2093301

| Frage | Antworten |

| In a competitive market, the firms are called "price-takers". Explain what that means. | It means that any one firm or groups of firms cannot significantly alter the terms of exchange or transaction terms - aka the price. Another way of explaining this would be that there are too many sellers for any effective price conspiracy to take place. |

| List the function of prices (3) | Disciplinarians, signals, and rationers |

| Explain the function of prices as disciplinarians | As disciplinarians, prices "regulate" the competitive behavior of producers. Consumers, through prices, tell producers that they need to provide a better product or a lower price on the current product. If the consumers' demands aren't met, they "vote" with their dollars by buying from competitive suppliers. |

| Explain the function of prices as signals. | As signals, prices reflect consumer choices and preferences. Their consumer expenditures give off "signals" to the producers. Like a traffic light, if the producers get a green light, consumers are saying the price is right according to their incomes and preferences. A yellow light suggests that consumers are considering substitutes - this may be because of the price relative to other goods and the consumer's income. A red light directs producers to design and provide different products and services. The reduced demand is no longer sufficient to pay for producers' costs, including a profit. |

| Explain the function of prices as rationers | As rationers, prices put pressure on consumers and suppliers to economize on scare resources. Relatively scare resources carry high price tags. Therefore the consumers expect producers to use relatively few scarce (high-price) resources, also called "economizing" those resources. Conversely, the relatively abundant resources would carry lower price tags and used more. |

| Two types of prices | Absolute price - price of a good as stated; Relative Price - expressed in terms of a ratio between any two prices or the ratio of a particular good and weighted average of all other goods (aog) available on the market. PR = (Px / Py) or (Px / Paog). |

| Equilibrium occurs when (3) | 1. QD = QS 2. No tendency for change; the demand function and the supply function stay constant 3. No surplus or shortage; the equilibrium price "clears" the markets. |

| What is the difference between "amount demanded" and "change in amounts demanded" | Amount demanded - the amounts consumers are willing to buy of a particular good or service at varying prices of that good/service. Change in Amounts Demanded - change along a demand curve as a result of only a change in the price of that good, certris paribus. Occurs when the determinants change. |

| 5 determinants of demand | 1. Number of consumers 2. Preferences of consumers 3. Prices of related goods - substitute and complementary 4. Consumers' incomes 5. Price expectations |

| 6 determinants of supply | 1. Number of sellers 2. Costs of resources or production 3. Prices of substitute goods (goods that are also produced or could be using similar resources) 4. Price expectations 5. Technology 6. Taxes/subsidies |

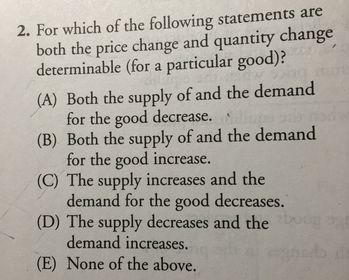

| What happens to the equilibrium price and quantity with an increase in demand and a constant supply? | Equilibrium price and quantity increases. |

| Giffen Good | Good for which there is an upward-sloping demand curve (theoretical). Aka people consume more as price rises. A Giffen good is typically an inferior product that does not have easily available substitutes, as a result of which the income effect dominates the substitution effect. |

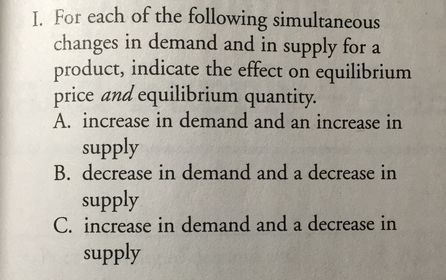

| What happens when changes in demand and supply are simultaneous? | |

| E | |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Möchten Sie mit GoConqr kostenlos Ihre eigenen Karteikarten erstellen? Mehr erfahren.