Seite 1

SUPPLY

Market equilibriumMarket disequilibriumForms of government intervention Price Ceiling Price Floor

Quantity supplied of a good Amount which producers are able and willing to offer for sale in a given time period, at a particular price, ceteris paribus. SupplyEntire range of quantities that producers are able and willing to offer for sale at different prices, in a given period of time, ceteris paribus.

{kind=link}

Quantity supplied At a particular point on the curve. Supply Refers to all the points on the supply curve, the entire supply curve.

Law of supply A direct relationship exists between price and quantity supplied of a good. Price increases, quantity supplied of a good increases Price decreases, quantity supplied of a good decreases. Why direct relationshipProducers are more willing to sell greater amounts at higher price, because the good have become relatively more profitable to produce.Higher price will help producers cover the higher opportunity cost.

Price changes Movements along the supply curve. Quantity supplied changes.

Determinants of supply

Determinants Factors other than the price which affects how much sellers are able and willing to sell a good Constant Shifts the entire curve (Quantity supplied changes at each and every price level)

Determinants Factor/resource price Technology Price of related goods Expectations of producers Number of sellers in the market

Resource price If higher costs or production were incurred. Less willing and able to sell at all price levels. (Shift left) If higher costs or production, higher price may be charged at every output level. (Shift left) Technology Fewer resources are needed for production of a good Leads to lower cost of production, at every price level suppliers are willing and able to sell more Supply increases, (Shift right) Or sellers are more able and willing to sell at lower price at every quantity (Shift right)

Price of related goods Substitutes: Require same resource to produce E.g. rubber bands, rubber erasers Complements: Jointly produced with same resources E.g. Beef and leather Substitutes (Price increase of one rubber quantity supplied of rubber increases, not enough resources for rubber bands. Left shift) Complements (Price increase, Quantity supplied of beef increases, increasing number of cows slaughtered, increase in supply of leather. Right shift)

Expectations of future profits If sellers expect price to fall they will sell more now. (Shift right)

Number of sellers If increase in number of sellers, supply increases (Shift right)

Changes in quantity supplied Price Movement along the curve

Changes in supply Non-price determinants (Resource/factor price, Technology, Price of related goods, Expectations of future profits, Number of sellers) Shift of supply curve

Supply (Factors of production) Comes from households and are sold to business firms, to produce goods and services Positively shaped

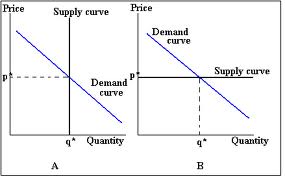

Exceptional supply curve Vertical supply: Regardless of any price change, quantity supplied will not change. Horizontal: At the existing price, the quantity supplied is infinite.

{kind=link}

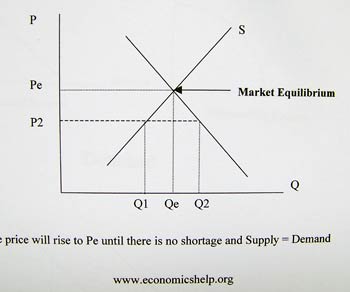

Market Equilibrium

What is equilibrium A state in which opposing forces balance each other. No inherent tendency for change. Market demand and market supply balance each other. No tendency for change. Wishes of buyers and sellers match. Quantity demanded equals quantity supplied.

{kind=link}

Not in equilibriumShortage (Qd>Qs) / Surplus (Qs>Qd) Surplus (Qs>Qd) Occurs when quantity supplied exceeds quantity demanded. Downward pressure on price as sellers are forced to reduce price. As price decreases, buyers buy more sellers sell less, until equilibrium is attained. Changes in Eqm Price & Qty Once equilibrium is attained, there is no tendency to change, unless demand, supply or both market forces to change. Demand and supply change if there is a change in non-price determinants.

SA

Shortage (Qd>Qs) Occurs when quantity demanded exceeds quantity supplied. Upward pressure on price as buyers increase price As price increases, sellers sell more and buyers buy less, until equilibrium is attained.

If demand and supply increase simultaneously, equilibrium qty will definitely increase. Equilibrium price will increase or decrease depends on. How much demand shifts relative to supply?

Market disequilibrium - Govt intervention Govt step in to restrict the free operation of market. Price ceiling or price floor.Price floor A legally established minimum price above the market equilibrium. Sales below price floor not permitted. Imposed during a period of falling prices. To ensure producers a higher and stable income Ensure std of living Price floor create surpluses govt intervention needed to prevent downward pressure on price. Buy the surplus. Distributed to poor, stored up wasteful if quality deteriorates over time. Consumers pay a higher price than market eqm. Consumers pay tax to cover govt support Amount bought and sold with PF imposed is less than market eqm.

Price ceiling A legally established maximum price below the market equilibrium. Sales above price ceiling not permitted Imposed during a period of rising prices. Prevents consumers from being overcharged Shortage: Caused by the price ceiling forces consumers to more time searching for an alternative. Lead to black market transactions. Rent control leads to deteriorating quality of housing (Little incentive for landlords to maintain) Amount bought and sold with a PC imposed is less than that at market eqm.

Supply

Determinants of supply

Market Equilibrium

Möchten Sie kostenlos Ihre eigenen Notizen mit GoConqr erstellen? Mehr erfahren.