3989011

Descrição

Quiz por jmkerstell, atualizado more than 1 year ago

|

|

Criado por jmkerstell

quase 9 anos atrás

|

|

Questão 1

Questão

Which of the following items may be confused with cash but is normally categorized under a different balance sheet caption (not categorized as cash)?

Responda

-

Foreign currency on deposit in a foreign bank.

-

Un-deposited credit card sales receipts.

-

Postdated checks.

-

Negotiable checks.

Questão 2

Questão

The definition of cash equivalents includes:

I. available to pay current obligations

II. short-term, highly liquid investments

III. so near maturity that there is little risk of changes in value because of changes in interest rates

Responda

-

I and II.

-

II and III.

-

I, II, and III.

-

I and III.

Questão 3

Questão

Which of the following is an important element of internal control over cash?

Responda

-

They are required for all companies.

-

They include a petty cash system.

-

They guarantee that a company's financial reports are reliable.

-

All of the choices are correct regarding internal controls.

Questão 4

Questão

Non-trade receivables include [blank_start]deposits with utilities[blank_end] while trade receivables include [blank_start]accounts receivable[blank_end].

Responda

-

deposits with utilities

-

notes receivable

-

accounts receivable

-

accounts receivable

-

advances to employees

-

loans made by nonfinancial companies

Questão 5

Questão

Revenue recognition criteria include [blank_start]realization must have occurred[blank_end] and [blank_start]must be earned[blank_end] which result in revenue generally being recognized when [blank_start]the product or service is delivered[blank_end].

Responda

-

realization must have occurred

-

readily available for general use

-

must be earned

-

not bound by any restrictions

-

the product or service is delivered

-

all defective items have been returned

Questão 6

Questão

Cash (sales) discounts [blank_start]induce prompt payment[blank_end] and are recorded using either the gross price method or the net price method.

Responda

-

induce prompt payment

-

are price reductions for large purchases

-

hide real prices from competitors

Questão 7

Questão

When a company records accounts receivable using the gross price method and the customer pays and takes advantage of the discount, which of the following is true?

Responda

-

The company records accounts receivable and sales at the net invoice price and no further adjustment is required.

-

No adjustment is needed because the amount of cash received is equal to the recorded amount of the receivable.

-

The company credits an account entitled Sales Discounts Not Taken.

-

The difference between the cash received and the original amount of accounts receivable is recorded as a debit to Sales Discounts Taken.

Questão 8

Questão

A [blank_start]sales allowance[blank_end] occurs when a customer retains defective goods; conceptually, the company should estimate and record in the period of sale so as to properly report sales revenue and ending accounts receivable.

Responda

-

sales allowance

-

cash discount

-

sales return

Questão 9

Questão

Which of the following statements is correct with regard to the direct write-off method?

I. Allows the manipulation of income.

II. Is simple to apply.

Responda

-

I only.

-

II only.

-

I and II

-

Neither I nor II

Questão 10

Questão

Using the [blank_start]% of outstanding accounts receivable[blank_end] approach, a company considers the existing balance in the allowance account and records bad debt expense as the amount necessary to adjust the allowance to its desired balance.

Responda

-

% of outstanding accounts receivable

-

direct write-off

-

% of credit sales

Questão 11

Questão

The net realizable value of a company's accounts receivable is the balance of the accounts receivable account

I. Plus the allowance for sales returns

II. Minus the allowance for doubtful accounts

III. Plus deferred gross profit

IV. Minus allowance for sales discounts

Responda

-

I, II, and III

-

II and IV

-

II, III, and IV

-

I, II, III, and IV

Questão 12

Questão

What method of bad debt estimation categorizes individual accounts receivable based on the length of time outstanding? Why is this length of time an important factor?

Responda

-

Aging is based on the fact that credit risk tends to decrease with the age of the account receivable.

-

A company that "ages" its accounts receivable first classifies the individual accounts receivable based on the length of time they have been outstanding and then estimates the allowance for bad debts by applying appropriate bad debts percentages to each age category.

-

Aging is a relatively simple balance sheet approach which bases the estimated expense on the historical relationship between the actual bad debts and the outstanding accounts receivable balance at the end of the year.

-

All of the choices are correct regarding aging of accounts receivable.

Questão 13

Questão

When accounts receivable are sold or factored

Responda

-

the transaction is accounted for as a lending agreement.

-

the transferor records a gain or loss.

-

the creditor can require the amounts collected from the accounts receivable be used to repay the amount owed.

-

the proceeds from the transfer of financial assets are recorded as a liability.

Questão 14

Questão

Accounts receivable are considered sold when

I. the transferred assets are put beyond the reach of the transferor.

II. the transferee has the right to sell the transferred assets.

III. the transferee has recourse against the transferor.

IV. the transferor does not maintain effective control over the transferred assets.

Responda

-

I, II, III, and IV.

-

I, III, and IV.

-

I, II, and III.

-

I, II, and IV

Questão 15

Questão

Unlike accounts receivable, notes receivable [blank_start]are negotiable[blank_end] and usually [blank_start]involve interest[blank_end].

Responda

-

are negotiable

-

arise from the company's operations

-

involve interest

-

are grouped as trade or nontrade in the

Questão 16

Questão

Sally Company accepted a 3-month, non-interest-bearing note receivable on December 1. If Sally's year end is December 31, what entry would be recorded

Responda

-

debit Cash and credit Interest Revenue.

-

debit Interest Expense and credit Cash.

-

debit Discount on Note Receivable and credit Interest Revenue.

-

debit Interest Expense and credit Discount on Note Receivable.

Questão 17

Questão

If a note is [blank_start]transferred with recourse[blank_end], the company reports a(n) [blank_start]liability[blank_end] at the estimated amount it would have to pay the buyer.

Responda

-

transferred with recourse

-

assigned

-

liability

-

expense

Questão 18

Questão

When a note receivable is transferred, the cash proceeds equal the [blank_start]maturity value[blank_end] of the note [blank_start]less[blank_end] a discount. The discount is determined by multiplying the discount rate times the [blank_start]maturity value of the note[blank_end] for the discount period.

Responda

-

maturity value

-

present value

-

less

-

plus

-

maturity value of the note

-

present value of the note

-

face value of the note less total intere

Questão 19

Questão

When financial assets are transferred, U.S. GAAP focuses on whether [blank_start]control has been surrendered[blank_end] in determining whether the transfer is accounted for as a secured borrowing or a sale. Under IFRS, the derecognition of a financial asset is based on whether the seller has transferred substantially all the risks and rewards of ownership.

Responda

-

control has been surrendered

-

an accounting mismatch arises

-

the seller has transferred risk/rewards

Questão 20

Questão

Which of the following transactions would not be appropriate for the use of a petty cash system?

Responda

-

Paying for postage.

-

Paying cab fare home for late-working employees.

-

Paying for NSF checks.

-

Paying for small amounts of office supplies.

Questão 21

Questão

Why are actual expenses, rather than the petty cash account, debited when the fund is replenished?

Responda

-

Because the entry records the expenses incurred for the period.

-

Because this process provides an external, independent control to verify a company's cash balance.

-

Because the petty cash fund is always carried in the company's accounting records at its current remaining balance.

-

All of the choices are correct regarding the petty cash account.

Questão 22

Questão

Differences between the cash balance listed on a company's bank statement and the balance shown in the company's cash account include all of the following except:

Responda

-

Outstanding checks.

-

Bank service charge expense.

-

Recourse liability expense.

-

Deposits in transit.

Questão 23

Questão

Which of the following items appearing on a bank reconciliation would require the company to make an adjusting entry?

Responda

-

Bank service charge.

-

Deposit in transit

-

Outstanding checks.

-

All of the choices would require an adjusting entry.

Questão 24

Questão

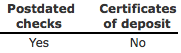

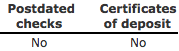

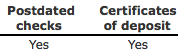

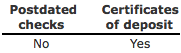

Which of the following items should be classified under the heading of cash on the balance sheet?

Responda

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Questão 25

Questão

Greenfield Company had the following cash balances at December 31, 2016:

- Cash in banks: $1,300,000

- Petty cash funds (all funds were reimbursed on December 31, 2016): 20,000

- Cash legally restricted for additions to plant (expected to be disbursed in 2018): 2,000,000

Cash in banks includes $300,000 of compensating balances against short-term borrowing arrangements at December 31, 2016. The compensating balances are not legally restricted as to withdrawal by Greenfield.

In the current assets section of Greenfield's December 31, 2016, balance sheet, what total amount should be reported as cash?

Responda

-

$3,020,000

-

$1,320,000

-

$3,320,000

-

$1,020,000

Questão 26

Questão

Cash on hand is [blank_start]included in[blank_end] cash on the company's balance sheet.

Checking account is [blank_start]included in[blank_end] cash on the company's balance sheet.

Sinking fund is [blank_start]excluded from[blank_end] cash on the company's balance sheet.

Savings account is [blank_start]included in[blank_end] cash on the company's balance sheet.

Certificates of deposit is [blank_start]excluded from[blank_end] cash on the company's balance sheet.

Negotiable checks is [blank_start]included in[blank_end] cash on the company's balance sheet.

Compensating balance is [blank_start]excluded from[blank_end] cash on the company's balance sheet.

Travel advance is [blank_start]excluded from[blank_end] cash on the company's balance sheet.

Deposits in a foreign bank is [blank_start]included in[blank_end] cash on the company's balance sheet.

Responda

-

included in

-

excluded from

-

included in

-

excluded from

-

excluded from

-

included in

-

included in

-

excluded from

-

excluded from

-

included in

-

included in

-

excluded from

-

excluded from

-

included in

-

excluded from

-

included in

-

included in

-

excluded from

Questão 27

Questão

Which of the following would not be included with cash and cash equivalents on the balance sheet?

Responda

-

unrestricted funds on deposit.

-

checks.

-

sinking funds.

-

undeposited credit card sales receipts.

Questão 28

Questão

A short-term investment is considered a cash equivalent if it is

Responda

-

highly liquid.

-

readily convertible into an unknown amount of cash.

-

within 120 days of maturity.

-

all of these choices.

Questão 29

Questão

Internal cash control procedures are

Responda

-

required by law for publicly traded companies.

-

enhanced by routine reviews of the accuracy of recorded cash transactions.

-

enhanced by the separation of employee duties.

-

all of these choices.

Questão 30

Questão

All of the following are a cash control over receipts except

Responda

-

daily recording of all cash receipts in the accounting records.

-

daily deposit of all receipts in the company’s bank account.

-

immediate counting of receipts by the person opening the mail or the salesperson using the cash register, and subsequent verification by an independent person.

-

making all payments by check (or electronic funds transfer) so there is a record for every company expenditure.

Questão 31

Questão

Which of the following would not be classified as a trade receivable?

Responda

-

customer accounts receivable for the sale of merchandise on account.

-

short-term customer note receivable in exchange for merchandise.

-

accrued interest on investments.

-

obligations arising from customers for services rendered.

Questão 32

Questão

Which of the following is treated as a cash sale?

Responda

-

credit card sale involving a bank credit card.

-

credit card sale involving the store's credit card.

-

sale involving the receipt of a note receivable.

-

all of these choices.

Questão 33

Questão

When a customer retains defective goods at a reduced price, the reduction is called a

Responda

-

sales discount.

-

sales return.

-

sales allowance.

-

trade discount.

Questão 34

Questão

Using the net price method, which account does not apply when recording the receipt of payment on account after the discount period?

Responda

-

Accounts Receivable.

-

Cash.

-

Sales Discounts Not Taken.

-

Sales Revenue.

Questão 35

Questão

Using the gross price method, the journal entry for a sale on account for $10,000 under the terms 2/10, n/30 would include a

Responda

-

debit to Cash for $9,800.

-

debit to Accounts Receivable for $10,000.

-

debit to Accounts Receivable for $9,800.

-

debit to Sales Revenue for $9,800.

Questão 36

Questão

Which of the following is not true of the account Allowance for Doubtful Accounts?

Responda

-

It is an expense account.

-

It is reported on the balance sheet.

-

It is debited when writing off an uncollectible account receivable.

-

Its balance is deducted from the balance in Accounts Receivable to determine the net realizable value of the company’s receivables.

Questão 37

Questão

Using the allowance method, which is the proper journal entry for writing off an uncollectible account?

Responda

-

Debit Bad Debt Expense; credit Accounts Receivable.

-

Debit Bad Debt Expense; credit Allowance for Doubtful Accounts.

-

Debit Allowance for Doubtful Accounts; credit Accounts Receivable.

-

Debit Accounts Receivable; credit Allowance for Doubtful Accounts.

Questão 38

Questão

Which of the following is not true of the direct write-off method?

Responda

-

It is the preferred method under GAAP.

-

Bad debt expense is recorded only when a specific customer account is determined uncollectible.

-

It matches bad debts of previous sales against current sales.

-

An uncollectible account is written off by debiting Bad Debt Expense and crediting Accounts Receivable.

Questão 39

Questão

If the transfer of receivables does not meet the conditions of a sale, it should be accounted for as

Responda

-

secured borrowing.

-

factoring.

-

a securitization.

-

a sale with recourse.

Questão 40

Questão

If Gable Company sells $50,000 of its accounts receivable to a factor without recourse, receiving 90% value and paying a 10% commission, the journal entry will include

Responda

-

a debit to Cash for $40,000.

-

a debit to Receivable from Factor for $5,000.

-

a debit to Factoring Expense for $5,000.

-

all of these

Questão 41

Questão

A retailer made $2,000 of bank credit card sales and is charged a 4% fee when depositing the receipts. Assuming it uses the gross price method of recording sales, the entry will include

Responda

-

a debit to Cash for $2,000. a credit to Sales Revenue for $1,920.

-

a debit to Credit Card Expense for $80.

-

none of these

Questão 42

Questão

Which of the following are true of a note receivable?

Responda

-

A note receivable gives the holder the right to collect money on demand.

-

A note receivable is not a negotiable instrument.

-

A note receivable usually does not involve interest.

-

None of these choices are true of a note receivable

Questão 43

Questão

The journal entry for the collection of a $10,000, 90-day, 10% note receivable would include

Responda

-

a debit to Cash for $10,000.

-

a credit to Notes Receivable for $9,750.

-

a credit to Interest Revenue for $250.

-

a debit to Interest Expense for $250.

Questão 44

Questão

A petty cash fund is established for $300. At the end of the accounting period, there is $50 cash and $245 in petty cash vouchers. The journal entry to replenish the fund will include

Responda

-

a debit to Petty Cash for $250.

-

a credit to Cash for $250.

-

a debit to various expenses for $245.

-

a credit to Cash Short and Over for $5.

Questão 45

Questão

On a bank reconciliation, which of the following would be deducted from the bank statement balance?

Responda

-

deposits in transit.

-

outstanding checks.

-

bank service charges.

-

a note collected by the bank.

Quer criar seus próprios Quizzes gratuitos com a GoConqr? Saiba mais.