16227808

Description

Quiz by Good Guy Beket, updated more than 1 year ago

|

|

Created by Good Guy Beket

almost 6 years ago

|

|

Question 1

Question

Accounting profit is equal to total revenue minus

Answer

-

implicit costs.

-

variable costs.

-

the sum of implicit and explicit costs.

-

explicit costs.

-

marginal costs.

Question 2

Question

Economic profit is equal to total revenue minus

Answer

-

variable costs.

-

implicit costs.

-

explicit costs.

-

marginal costs.

Question 3

Question

Nicole owns a small pottery factory. She can make 1,000 pieces of pottery per year and sell them for €100 each. It costs Nicole €20,000 for the raw materials to produce the 1,000 pieces of pottery. She has invested €100,000 in her factory and equipment: €50,000 from her savings and €50,000 borrowed at 10 per cent. (Assume that she could have loaned her money out at 10 per cent, too.) Nicole can work at a competing pottery factory for €40,000 per year. The accounting profit at Nicole's pottery factory is

Answer

-

€30,000.

-

€35,000.

-

€75,000.

-

€70,000.

-

€80,000

Question 4

Question

Nicole owns a small pottery factory. She can make 1,000 pieces of pottery per year and sell them for €100 each. It costs Nicole €20,000 for the raw materials to produce the 1,000 pieces of pottery. She has invested €100,000 in her factory and equipment: €50,000 from her savings and €50,000 borrowed at 10 percent (assume that she could have loaned her money out at 10 percent, too). Nicole can work at a competing pottery factory for €40,000 per year. The economic profit at Nicole's pottery factory is

Answer

-

€80,000.

-

€30,000.

-

€75,000.

-

€70,000.

-

€35,000.

Question 5

Question

If there are implicit costs of production,

Answer

-

accounting profit will exceed economic profit.

-

economic profit will always be zero.

-

economic profit will exceed accounting profit.

-

accounting profit will always be zero.

-

economic profit and accounting profit will be equal.

Question 6

Question

If a production function exhibits diminishing marginal product, its slope

Answer

-

is linear (a straight line).

-

becomes steeper as the quantity of the input increases.

-

could be any of these answers.

-

becomes flatter as the quantity of the input increases.

Question 7

Question

If a production function exhibits diminishing marginal product, the slope of the corresponding total-cost curve

Answer

-

is linear (a straight line).

-

could be any of these answers.

-

becomes steeper as the quantity of output increases.

-

becomes flatter as the quantity of output increases.

Question 8

Question

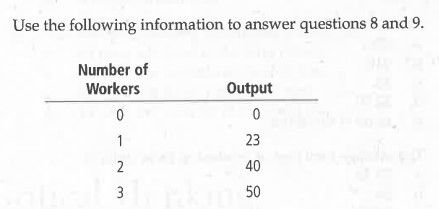

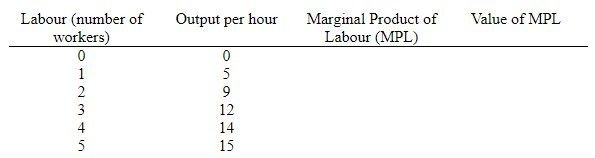

The marginal product of labour as production moves from employing one worker to employing two workers is

{kind=link}

Answer

-

10

-

0

-

23

-

40

-

17

Question 9

Answer

-

constant marginal product of labour.

-

diminishing marginal product of labour.

-

increasing returns to scale.

-

increasing marginal product of labour.

-

decreasing returns to scale.

Question 10

Question

Which of the following is a variable cost in the short run?

Answer

-

rent on the factory

-

wages paid to factory labour

-

interest payments on borrowed financial capital

-

payment on the lease for factory equipment

-

salaries paid to upper management

Question 11

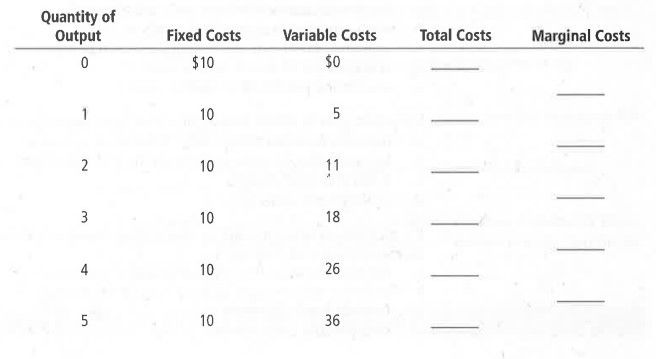

Question

The average fixed cost of producing four units is

{kind=link}

Answer

-

€2.50.

-

€26.

-

none of these answers.

-

€10.

-

€5.

Question 12

Question

The average total cost of producing three units is

Answer

-

€28.

-

€6.

-

€3.33.

-

€18.

-

€9.33.

Question 13

Question

The marginal cost of changing production from three units to four units is

Answer

-

€7.

-

€5

-

€8.

-

€9.

-

€6.

Question 14

Answer

-

two units.

-

three units.

-

one unit.

-

five units.

-

four units.

Question 15

Question

When marginal costs are below average total costs,

Answer

-

average fixed costs are rising.

-

average total costs are falling.

-

average total costs are rising.

-

average total costs are minimized.

Question 16

Question

If marginal costs equal average total costs,

Answer

-

average total costs are falling.

-

average total costs are rising.

-

average total costs are maximized.

-

average total costs are minimized.

Question 17

Question

If, as the quantity produced increases, a production function first exhibits increasing marginal product and later diminishing marginal product, the corresponding marginal-cost curve will

Answer

-

be flat (horizontal).

-

slope upward.

-

slope downward.

-

be U-shaped.

Question 18

Question

In the long run, if a very small factory were to expand its scale of operations, it is likely that it would initially experience

Answer

-

an increase in average total costs.

-

diseconomies of scale.

-

economies of scale.

-

constant returns to scale.

Question 19

Question

The efficient scale of production is the quantity of output that minimizes

Answer

-

average fixed cost.

-

average total cost.

-

average variable cost.

-

marginal cost.

Question 20

Question

Which of the following statements is true?

Answer

-

All costs are fixed in the short run.

-

All costs are variable in the long run.

-

All costs are variable in the short run.

-

All costs are fixed in the long run.

Question 21

Question

The market for hand tools (such as hammers and screwdrivers) is dominated by Draper, Stanley, and Craftsman. This market is best described as

Answer

-

monopolistically competitive.

-

a monopoly.

-

an oligopoly.

-

competitive.

Question 22

Question

A market structure in which many firms sell products that are similar but not identical is known as

Answer

-

monopolistic competition.

-

monopoly.

-

perfect competition.

-

oligopoly.

Question 23

Question

If oligopolists engage in collusion and successfully form a cartel, the market outcome is

Answer

-

the same as if it were served by competitive firms.

-

efficient because cooperation improves efficiency.

-

the same as if it were served by a monopoly.

-

known as a Nash equilibrium.

Question 24

Question

Suppose an oligopolist individually maximizes its profits. When calculating profits, if the output effect exceeds the price effect on the marginal unit of production, then the oligopolist

Answer

-

should produce more units.

-

has maximized profits.

-

is in a Nash equilibrium.

-

should produce fewer units.

-

should exit the industry.

Question 25

Question

As the number of sellers in an oligopoly grows larger, an oligopolistic market looks more like

Answer

-

monopoly.

-

a competitive market.

-

monopolistic competition.

-

a collusion solution.

Question 26

Question

When an oligopolist individually chooses its level of production to maximize its profits, it produces an output that is

Answer

-

more than the level produced by a monopoly and less than the level produced by a competitive market.

-

less than the level produced by a monopoly and more than the level produced by a competitive market.

-

less than the level produce by either monopoly or a competitive market.

-

more than the level produced by either monopoly or a competitive market.

Question 27

Question

When an oligopolist individually chooses its level of production to maximize its profits, it charges a price that is

Answer

-

more than the price charged by either monopoly or a competitive market.

-

less than the price charged by either monopoly or a competitive market.

-

more than the price charged by a monopoly and less than the price charged by a competitive market.

-

less than the price charged by a monopoly and more than the price charged by a competitive market.

Question 28

Question

As the number of sellers in an oligopoly increases,

Answer

-

output in the market tends to fall because each firm must cut back on production.

-

the price in the market moves further from marginal cost.

-

collusion is more likely to occur because a larger number of firms can place pressure on any firm that defects.

-

the price in the market moves closer to marginal cost.

Question 29

Question

A situation in which oligopolists interacting with one another each choose their best strategy given the strategies that all the other oligopolists have chosen is known as a

Answer

-

Nash equilibrium.

-

dominant strategy.

-

cartel.

-

collusion solution.

Question 30

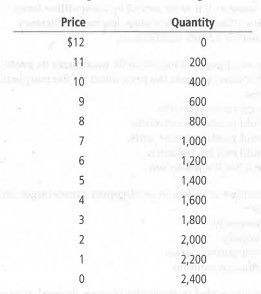

Question

Under competition, the price and quantity in this market would be

{kind=link}

Answer

-

$8; 800

-

$6; 1.200

-

$4; 1.600

-

$2; 2.000

-

$0; 2.400

Question 31

Question

If the duopolists in this baseball market collude and successfully form a cartel, what is the price that each should charge in order to maximize profits?

Answer

-

$8

-

$7

-

$6

-

$5

-

$4

Question 32

Question

If the duopolists in this baseball market collude and successfully form a cartel, how much profit will each earn?

Answer

-

$2.700

-

$3.200

-

$3.500

-

$3.600

-

$7.200

Question 33

Question

If the duopolists are unable to collude, how much profit will each earn when the market reaches a Nash equilibrium?

Answer

-

$2.700

-

$3.200

-

$3.500

-

$3.600

-

$7.200

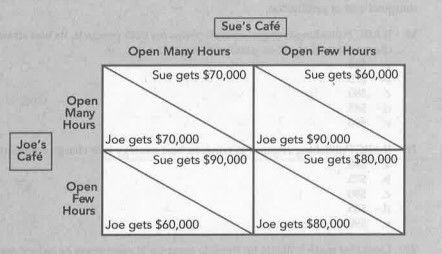

Question 34

{kind=link}

Answer

-

both to be open for many hours

-

both to be open for a few hours

-

Sue to be open for many hours while Joe is open for few hours

-

Sue to be open for few hours while Joe is open for many hours

-

There is no dominant strategy in this prisoners' dilemma game

Question 35

Question

Suppose Sue and Joe agreed to collude and jointly maximize their profits. If Sue and Joe were to be able to repeatedly play the game shown earlier and they agreed on a penalty for defecting from their agreement, what is the likely outcome of the game?

Answer

-

Both are open for many hours

-

Both are open for a few hours

-

Sue is open for many hours while Joe is open for few hours

-

Sue is open for few hours while Joe is open for many hours

Question 36

Question

Many economists argue that resale price maintenance

Answer

-

is price fixing and therefore is prohibited by law

-

Enhance the market power of the producer

-

Has a legitimate purpose of stopping discount retailers from free riding on the services provided by full-service retailers

-

Both A and B

Question 37

Question

Collusion is difficult for an oligopoly to maintain

Answer

-

Because antitrust laws make collusion illegal

-

Because in the case of oligopoly, self-interest is in conflict with cooperation

-

If additional firms enter of the oligopoly

-

For all of the above reasons

Question 38

Question

If ABC Publishing charges separate prices for both products, its best strategy is to charge prices that, when combined, total

Answer

-

$60

-

$75

-

$80

-

$85

-

$90

Question 39

Question

If ABC Publising engages in tying, its best strategy is to charge a combined price of:

Answer

-

$60

-

$75

-

$80

-

$85

-

$90

Question 40

Question

Laws that make it illegal for firms to conspire to raise prices of reduce production are known as

Answer

-

Pro-competition laws

-

Antitrust laws

-

Antimonopoly laws

-

Anticollusion laws

-

All of the above

Question 41

Question

The most important factors of production are

Answer

-

labour, land, and capital.

-

water, earth, and knowledge.

-

money, stocks, and bonds.

-

management, finance, and marketing.

Question 42

Question

If a factor exhibits diminishing marginal product, hiring additional units of the factor will

Answer

-

cause a reduction in output.

-

have no effect on output.

-

increase the marginal product of the factor.

-

generate ever smaller amounts of output.

Question 43

Question

What is the marginal product of labour as the firm moves from using three workers to using four workers?

{kind=link}

Answer

-

14

-

0

-

none of these answers

-

2

-

12

Question 44

Question

If the price of output is €4 per unit, what is the value of the marginal product of labour as the firm moves from using four workers to using five workers?

Answer

-

€60

-

€4

-

€12

-

€8

-

€56

Question 45

Question

If this profit-maximizing firm sells its output in a competitive market for €3 per unit and hires labour in a competitive market for €8/hour, then this firm should hire

Answer

-

four workers.

-

three workers.

-

two workers.

-

five workers.

-

one worker.

Question 46

Question

The value of the marginal product of labour is

Answer

-

the price of the output times the wage of labour.

-

the price of the output times the marginal product of labour.

-

none of these answers.

-

the wage of labour times the quantity of labour.

-

the wage of labour times the marginal product of labour.

Question 47

Question

For a competitive, profit-maximizing firm, the value-of-the-marginal-product curve for capital is the firm's

Answer

-

supply curve of capital.

-

demand curve for capital.

-

production function.

-

marginal cost curve.

Question 48

Question

An increase in the supply of labour

Answer

-

increases the value of the marginal product of labour and decreases the wage.

-

decreases the value of the marginal product of labour and decreases the wage.

-

decreases the value of the marginal product of labour and increases the wage.

-

increases the value of the marginal product of labour and increases the wage.

Question 49

Question

A decrease in the demand for fish

Answer

-

decreases the value of the marginal product of fishermen, reduces their wage, and reduces employment in the fishing industry.

-

increases the value of the marginal product of fishermen, increases their wage, and increases employment in the fishing industry.

-

decreases the value of the marginal product of fishermen, reduces their wage, and increases employment in the fishing industry.

-

increases the value of the marginal product of fishermen, increases their wage, and decreases employment in the fishing industry.

Question 50

Question

What will a decrease in the supply of fishermen do to the market for capital employed in the fishing industry?

Answer

-

increase the demand for fishing boats and decrease rental rates on fishing boats

-

decrease the demand for fishing boats and increase rental rates on fishing boats

-

decrease the demand for fishing boats and decrease rental rates on fishing boats

-

increase the demand for fishing boats and increase rental rates on fishing boats

Question 51

Question

An increase in the demand for apples will cause all but which of the following?

Answer

-

a decrease in the number of apple pickers employed

-

an increase in the value of the marginal product of apple pickers

-

an increase in the price of apples

-

an increase in the wage of apple pickers

Question 52

Question

A decrease in the supply of farm tractors will cause all but which of the following?

Answer

-

an increase in the rental rate for tractors

-

a decrease in the rental rate of farmland

-

an increase in the value of the marginal product of tractors

-

an increase in the wage of farm workers

Question 53

Question

If both input and output markets are competitive and firms are profit maximizing, then in equilibrium each factor of production earns

Answer

-

an amount equal to the price of output times total output.

-

the amount allocated by the political process.

-

an equal share of output.

-

the value of its marginal product.

Question 54

Question

An individual firm's demand for a factor of production

Answer

-

slopes downward because an increase in the production of output reduces the price at which the output can be sold in a competitive market, thereby reducing the value of the marginal product as more of the factor is used.

-

slopes downward due to the factor's diminishing marginal product.

-

slopes upward due to the factor's increasing marginal product.

-

is perfectly elastic (horizontal) if the factor market is perfectly competitive.

Question 55

Question

An increase in the demand for a firm's output

Answer

-

decreases the prosperity of the firm but increases the prosperity of the factors hired by the firm.

-

decreases the prosperity of both the firm and the factors hired by the firm.

-

increases the prosperity of both the firm and the factors hired by the firm.

-

increases the prosperity of the firm but decreases the prosperity of the factors hired by the firm.

Question 56

Question

A competitive, profit-maximizing firm should hire workers up to the point where

Answer

-

the wage, the rental price of capital, and the rental price of land are all equal.

-

the marginal product of labour equals zero and the production function is maximized.

-

the value of the marginal product of labour equals the wage.

-

the marginal product of labour equals the wage.

Question 57

Question

Which of the following is not true with regard to workers who have a high value of marginal product?

Answer

-

have skills that are in relatively scarce supply.

-

produce output for which there is great demand.

-

usually have little capital with which to work.

-

are usually highly paid.

Question 58

Question

An increase in the price of automobiles shifts the demand for autoworkers to the

Answer

-

left and decreases the wage.

-

right and decreases the wage.

-

right and increases the wage.

-

left and increases the wage.

Question 59

Question

When capital is owned by the firm as opposed to being directly owned by households, capital income may take any of the following forms except

Answer

-

interest.

-

dividends.

-

increases in stocks of goods.

-

retained earnings.

Question 60

Question

Suppose that a war is fought with biological weapons. The weapons destroy people but not capital. What is likely to happen to equilibrium wages and rental rates after the war when compared to their values before the war?

Answer

-

Wages rise and rental rates fall.

-

Wages rise and rental rates rise.

-

Wages fall and rental rates rise.

-

Wages fall and rental rates fall.

Want to create your own Quizzes for free with GoConqr? Learn more.