21

Questão

Tax research process

Step 1: identify and refine [blank_start]problem[blank_end]

- Understand your facts, what’s [blank_start]relevant[blank_end] from tax perspective

Open facts: haven’t happened yet

Closed fact: [blank_start]completed[blank_end] tax actions and want to know what will happen

- Identify issues

- Start broad & narrow it down

Step 2: locate appropriate tax law [blank_start]sources[blank_end]

- RIA checkpoint

Step 3: analyze tax sources

- Apply facts to [blank_start]law[blank_end], apply client’s facts to law

- Questions of fact – research hinges on client’s [blank_start]facts[blank_end], favorable vs unfavorable, distinguish client from them

- Questions of law – words or phrases, definitions, meanings & [blank_start]interpretation[blank_end]

- Conflicting authorities – the one that carries more [blank_start]weight[blank_end] (higher court decision), age of decision, appellate jurisdiction that apply

- Consider both sides – cannot simply support position, have to look at opposing side (unfavorable), can you differentiate client’s cases to assess strength of conclusion

Step 4: formulated solutions, [blank_start]alternative[blank_end] solutions

- Consider nontax factors

IRAC – issue, [blank_start]rule[blank_end], analysis, [blank_start]conclusion[blank_end]

Responda

-

problem

-

relevant

-

completed

-

sources

-

law

-

facts

-

interpretation

-

weight

-

alternative

-

rule

-

conclusion

Questão 22

Questão

Assess tax law sources

Internal revenue code – [blank_start]highest[blank_end] authority

Treasury regulations – taxpayer has burden of [blank_start]proof[blank_end]

1. Final – force and effect of law, [blank_start]highest[blank_end] admin authority, substantial weight

2. Temp – can be [blank_start]cited[blank_end], given considerable weight

3. Prop – not [blank_start]binding[blank_end] on taxpayer and IRS

Judicial sources – have to look at level of court case, taxpayer residence, type of decision

1. Novel tax issue = more [blank_start]weight[blank_end] vs tax court memo decision

2. Weight of authority

3. The [blank_start]newer[blank_end] the case has more weight

4. Have to look at subsequent [blank_start]history[blank_end]

Other administrative sources

1. Revenue rulings, private letter rulings, notices from IRS

2. Does not carry as much [blank_start]weight[blank_end]

3. Can be overturned and has been

Unofficial sources

1. [blank_start]Secondary[blank_end] sources

2. Cannot cite, carry no [blank_start]weight[blank_end]

3. Can help understand but can’t be used

IRS publications

1. Carry no [blank_start]weight[blank_end], IRS aren’t bound by these

Tax memo layout

Facts

i. do not simply cut & paste facts given

ii. glean only [blank_start]relevant[blank_end] facts

iii. Provide necessary background

iv. Facts might influence research answer

Issues

Authorities

i. List out authorities & apply it to client’s fact

Conclusion

Analysis

i. start with [blank_start]highest[blank_end] authority, and then follow by decreasing authorities

Responda

-

highest

-

proof

-

highest

-

cited

-

binding

-

weight

-

newer

-

history

-

weight

-

Secondary

-

weight

-

weight

-

relevant

-

highest

Questão 23

Questão

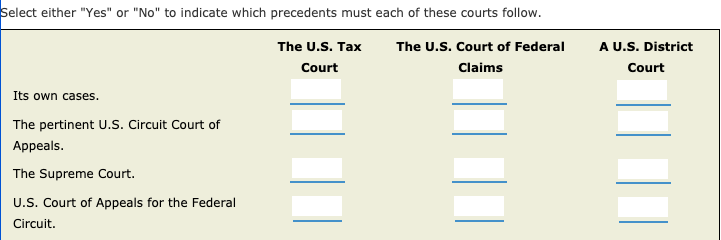

Label each box with either a Y (yes) or N (no).

{kind=link}

Responda

-

Y

-

Y

-

Y

-

N

Questão 24

Questão

Label each box with either a Y or N.

{kind=link}

Responda

-

Y

-

Y

-

Y

-

Y

-

N

Questão 25

Questão

Label each box with either a Y or N.

{kind=link}

Responda

-

Y

-

Y

-

Y

-

Y

-

N

Questão 26

Questão

Label each box with either a Y or N.

{kind=link}

Responda

-

N

-

Y

-

Y

-

Y

-

N

Questão 27

Questão

Label each box with either a Y or N.

{kind=link}

Responda

-

Y

-

Y

-

Y

-

N

-

Y

-

N

-

Y

-

Y

-

Y

-

Y

-

Y

-

N

Questão 28

Questão

[blank_start]____[blank_end] Interpretive Regulation.

[blank_start]____[blank_end] Legislative Regulation.

[blank_start]____[blank_end] Letter Ruling.

[blank_start]____[blank_end] Revenue Ruling.

[blank_start]____[blank_end] Internal Revenue Code.

[blank_start]____[blank_end] Proposed Regulation.

Responda

-

4

-

5

-

1

-

3

-

6

-

2

Questão 29

Questão

1. Temp.Reg. § 1.760–8T.

Type of regulation - [blank_start]1[blank_end]

Related code section - [blank_start]760[blank_end]

Regulation section number - [blank_start]8[blank_end]

Temporary - [blank_start]T[blank_end]

2.Rev.Rul. 2012–22, 2012–42 I.R.B. 731.

Revenue ruling number - [blank_start]22[blank_end]

Page - [blank_start]731[blank_end]

Issue week - [blank_start]42[blank_end]

3. Ltr.Rul. 20112540.

Letter ruling - [blank_start]40[blank_end]

Issue week - [blank_start]25[blank_end]

Year - [blank_start]2011[blank_end]

Responda

-

1

-

760

-

8

-

T

-

22

-

731

-

42

-

40

-

25

-

2011

Questão 30

Questão

a. CA–2 is an abbreviation for the [blank_start]U.S. Second Circuit Court of Appeals[blank_end] .

b. Fed.Cl. stands for [blank_start]Federal Claims Reporter[blank_end] .

c. The abbreviation aff'd stands for [blank_start]affirmed[blank_end] .

d. The abbreviation rev'd stands for [blank_start]reversed[blank_end] .

e. The abbreviation rem'd stands for [blank_start]remanded[blank_end] .

f. Cert. denied stands for [blank_start]Certiorari has been denied[blank_end] .

g. The abbreviation acq. stands for [blank_start]acquiescence[blank_end] .

h. B.T.A stands for [blank_start]Board of Tax Appeals[blank_end] .

i. USTC stands for [blank_start]Commerce Clearing House U.S. Tax Cases[blank_end] .

j. AFTR stands for [blank_start]American Federal Tax Reports[blank_end] .

k. F.3d stands for [blank_start]Federal Third Series[blank_end] .

l. F.Supp. stands for [blank_start]Federal Supplement Series[blank_end] .

m. USSC stands for the [blank_start]U.S. Supreme Court[blank_end] .

n. S.Ct. stands for [blank_start]Supreme Court Reporter[blank_end] .

o. D.Ct. stands for [blank_start]District Court decision[blank_end] .

Responda

-

U.S. Second Circuit Court of Appeals

-

Federal Claims Reporter

-

affirmed

-

reversed

-

remanded

-

Certiorari has been denied

-

acquiescence

-

Board of Tax Appeals

-

Commerce Clearing House U.S. Tax Cases

-

American Federal Tax Reports

-

Federal Third Series

-

Federal Supplement Series

-

U.S. Supreme Court

-

Supreme Court Reporter

-

District Court decision

Questão 31

Questão

a. 716 F.2d 693 (CA–9, 1983). [blank_start]Ninth Circuit Court of Appeals[blank_end]

b. 92 T.C 400 (1998). [blank_start]U.S. Tax Court[blank_end]

c. 70 U.S. 224 (1935). [blank_start]U.S. Supreme Court[blank_end]

d. 3 B.T.A. 1042 (1926). [blank_start]Board of Tax Appeals[blank_end] (old name of U.S. Tax Court).

e. T.C.Memo. 1957–169. [blank_start]Tax Court[blank_end] (memorandum decision)

f. 50 AFTR 2d 92–6000 (Cl.Ct., 1992). [blank_start]Court of Claims[blank_end]

g. Ltr.Rul. 9046036. [blank_start]Not a court decision[blank_end]

h. 111 F.Supp.2d 1294 (S.D.N.Y., 2000). [blank_start]District Court in New York[blank_end]

i. 98–50, 1998–1 C.B. 10. [blank_start]Not a court decision[blank_end]

Responda

-

Ninth Circuit Court of Appeals

-

U.S. Tax Court

-

U.S. Supreme Court

-

Board of Tax Appeals

-

Tax Court

-

Court of Claims

-

Not a court decision

-

District Court in New York

-

Not court decisions

Questão 32

Questão

United Draperies, Inc. v. Comm., 340 F.2d 936 (CA–7, 1964), aff'g 41 T.C. 457 (1963), cert. denied 382 U.S. 813 (1965).

a. In which court did this case first appear?

The U.S. [blank_start]Tax[blank_end] Court

b. Did the appellate court uphold the trial court?

[blank_start]Yes[blank_end]

c. Who was the plaintiff?

United Draperies, Inc.

d. Did the U.S. Supreme Court uphold the appellate court decision?

[blank_start]Yes[blank_end]

Responda

-

Tax

-

Yes

-

Yes

Questão 33

Questão

Using the legend provided, classify each of the following tax sources.

Legend

P = Primary tax source

S = Secondary tax source

B = Both

N = Neither

a. Sixteenth Amendment to the U.S. Constitution.

[blank_start]P[blank_end]

b. Tax treaty between the United States and India.

[blank_start]P[blank_end]

c. Revenue Procedure.

[blank_start]P[blank_end]

d. An IRS publication.

[blank_start]S[blank_end]

e. U.S. District Court decision.

[blank_start]P[blank_end]

f. Yale Law Journal article.

[blank_start]S[blank_end]

g. Temporary Regulations (issued 2018).

[blank_start]P[blank_end]

h. U.S. Tax Court Memorandum decision.

[blank_start]P[blank_end]

i. Small Cases Division of the U.S. Tax Court decision.

[blank_start]N[blank_end]

j. House Ways and Means Committee report.

[blank_start]P[blank_end]

Responda

-

P

-

P

-

P

-

S

-

P

-

S

-

P

-

P

-

N

-

P

Questão 34

Questão

income – broadly defined, taxed from whatever [blank_start]source[blank_end] derived

a. included in gross income unless there’s a statute that excludes it

b. [blank_start]loan[blank_end] proceeds are not included in gross income

exclusions – excluded from gross income and it’s never taxed

a. statutes state so

b. life insurance proceeds to beneficiary are generally [blank_start]excluded[blank_end] from gross income

i. good public policy – people are too distraught to worry about paying tax

c. interest income from state & local municipal bond is [blank_start]tax[blank_end] exempt

i. federal government is subsidizing state & local industries, provides incentive to [blank_start]buy[blank_end] bonds

deductions – not allowed unless there’s a specific tax revision

a. above the line deductions (Above adjusted gross income) – trade or [blank_start]business[blank_end] expenses are typically deductible, COGS, salaries, etc.

b. below the line deductions (below adjusted gross income) – have option of picking higher of either standard deduction or itemized deduction

i. itemized – [blank_start]personal[blank_end] expenses that are allowed by statutes to be deducted

1. medical expenses

2. mortgage interests

3. state taxes

4. charitable contributions (qualified charitable organizations)

c. qualified businesses income – certain businesses are allowed a deduction, engaged in certain industries

tax credits – amounts [blank_start]withheld[blank_end] and other prepayments

a. reduces current tax liability

5. realized & recognized income

a. deferral – income is taxed [blank_start]later[blank_end]

b. have cash on hand for current use

c. can reduce the amount of tax liability now and apply it later

Responda

-

source

-

loan

-

excluded

-

tax

-

buy

-

business

-

personal

-

withheld

-

later

Questão 35

Questão

Joshua sees on the street an envelope with $20,000 in cash and decides to keep it. Is this included in his gross income?

Responda

-

Includible

-

Excludible

Questão 36

Questão

recognition of gross income – once all 3 recognized, have to be included

a. has to be an [blank_start]economic[blank_end] benefit – included in tax return

b. must be [blank_start]realization[blank_end] – prerequisite for recognition (what period is income recognized & reduce uncertainty in calculating amount of income)

i. taxpayer engages in a transaction with another party

ii. as a result of the transaction, there is a measurable change in taxpayer’s property rights

c. no tax provision in internal revenue code that allows an [blank_start]exclusion[blank_end] or deferral

Responda

-

economic

-

realization

-

exclusion

Questão 37

Questão

Form of receipt - does it matter?

Ben installs cabinets and Rey installs carpet, they exchange services for each other and offers to do both for each other. Ben installs for Rey, Rey installs for Ben. Are their services included in their gross income?

Responda

-

Includible

-

Excludible

Questão 38

Questão

Return of capital principle – return of the cost of taxpayer capital investment of an asset is not taxed, what’s taxed is the [blank_start]difference[blank_end] between sales proceed and cost of asset

a. Bought amazon stock for $1000, sold for $2500, gain 1500

i. $1000 cost is return from their proceeds

ii. Only [blank_start]gain[blank_end] should be taxed

Economic income – takes into account the [blank_start]fair[blank_end] value of the asset less the liabilities and add back consumption

Gross income – has to be [blank_start]realized[blank_end] and recognized

Responda

-

difference

-

gain

-

fair

-

realized

Questão 39

Questão

Accounting periods

a. Individuals: [blank_start]Calendar[blank_end] year end, Jan-Dec

b. Corporation: Typically [blank_start]fiscal[blank_end] year, end on a month other than Dec

c. Partnerships & S-Corps: Typically [blank_start]calendar[blank_end] year end

3 primary accounting method for tax purposes

a. Hybrid - Combination of cash basis & [blank_start]accrual[blank_end] method

ii. If a taxpayer sells inventory, sales rev & cogs follow [blank_start]accrual[blank_end] method

iii. Rest of taxpayer’s income and expenses follows [blank_start]cash[blank_end] basis

Responda

-

Calendar

-

fiscal

-

calendar

-

accrual

-

accrual

-

cash

Questão 40

Questão

Cash receipts method - recognize income when it is actually or constructively received

Actual – have [blank_start]cash[blank_end] in hand

Constructive

a. Income has been made readily to [blank_start]taxpayer[blank_end]

b. No substantial restrictions or limitations on taxpayer’s [blank_start]control[blank_end] over the income (claims of rights doctrine)

Joshua works for the Gap, received check in mail on dec 20 2020, didn’t cash check until jan 2021

a. Recognize gross income in [blank_start]2020[blank_end] since he could’ve cashed it anytime in 2020

4. Joshua received check in dec 20 2020, saw it was postdated in Jan 2021

a. Recognize in 2021 since he can’t cash it until 2021

Advantages

1. More flexibility for taxpayer in terms of timing of recognition of income or [blank_start]deductions[blank_end]

a. Taxpayer sells goods in Dec, tells customer payment is due in Jan, do not recognize income until they receive money

b. Deferred from 2020 to 2021

Accelerate deductions to reduce taxable [blank_start]income[blank_end]

a. Pay expense in 2020 instead of 2021

b. IRS placed restrictions to how much you can defer or accelerate

3. Easier for bookkeeping purposes

iii. Loan proceeds – not includible in gross [blank_start]income[blank_end]

1. Not revenue, it’s a [blank_start]liability[blank_end]

Fair market value of assets – [blank_start]include[blank_end] in gross income

1. Instead of cash, sent to Joshua $500 in jackets, sweaters, etc.

a. Doesn’t have to be cash, form of receipt does not matter, would have to include

v. Property subject to restrictions

Receives property subject to substantial risk of forfeiture (have to return property), does not recognize in gross [blank_start]income[blank_end] the amount of property until substantial risk of forfeiture lapses

a. Maria is working and employers give her stock, if you leave within 5 years of date you were hired you have to forfeit the stock

b. Does not have to recognize until the 5 years is over and there’s income recognition

Obligation to repay – receive income and have to [blank_start]repay[blank_end] it

1. Landlord requires security deposit, but have obligation to pay back if there’s no damage to apartment

a. Does not recognize as gross income unless renter creates damage to apartment and loses their security deposit

b. Recognizes in the year he inspects and discovers damage

i. Landlord also gets a deduction in repairs and maintenance

Responda

-

cash

-

taxpayer

-

control

-

2020

-

deductions

-

income

-

income

-

liability

-

include

-

income

-

repay

Questão 41

Questão

Accrual method - Results in a better matching of revenues and [blank_start]expenses[blank_end]

b. Recognize income in the year it is [blank_start]earned[blank_end]

All events test is satisfied – all events have occurred that fixed the taxpayer’s right to receive the [blank_start]income[blank_end]

1. [blank_start]Earliest[blank_end] of one of the following dates

a. Date the taxpayer has provided services or transferred [blank_start]goods[blank_end]

b. Date the payment is [blank_start]due[blank_end]

c. Date the payment is [blank_start]received[blank_end]

ii. Income can be determined with reasonable accuracy (you know the amount)

Subsequent event

i. If it isn’t satisfied and there’s a subsequent event like a [blank_start]warranty[blank_end] taxpayer still recognizes once the elements are satisfied

1. If customer later exercises warranty, taxpayer can claim [blank_start]deduction[blank_end]

Prepaid rent & prepaid interest – paid ahead of when it is due, so recognized when payment is [blank_start]received[blank_end]

Special Rules for Accrual Method

Prepaid income: general rule

1. Financial accounting perspective: unearned/prepaid income is considered as a liability, report it when it is actually [blank_start]earned[blank_end]

2. Tax perspective: prepaid income/advance payment/unearned income is recognized in the year of [blank_start]receipt[blank_end] since all events test was satisfied & measured with reasonable accuracy

Prepaid rent and prepaid interest

1. Follow the general rule of all events test & reasonable accuracy

Advance payment for services

I.R.C. Sec. 451(c) – have to recognize the amount in the [blank_start]extent[blank_end] in which they perform services, the remainder can elect to defer only to the following [blank_start]year[blank_end]

Responda

-

expenses

-

earned

-

income

-

Earliest

-

goods

-

due

-

received

-

warranty

-

deduction

-

received

-

earned

-

receipt

-

extent

-

year

Questão 42

Questão

Advance payment for goods

Full inclusion – in the year they received, they recognized the [blank_start]full[blank_end] amount in gross income

Deferral – in taxpayer’s financial statement, if it reports income in the year of receipt, it cannot defer to following [blank_start]year[blank_end]

i. Can defer it if their financial statement reports it as a deferral to only following year

Prepaid rent or interest – recognized in year of [blank_start]receipt[blank_end]

Income sources

a. Income from personal services (earned income)

Assignment of income doctrine - The person that earns the income by performing [blank_start]services[blank_end] is taxed on income of the performance

ii. Fruit and tree metaphor

Income from property - Income from property is taxed to the [blank_start]owner[blank_end] of the property

Interest income – any interest income is [blank_start]taxable[blank_end], no matter how small

a. Interest income from a bank

b. Income producing property

Property transferred by gift – interest income is [blank_start]allocated[blank_end] by donor and giftee based on number of days each have held the property

Property transferred – seller recognizes interest income on date of [blank_start]sale[blank_end]

Dividends

Qualified dividends – subject to [blank_start]preferential[blank_end] tax rate, lower than ordinary income tax rate, depends on taxpayer’s ordinary income

i. 0, 15, 20%

Stock gifted before date of record

i. Dividends has ripen and belongs to the [blank_start]donor[blank_end] to be taxed

Responda

-

full

-

year

-

receipt

-

services

-

owner

-

taxable

-

allocated

-

sale

-

preferential

-

donor

Questão 43

Questão

Life insurance proceeds - Generally [blank_start]excludable[blank_end] from gross income

Exceptions to exclusion

Owners [blank_start]cancels[blank_end] policy and takes cash surrender value

Cash surrender value – if owner voluntarily terminates their policy and can cash it out

Transfers for valuable consideration - transfers to another [blank_start]party[blank_end] for money

Accelerated death benefit – if the taxpayer is insured on the policy, receives the benefit on result of transfer to someone else

1. receives proceeds from the insurance & is not [blank_start]taxable[blank_end]

2. Person is terminally or chronically ill and transfers to another person

Terminally ill: dying within 24 months due to a [blank_start]diagnosis[blank_end]

a. Can use benefit for whatever they want and still [blank_start]excludable[blank_end]

Chronically ill: cannot perform certain daily [blank_start]tasks[blank_end]

a. benefits have to be used for long term [blank_start]care[blank_end]

interest on life insurance proceeds

i. leaves it with insurance company and choose to receive install payments w/ interest

ii. principal amount excludable, interest is [blank_start]taxable[blank_end]

tax benefit rule – if a taxpayer, in one year, gets the tax benefit of a deduction and then in a later year recovers all or part of amount, in that year of recovery, have to include the amount of the recovery in [blank_start]income[blank_end]

Responda

-

excludable

-

cancels

-

party

-

taxable

-

diagnosis

-

excludable

-

tasks

-

care

-

taxable

-

income

Questão 44

Questão

Interest on state & local government obligations

Interest from municipal bonds – [blank_start]excludable[blank_end] from gross income

b. Its constitutional to tax bonds but never amended the laws

c. It encourages people to buy their bonds even if their interest rates are [blank_start]lower[blank_end]

Us treasury bill & bonds are still [blank_start]taxable[blank_end] at federal level

One state can tax interest [blank_start]income[blank_end] on bonds from another state

i. Want to discourage you from buying out-of-state bonds

Responda

-

excludable

-

lower

-

taxable

-

income

Questão 45

Questão

Imputed Interest on below-market loans - Shifting taxes from high rate to low rate, using below-market loans

i. Weren’t charging the appropriate [blank_start]interest[blank_end] rate

ii. Lend money to another party w/ low tax rate w/o charging interest

iii. Creating tax [blank_start]savings[blank_end] as a unit

Imputed interest rules

i. Since lender is not charging imputed interest, government will impute [blank_start]interest[blank_end] themselves (deemed what they think is appropriate)

ii. Amount that would have been charged at the [blank_start]federal[blank_end] rate – what is actually

Applies to:

1. Gift loans

2. Compensation-related loans

3. Corporate-shareholder loans

4. Tax avoidance loans

Responda

-

interest

-

savings

-

interest

-

federal

Questão 46

Questão

Gift loan

1. Loan proceeds – 200,000

2. AFR 10%

3. Imputed interest 20,000

4. expense of [blank_start]borrower[blank_end]

a. Used for personal reasons, interest expense not [blank_start]deductible[blank_end]

b. Lender is deemed to have interest [blank_start]income[blank_end] of 20000 taxed at their rate

c. Lender paid a gift of 20,000, not [blank_start]deductible[blank_end]

d. Borrower received a gift of 20,000 [blank_start]excludible[blank_end] from gross income

5. IRS gets money from interest [blank_start]income[blank_end] of lender

6. Motive of loan: gift

Responda

-

borrower

-

deductible

-

income

-

deductible

-

excludible

-

income

Questão 47

Questão

Employer to Employee – compensation-related loans

1. Loan proceeds – 200,000

2. AFR 10%

3. Imputed interest 20,000

4. Borrower, int of 20,000

a. Used for personal reasons, not [blank_start]deductible[blank_end]

5. Lender has interest [blank_start]income[blank_end] of 20,000 taxed at ordinary income tax rate

Motive of loan

a. lender considers it as [blank_start]deductible[blank_end] compensation expense

b. borrower receives compensation [blank_start]income[blank_end] of 20,000, taxed at ordinary income tax rate

7. IRS gets money from compensation income of [blank_start]borrower[blank_end]

Corporation to shareholder – corporate-shareholder loans

1. Loan proceeds – 200,000

2. AFR 10%

3. Imputed interest 20,000

a. Shareholder has 20,000 interest expense, not [blank_start]deductible[blank_end] for personal reasons

b. Corporation received interest [blank_start]income[blank_end] of 20,000 taxed at ordinary rate

Motive:

a. Deems corporation pays a 20,000 [blank_start]dividend[blank_end], not deductible

b. Shareholder deemed to receive dividend [blank_start]income[blank_end] of 20,000 subject to preferential rate at 0, 15, or 20% depending on ordinary rate

IRS gets money from interest [blank_start]income[blank_end] of Corporation & dividend [blank_start]income[blank_end] of shareholder

Responda

-

deductible

-

income

-

deductible

-

income

-

borrower

-

deductible

-

income

-

dividend

-

income

-

income

-

income

Questão 48

Questão

Exceptions

De minimis exception – for [blank_start]admin[blank_end] convenience

1. $10,000 or less, applies to all [blank_start]3[blank_end] loans

2. Cannot be used for tax avoidance purposes or to purchase income-producing [blank_start]assets[blank_end]

Aggregate loans

1. $100,000 or less

2. Applies only to [blank_start]gift[blank_end] loans between individuals

3. Imputed interest is capped at a ceiling in the amount of borrower’s net investment [blank_start]income[blank_end]

4. If borrower’s net investment income is $1000 or [blank_start]less[blank_end], imputed interest rules do not apply

Responda

-

admin

-

3

-

assets

-

gift

-

income

-

less

Questão 49

Questão

CODI (cancellation of debt income - Discharge of indebtedness – cancellation of debt forgiveness of debt)

General rule: Amount is [blank_start]included[blank_end] in gross income, no obligation to repay

If taxpayer transfers officiated property in satisfaction of debt

i. Government views it as if sold as property as gain or loss & took money from sale and repaid debt, not [blank_start]CODI[blank_end] treated as a sale

Foreclosure – treated as [blank_start]forced[blank_end] sale, have to recognize gain or loss on forced sale

Special situations:

Creditors’ gifts – borrower borrows money from lender, lender decides to cancel debt

1. Treated as a [blank_start]gift[blank_end] if canceled out of love, affection, respect, not subject to tax

2. If business canceled debt for business reasons or expediency, has to be considered as [blank_start]CODI[blank_end]

Seller’s cancellation

1. Canceled all or part of debt, it is considered as purchase price [blank_start]reduction[blank_end]

2. When later sold, has to recalculate gain or loss from the new basis

3. Not [blank_start]CODI[blank_end]

Shareholder’s cancellation of corporation debt

1. Shareholder loaning money to corp

2. Treated as if shareholder made an additional capital contribution

3. Not [blank_start]CODI[blank_end]

4. Shareholder basis in stock increases

Forgiveness of certain student loans

1. If student stays within state and practices for certain number of years, they’ll cancel the debt

2. [blank_start]Excludable[blank_end] from gross income

Insolvency and bankruptcy – excludable to the extent that the taxpayer is insolvent

1. Liabilities exceed [blank_start]assets[blank_end]

2. Have to reduce tax attributes to extent of exclusions or to reduce basis in tax assets

Responda

-

included

-

CODI

-

forced

-

gift

-

CODI

-

reduction

-

CODI

-

CODI

-

Excludable

-

assets

Questão 50

Questão

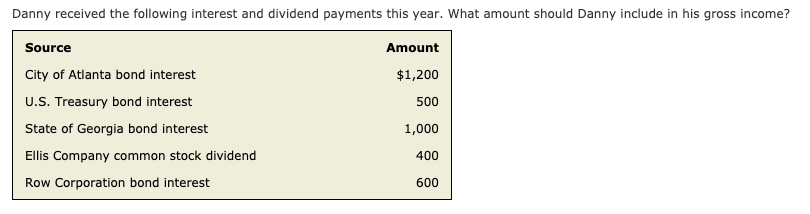

Pick the correct answer based off of the fact pattern.

{kind=link}

Responda

-

2500

-

1500

-

3700

-

2200

Questão 51

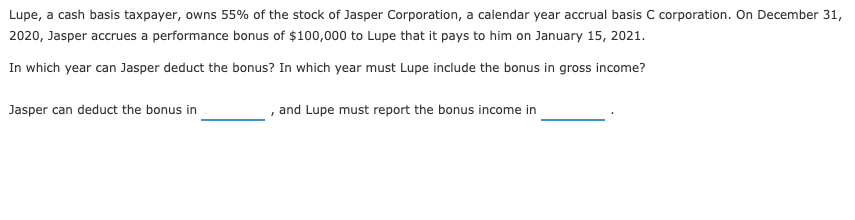

Questão

Answer the following using either 2020 or 2021.

{kind=link}

Responda

-

2021

-

2021

Questão 52

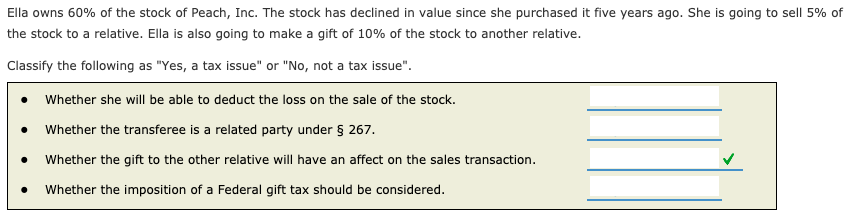

Questão

Answer the following using either Y or N.

{kind=link}

Responda

-

Y

-

Y

-

N

-

Y

Questão 53

{kind=link}

Responda

-

Yes

-

No

Questão 54

Questão

Answer each with either deductible, partially or not deductible.

{kind=link}

Responda

-

not deductible

-

deductible

-

partially

-

not deductible

-

partially

-

deductible

-

not deductible

-

deductible

-

partially

-

not deductible

-

partially

-

deductible

-

not deductible

-

deductible

-

partially

-

not deductible

-

deductible

-

partially

-

not deductible

-

deductible

-

partially

-

deductible

-

partially

-

not deductible

Questão 55

Questão

Banks Corp., a calendar year corporation, reimburses employees for properly substantiated qualifying business meal expenses. The employees are present at the meals, which are neither lavish nor extravagant, and the reimbursement is not treated as wages subject to withholdings. For the current year, what percentage of the meal expense may Banks deduct?

Responda

-

0%

-

50%

-

80%

-

100%

Questão 56

Questão

Campbell Corporation, an accrual basis calendar year corporation, had income of $450,000 for financial statement purposes in year 7. This amount included book depreciation of $50,000. The related tax depreciation was $65,000. Further, the financial statements reported $100,000 of municipal bond interest income, an expense of $2,000 for life insurance premiums on the corporation's president, charitable contributions of $5,000, excess capital losses over capital gains of $3,000, income tax penalties of $10,000, state income tax of $40,000, and Federal income tax expense of $175,000. What is the amount of Campbell's taxable income for year 7?

Responda

-

$522,000

-

$525,000

-

$530,000

-

$565,000

Questão 57

Questão

Michael Sima, a sole proprietor craftsman, purchased an amount of equipment in the current year that exceeded the maximum allowable § 179 depreciation election limit by $20,000. Sima's total purchases of property placed in service in the current year did not exceed the limit imposed by § 179. All of the property (including the equipment) was purchased in November of the current year, and Sima elected to depreciate the maximum amount of equipment under § 179. Sima had bottom-line Schedule C income of $50,000 in the current year. Which method may Sima use to depreciate the remaining equipment in the current year?

Responda

-

Sima may not depreciate any additional equipment other than the § 179 maximum in the current year and must carry forward the excess amount to use in the following taxable year.

-

MACRS half-year convention for personal property.

-

MACRS mid-quarter convention for personal property.

-

Straight-line, mid-month convention over 27.5 years for real property.

Questão 58

Questão

Stem Corp. bought a machine in February of year 7 for $20,000. Then Stem bought furniture in November of year 7 for $30,000. Both machines were placed in service for business purposes immediately after purchase. No other assets were purchased during year 7. What depreciation convention must Stem use for the machine purchased in February year 7?

Responda

-

Mid-month

-

Half-year

-

Mid-quarter

-

Full-year

Questão 59

Questão

Data, Inc., purchased and placed in service a $5,000 computer on August 24, year 3. This is the only asset purchase during the year. Section 179 expensing and bonus depreciation were not elected. Using the excerpt of the MACRS half-year convention table below, what is the MACRS depreciation in year 3 for the computer?

Recovery Period 5-Year 7-Year 10-Year

1 20% 14.29% 10%

2 32% 24.49% 18%

3 19.2% 17.49% 14.4%

Responda

-

$500

-

$715

-

$960

-

$1,000

Questão 60

Questão

Data, Inc., purchased and placed in service a $5,000 computer on August 24, year 3. This is the only asset purchase during the year. Section 179 expensing and bonus depreciation were not elected. Using the excerpt of the MACRS half-year convention table below, what is the MACRS depreciation in year 3 for the computer?

Recovery Period 5-Year 7-Year 10-Year

1 20% 14.29% 10%

2 32% 24.49% 18%

3 19.2% 17.49% 14.4%

Responda

-

$360

-

$437

-

$480

-

$960

Questão 61

Questão

Data, Inc., purchased and placed in service a $5,000 computer on August 24, year 3. This is the only asset purchase during the year. Section 179 expensing and bonus depreciation were not elected. Using the excerpt of the MACRS half-year convention table below, what is the MACRS depreciation in year 3 for the computer?

Recovery Period 5-Year 7-Year 10-Year

1 20% 14.29% 10%

2 32% 24.49% 18%

3 19.2% 17.49% 14.4%

Responda

-

$500

-

$715

-

$875

-

$1,000

Questão 62

Questão

Which statement below is correct?

Responda

-

Real property is depreciated using the half-year convention.

-

Residential real estate is depreciated over a 39-year life.

-

One-half month of depreciation is taken for the month that real property is disposed of.

-

Salvage value is considered in MACRS depreciation.

Questão 63

Questão

Which statement below is incorrect about the Section 179 deduction?

Responda

-

The Section 179 deduction is allowed even if there is a loss.

-

The Section 179 deduction may be reduced based on total purchases.

-

Real property is generally not eligible for the Section 179 deduction.

-

Corporations may elect to take the Section 179 deduction.

Questão 64

Questão

Trade or Business Deductions - Deductions must be directly connected to [blank_start]business[blank_end] activity

a. IRC Sec. 162

To be deductible:

i. Ordinary – common and accepted practice in that business industry, does not have to be [blank_start]recurring[blank_end]

ii. Necessary – [blank_start]helpful[blank_end] & appropriate to the business

iii. Reasonable – not [blank_start]excessive[blank_end] under the circumstances

Methods of Accounting

Cash

General – deductible in the year it is [blank_start]paid[blank_end]

Capital expenditures – cannot take an [blank_start]immediate[blank_end] deduction even though you paid the full amount

a. Have to capitalize and [blank_start]depreciate[blank_end]

Prepaid expense

a. Used to try to accelerate their deduction by paying in dec 2020 instead of jan 2021

One-year rule (12 month rule) – deductible in the year that it is [blank_start]paid[blank_end] provided that two elements are satisfied, both tests have to be satisfied

i. Contract period cannot last more than [blank_start]1[blank_end] year

ii. Contract period cannot extend beyond the year following the year of [blank_start]payment[blank_end] (year payment is 2020, contract cannot extend past 2021)

c. If not fully satisfied, they must prorate the prepaid expense over the contract period

d. Prepaid must be required, not voluntary

e. Does not apply to [blank_start]interest[blank_end], interest is always recognized ratably over the period

Responda

-

business

-

recurring

-

helpful

-

excessive

-

paid

-

immediate

-

depreciate

-

paid

-

1

-

payment

-

interest

Questão 65

Questão

Accrual – all 3 has to be met

All events test – all events have occurred to fix the [blank_start]liability[blank_end]

Amounts have to be measured with reasonable [blank_start]accuracy[blank_end]

Economic performance test

1. receives good and services from another [blank_start]party[blank_end] – met when 3rd party provides the goods or services to taxpayer

2. provide goods and services to another [blank_start]party[blank_end] – met when taxpayer provides the goods and services

3. rent or lease property from another [blank_start]party[blank_end] – met ratably over the rental period

4. payment liabilities – met when it is actually [blank_start]paid[blank_end]

interest expense – recognized ratably over the [blank_start]interest[blank_end] period

recurring item exception to economic performance test (make an m adjustment)

1. even though economic performance test is not [blank_start]satisfied[blank_end] yet, a taxpayer can take a deduction for a recurring item

a. the item has to be [blank_start]recurring[blank_end] and the taxpayer takes it/treats it consistently from year to year

b. the amount cannot be [blank_start]material[blank_end], cannot be a significant event

c. the all [blank_start]events[blank_end] test has to be met

d. even though economic performance test has not occurred yet, it must occur within/after [blank_start]8.5[blank_end] months year end

e. if all satisfied, can take a deduction for the item

reserves – not [blank_start]deductible[blank_end] because economic [blank_start]performance[blank_end] test has not been satisfied

1. ex. the allowance for doubtful accounts

2. estimates are not deductibles

Responda

-

liability

-

accuracy

-

party

-

party

-

party

-

paid

-

interest

-

satisfied

-

recurring

-

material

-

events

-

8.5

-

deductible

-

performance

Questão 66

Questão

Expenses accrued to related parties – will be disallowed a [blank_start]deduction[blank_end]

a. Irc section 267

b. Family members, spouses, siblings, ancestors, descendants

c. Shareholders that own more than 50% of a C-Corp

d. Controlled group

Election to Expense Assets – Section 179

a. Have to capitalize [blank_start]asset[blank_end] and depreciate over useful

b. Taxpayer can opt to get an immediate [blank_start]deduction[blank_end] up to 1040000 for 2020

c. Annual election

d. Applies to tangible personalty used in trade of business

e. Have to reduce the basis of the asset you’re able to claim

Limitations

i. Phaseout limitation (2590000 for 2020)

1. The immediate expense, dollar for dollar, to the extent of the [blank_start]tangible[blank_end] personalty is over 2590000

ii. Taxable income limitation – the taxpayer is further limited in their [blank_start]deduction[blank_end] to the taxable income of the business

Responda

-

deduction

-

asset

-

deduction

-

tangible

-

deduction

Questão 67

Questão

Additional First-Year Depreciation (Bonus Depreciation)

a. In addition to 179 or instead of 179

b. Can immediately deduct [blank_start]100[blank_end]% of the cost of qualified property

c. Qualified property – property that has class life of 20 years or less

i. Include new and used but newly [blank_start]acquired[blank_end]

d. If 179 is taken, bonus depreciation is computed after

e. Claim bonus in the year assets were placed in [blank_start]service[blank_end]

f. After bonus, any remaining basis is calculated using MACRS

Excessive Executive Compensation

a. Government concerned that c-corps were claiming huge deductions for executive compensations

b. Put a $1 million [blank_start]ceiling[blank_end] a C-Corp can take for executive compensation per tax year, per covered executive

Exceptions – before Tax cuts and Jobs Act 2019 taxpayers found a way around this

i. Would pay a $1 million to executive, 2 million on performance-based, 1 million on commission-based; would get around the ceiling by recategorizing the compensation

ii. If contract was established in 2017, it would be [blank_start]grandfathered[blank_end] in

iii. After tax cuts and jobs act, performance based and commission would be included in ceiling

Before: Established by 11/2/2017, you will be grandfathered in and allowed

a. Compensation 1,000,000; performance based 2,000,000; deducting a total of 3 million on tax return

After:

a. No longer the way to get around

b. Compensation 900,000; performance based 2,100,000; can only deduct 1,000,000

Exceptions – can still take deductions for these and not included in the ceiling

1. Payments to qualified [blank_start]retirement[blank_end] plans

2. Payments excludable from gross [blank_start]income[blank_end]

a. Health benefits, medical benefits

Responda

-

100

-

acquired

-

service

-

ceiling

-

grandfathered

-

retirement

-

income

Questão 68

Questão

Cost Recovery

a. Tangible Assets: assets that will benefit more than [blank_start]1[blank_end] period has to be capitalized and depreciated

i. Allocated over useful life of [blank_start]assets[blank_end]

ii. Use an [blank_start]accelerated[blank_end] form for depreciation

Intangible assets: copyrights & patents are [blank_start]amortized[blank_end]

c. No deduction for land/assets with no [blank_start]determinable[blank_end] life

Nature Property

Real property (realty) – land and [blank_start]buildings[blank_end]

Personal property (personalty)– any asset that is not [blank_start]realty[blank_end]

i. Not to be confused with [blank_start]personal[blank_end] use property

ii. Write off are not allowed for personal use assets

1. Personal use can be realty or [blank_start]personalty[blank_end]

c. In order to be deductible, has to be a trade or business asset or for the production of [blank_start]income[blank_end]

d. Has to have a limited life & [blank_start]determinable[blank_end] useful life

i. Subject to wear, tear and obsolesce

Property basis – [blank_start]adjusted[blank_end] cost basis

Asset cost basis – accumulated [blank_start]depreciation[blank_end] = adjusted cost basis

1. All expenses to purchase the asset and make it available for intended use

a. Sales tax, insulation costs

ii. Reduced by the amount of depreciation that is [blank_start]taken[blank_end] or could’ve been taken

1. What is deducted as depreciation expense or what could’ve been but didn’t

Responda

-

1

-

assets

-

accelerated

-

amortized

-

determinable

-

buildings

-

realty

-

personal

-

personalty

-

income

-

determinable

-

adjusted

-

depreciation

-

taken

Questão 69

Questão

MACRS: tax depreciation – form of accelerated depreciation

a. Taxpayer gets more [blank_start]depreciation[blank_end] upfront in the earlier years of the asset and slows down in the later years

Personal property

i. What is class [blank_start]life[blank_end] of the asset – determined by revenue procedures

ii. What the method of [blank_start]depreciation[blank_end] – double declining balance method, twice the straight line

1. Use tables the incorporate the methods

What is the convention

1. Half year

a. In the year, the asset is placed in service, taxpayer will get half-year worth of depreciation

i. Placed in jan or dec still gets [blank_start]half[blank_end] year

b. In the year of disposal, will get a [blank_start]half[blank_end] year worth of depreciation

i. Jan vs dec will still get a half year worth

i. 1st percentages and last percentages are half years

ii. Everything in the middle is not half year, it is full year

iii. If you dispose in the middle, you’d have to divide the percentage in half

Mid quarter

a. Applies if more than [blank_start]40[blank_end]% of personalty is placed in service during last quarter of the year

i. Taxpayers were buying in dec 2020 instead of jan 2021

b. Treats assets as if it were placed into service in the middle of the quarter

i. Placed in jan, 1st quarter

c. Disposal - Gets depreciation in half of the quarter in the [blank_start]quarter[blank_end] of disposal

i. Get depreciation expense in 1, 2, .5 of quarter 3

ii. Full year’s depreciation x [(quarter in which asset disposed - .5)/4]

d. Year 1 already takes account in the half quarter like half-year

i. First – 12.5% = .5/4

ii. Second – 37.5% = 1.5/4

iii. Third – 62.5% = 2.5/4

iv. Fourth – 87.5% = 3.5/4

iv. DB – gets more in the beginning and then switches to straight-line

Responda

-

depreciation

-

life

-

depreciation

-

half

-

half

-

40

-

quarter

Questão 70

Questão

MACRS – Realty

a. Residential rental – [blank_start]27.5[blank_end] years

i. Property for which [blank_start]80[blank_end]% or more of gross rental revenues are from non-transient dwelling units like an apartment building

ii. Straight-line method

iii. Mid-month

Nonresidential realty 0 31.5 years or [blank_start]39[blank_end] years

i. Depends on when asset was placed in service – look at the years

ii. Straight-line method

iii. Mid-month

1. April 25 but treated as April 15

2. Calculate a full year’s depreciation x [(month in which asset disposed - .5)/12]

Amortization

a. Sec. 197 Intangibles

b. Intangible assets – assets taxpayers have acquired in the [blank_start]acquisition[blank_end] of a business

i. Goodwill, copyrights, patents

ii. Amortized on straight-line basis, [blank_start]15[blank_end] years (180 months) beginning in month intangible is acquired

Responda

-

27.5

-

80

-

39

-

acquisition

-

15

Questão 71

Questão

Investigation of a business - Investigation expenses a taxpayer occurs if they’re looking to [blank_start]expand[blank_end] an existing line of business or looking to starting a brand-[blank_start]new[blank_end] line of business

b. Government concerned that what taxpayers are claiming to be investigation expenses but are actually [blank_start]vacation[blank_end] expenses

d. Depends on if taxpayer is already in a similar line of business of which that they are investigating

i. Regardless of whether acquired or not acquired, can deduct the [blank_start]entire[blank_end] amount of expenses

TP not in a similar line of business or same business being investigated

i. Depends on whether acquired or not acquired

Not acquired: no [blank_start]deduction[blank_end] allowed

1. Gov’t concerned that taxpayers were trying to claim personal vacation expenses

Acquired: can take [blank_start]immediate[blank_end] deduction subject phaseout

1. Election – 5,000 of expense

2. Phase-out – 5,000 dollar for dollar to the extent the investigation expense [blank_start]exceeds[blank_end] 50,000

a. Remainder is amortized over [blank_start]180[blank_end] months (15 years)

b. Start in month business is acquired

Responda

-

expand

-

new

-

vacation

-

entire

-

deduction

-

immediate

-

exceeds

-

180

Questão 72

Questão

Interest Relating to Tax-Exempt Income

a. A taxpayer takes out a loan, uses loan proceeds, and bank is charging an interest to buy tax exempt income producing property then the interest expense [blank_start]deductible[blank_end] is disallowed

Research and experimental expenditures

a. R&E expenditures

i. Has to be for the [blank_start]development[blank_end] and/or improvement of product, invention, formula

ii. Does not include ordinary test, [blank_start]quality[blank_end] controls, advertising, promotions

Before 1/1/2022, three alternative treatments

i. Deduct the [blank_start]entire[blank_end] amount in the year paid or incurred

1. Most taxpayers choose to do this

Defer and amortize R&D expenses

1. Over a period of at least [blank_start]60[blank_end] months (5 years)

a. Begins in the month taxpayer expects to receive a [blank_start]benefit[blank_end]

2. Over 10-year period

a. begins in year [blank_start]paid[blank_end] or incurred

capitalize

1. on the balance but no deductions until the project is [blank_start]abandoned[blank_end] or deemed worthless

2022 onwards, 1 way to treat – TCJA 2017

i. No expense method

ii. [blank_start]Capitalize[blank_end] & amortized

iii. Over [blank_start]60[blank_end] months (5 years) domestic R&D

1. 15 years for foreign research expenses

2. Begin in the mid-point in the year that it was [blank_start]paid[blank_end] or incurred

Business Interest Expense Limitation

a. Take out loans and drive down taxable income, deduct interest [blank_start]expense[blank_end] related to the loans

b. TCJA 2017

c. The amount of deduction is limited to the sum of business interest income + [blank_start]adjusted[blank_end] taxable income

d. CARES Act: 2019 & 2020 [blank_start]50[blank_end]% of adjusted taxable income

e. 2021 onward, [blank_start]30[blank_end]% adjusted taxable income

f. [blank_start]Carryforward[blank_end] indefinitely until they can use it

g. Targeted towards [blank_start]large[blank_end] corporations

Exception: average gross receipts for the prior 3-year period of $[blank_start]26[blank_end] million or less, there will be no limitation

Responda

-

deductible

-

development

-

quality

-

entire

-

60

-

benefit

-

paid

-

abandoned

-

60

-

Capitalize

-

paid

-

expense

-

adjusted

-

50

-

30

-

Carryforward

-

large

-

26

Questão 73

Questão

Charitable Contribution Deduction – for C-Corporation

a. Also [blank_start]deductible[blank_end] from individual tax perspective

b. Qualified charitable organization – tax-exempt organizations in the [blank_start]government[blank_end]

c. Donative intent – no intention of getting anything back in [blank_start]return[blank_end]

d. Deductible in the year it is paid, regardless or cash or [blank_start]accrual[blank_end] basis

i. No [blank_start]legal[blank_end] obligation to make a charitable contribution

Exception: only applies to C-Corp, if met it can deduct amount in 2020 despite not being paid yet until 2021

1. The board of directors approve the contribution by the corporation’s year [blank_start]end[blank_end] (ex. Dec 31 2020)

a. Approves 100,000 by year-end

2. Must be made by [blank_start]15th[blank_end] day of the 4th month after year-end

a. April 15th

Property contributions

i. Long term capital gain property – capital asset held for more than 1 [blank_start]year[blank_end] (like stock) then the amount is the fair market value of that property subject to limitations

1. Taxed at [blank_start]preferential[blank_end] rates

ii. Ordinary income property (like inventory) – taxed at [blank_start]ordinary[blank_end] rates

1. Amount is adjusted basis of that property subject to limitations

a. Depends on what year