9024535

Throughput Accounting

- Key Concepts

- Throughput = Sales revenue less material cost

- All costs other than materials are assumed to be fixed in the short term.

- Inventory is BAD - ideal inventory is zero

- Sales = Profit (No demand = no production)

- Throughput = Sales revenue less material cost

- Theory of

Constraints

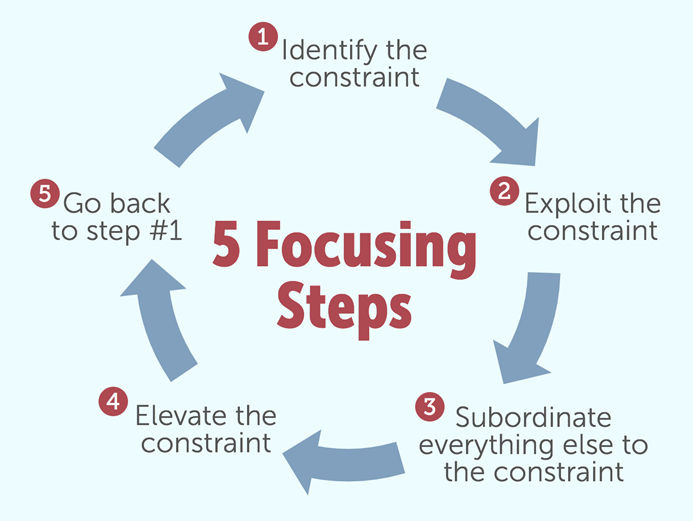

- Goldratt’s proposed five-step process for ongoing

improvement:

- Step 1 Identify the bottleneck/binding constraint.

- Step 2 Exploit. Obtain highest possible output from constraint.

- Step 3 Subordinate. Operations prior to constraint should operate as same speed as

constraint to avoid build up of WIP.

- Step 4 Elevate the constraint/ bottleneck. Take steps to improve its efficiency.

- Step 5 Return to step 1.

- Step 5 Return to step 1.

- Step 4 Elevate the constraint/ bottleneck. Take steps to improve its efficiency.

- Step 3 Subordinate. Operations prior to constraint should operate as same speed as

constraint to avoid build up of WIP.

- Step 2 Exploit. Obtain highest possible output from constraint.

- Step 1 Identify the bottleneck/binding constraint.

- Goldratt’s proposed five-step process for ongoing

improvement:

- TPAR

- Return per factory hour/Cost per factory hour

- Sales – Direct Material costs /Product’s time on the bottleneck resource

- Total Factory Cost/Total bottleneck resource time available

- Sales – Direct Material costs /Product’s time on the bottleneck resource

- Interpretation

- Viable products/divisions should have a TPAR >1

- TPAR>1 would suggest that throughput exceeds operating costs so the product should make a profit.

Priority should be given to the products generating the best ratios.

- TPAR<1 would suggest that throughput is insufficient to cover operating costs resulting in a loss.

- TPAR<1 would suggest that throughput is insufficient to cover operating costs resulting in a loss.

- TPAR>1 would suggest that throughput exceeds operating costs so the product should make a profit.

Priority should be given to the products generating the best ratios.

- Viable products/divisions should have a TPAR >1

- Improving the TPAR

- 1) Increase the sales price for each unit sold to increase the throughput per unit. 2) Reduce materials

costs per unit (change materials or suppliers) to increase the throughput per unit. 3) Reduce total

operating expenses to reduce the cost per factory hour. 4) Increase capital investment in equipment,

machines 5) Improve the productivity of the bottleneck e.g. the assembly workforce or the bottleneck

machine, thus reducing the time required to make each unit. Throughput per factory hour would

increase and consequently the TPAR would increase.

- 1) Increase the sales price for each unit sold to increase the throughput per unit. 2) Reduce materials

costs per unit (change materials or suppliers) to increase the throughput per unit. 3) Reduce total

operating expenses to reduce the cost per factory hour. 4) Increase capital investment in equipment,

machines 5) Improve the productivity of the bottleneck e.g. the assembly workforce or the bottleneck

machine, thus reducing the time required to make each unit. Throughput per factory hour would

increase and consequently the TPAR would increase.

- Criticisms of TPAR

- It concentrates on the short term when a business has a fixed supply of resources (i.e. a bottleneck)

and operating expenses are largely fixed. However, most businesses can’t produce products based

on the short term only.

- It is more difficult to apply TA concepts in the long term, when all costs are variable and vary with the

volume of production and sales. The business should consider this long term view before rejecting

products with a TPAR<1

- It concentrates on the short term when a business has a fixed supply of resources (i.e. a bottleneck)

and operating expenses are largely fixed. However, most businesses can’t produce products based

on the short term only.

- Return per factory hour/Cost per factory hour

- Multi-Product Decision Making

- Step 1: Identify the bottleneck constraint

- Step 2: Calculate the throughput per unit for each product

- Step 3: Calculate the throughput per unit of the bottleneck resource for each product

- Step 4: Rank the products in order of the throughput per unit of bottleneck resource

- Step 5: Allocate resources using this ranking and answer the question e.g. calculate

the total throughput/profit of this optimum production level

- Step 5: Allocate resources using this ranking and answer the question e.g. calculate

the total throughput/profit of this optimum production level

- Step 4: Rank the products in order of the throughput per unit of bottleneck resource

- Step 3: Calculate the throughput per unit of the bottleneck resource for each product

- Step 2: Calculate the throughput per unit for each product

- Step 1: Identify the bottleneck constraint

- Bottleneck resource or binding constraint = an activity which has a lower capacity than preceding or

subsequent activity thereby limiting throughput

- Optimised Production Technique

- OPT is based on the principle that profits are increased by increasing the throughput of the organisation. The OPT

approach identifies what prevents throughput being higher by distinguishing between bottleneck and

non-bottleneck resources. The OPT philosophy therefore advocates that non-bottleneck resources should not be

operating at 100% as this will result in inventories increasing. Thus idle time in a non-bottleneck resource is not

considered to be detrimental to the company’s operations as increased inventory would result without a

corresponding increase in throughput for sale.

- OPT is based on the principle that profits are increased by increasing the throughput of the organisation. The OPT

approach identifies what prevents throughput being higher by distinguishing between bottleneck and

non-bottleneck resources. The OPT philosophy therefore advocates that non-bottleneck resources should not be

operating at 100% as this will result in inventories increasing. Thus idle time in a non-bottleneck resource is not

considered to be detrimental to the company’s operations as increased inventory would result without a

corresponding increase in throughput for sale.

Medienanhänge

{kind=link}

{kind=link}

Möchten Sie kostenlos Ihre eigenen Mindmaps mit GoConqr erstellen? Mehr erfahren.