3220037

Beschreibung

Mindmap von meyer cohn, aktualisiert more than 1 year ago

|

|

Erstellt von meyer cohn

vor mehr als 9 Jahre

|

|

PPE summary

- DEF: Tangible items: 1. held for

use; & 2. expected to be

used in more than 1 period

- Recognition

- COST: 1. Probable future

economic benefits flow to

entity; 2. Measured reliably.

- COST: 1. Probable future

economic benefits flow to

entity; 2. Measured reliably.

- Measurement

- Initial Cost

- Elements & E.g

IAS16.16

- Elements & E.g

IAS16.16

- After recognition

- Cost model

- Cost less accumulated

depreciation &

impairment losses

- Cost less accumulated

depreciation &

impairment losses

- Revaluation model

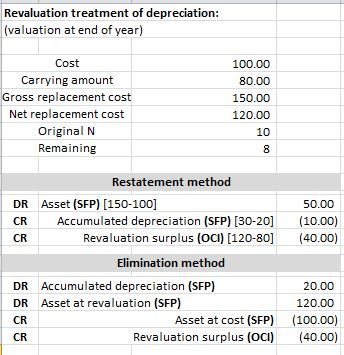

- Fair value less accumulated

depreciation & impairment

losses (Since last valuation)

- Determine FV

(IFRS 13)

- Market / Cost /

Income

- Asset is revalued from

CA to Net Replacement

Cost ON Valuation date.

- Market / Cost /

Income

- Treatment of

Accum. deprec.

- Proportionately

restated

- Eliminated

- Proportionately

restated

- Realisation

of Revalue

surplus

- Through use: Difference between Deprec. @

revalue amount and Deprec. @ Cost (ignore

revalue). DR Revalue Surpl. (SCE) CR Ret.

Earn. (SCE)

- Through use: Difference between Deprec. @

revalue amount and Deprec. @ Cost (ignore

revalue). DR Revalue Surpl. (SCE) CR Ret.

Earn. (SCE)

- Timing

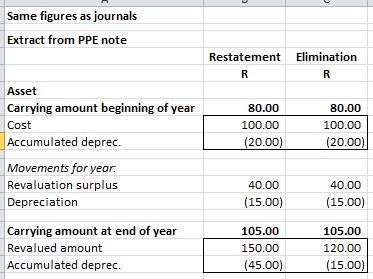

- BEGIN/yr: Deprec.

& CA at price levels

at BEGIN/yr.

- END/yr: At GRC calc NRC at

BEGIN/yr to calc. revaluation

surplus.

- BEGIN/yr: Deprec.

& CA at price levels

at BEGIN/yr.

- Fair value less accumulated

depreciation & impairment

losses (Since last valuation)

- Cost model

- Initial Cost

- Disclosure

simplistic

- Deferred tax

Medienanhänge

{kind=link}

{kind=link}

{kind=link}

Möchten Sie kostenlos Ihre eigenen Mindmaps mit GoConqr erstellen? Mehr erfahren.