9052654

Beschreibung

Karteikarten von Josie Robinson, aktualisiert more than 1 year ago

|

|

Erstellt von Josie Robinson

vor mehr als 7 Jahre

|

|

| Frage | Antworten |

| CHAPTER 1 What is a business case? | A justification of a procurement on the basis of how effectively and efficiently it meets identified business needs |

| 'Inputs' examples | materials, components, energy, machinery, equipment, labour, supplies, services, skills |

| Strategic / commercial objectives | 1. achieve value for money for shareholders and the public while upholding service level agreements 2. achieve and maintain a competitive advantage in the market 3. achieve differentiation and innovation (CSR) 4. attract and retain high quality stakeholders |

| Four stages in the way procurement has developed | 1. passive 2. independent 3. supportive 4. integrative |

| the procurement cycle 1. identify the need 2. define the need 3. develop contract terms 4. source the market 5. appraise the market | 6. invite RFQ or RFT responses 7. analyse responses 8. negotiate best value 9. award the contract 10. contract and supplier management |

| Three types of purchase | 1. straight re-buy: items already sourced from a supplier 2. modified re-buy: requirements change with existing supplier 3. new buy: requirement has not previously been specified or sourced |

| straight re-buy the buyer may already have a preferred supplier | it is not always necessary to: establish specifications survey or source the market invite quotations and tenders |

| straight re-buy (or inventory replenishment) involves... | 1. to optimise inventory replenishment methods 2. review existing specifications and arrangements 3. re-open existing long-term contracts to competition |

| modified re-buy requirements - some of the requirements have changed | 1. need to re-specify the need or re-negotiate the contract with same supplier 2. business case justification required for high-risk procurement modifications 3. modification of the requirement may present an opportunity to revisit specfications or the contract |

| modified re-buy involves.. | 1. reviewing existing specifications and arrangements 2. challenge modified specifications 3. re-open existing contracts to competition 4. justify specification or contract modification 5. re-negotiate contract terms |

| New purchase a good or service which has not been specified or purchased before | 1. procurement activity is likely to conform to the full, systematic procurement process 2. an in depth business case justification 3. key opportunity to identify new additional benefits |

| purchasing research | 1. demand analysis 2. vendor analysis 3. supply market analysis |

| value engineering eliminates waste | value analysis applied to design, development and specification stage of procurement development |

| early buyer involvement (EBI) influences whole-of-life impact | ensures commercial and supply market considerations are taken into account |

| early supplier involvement (ESI) | ensures solution takes into account supply market expertise, technology and innovation |

| Capital procurement | Procurement of assets with long usage life and high acquisition cost |

| production materials | raw materials, components and assemblies. often impact operational efficiencies |

| maintenance repair and operating (MRO) | all goods and services, other than capital equipment, necessary to transform raw materials and components into end products |

| commodities | raw materials such as textiles, food and beverage crops, and minerals |

| goods for re-sale | purchases by a retailer or wholesaler for sale onwards to customers / consumers |

| informal business case structure | 1. intro / background 2. options 3. business benefits 4. costs and risk 5. recommendation 6. KPIs |

| comprehensive, formal business case structure (for high-risk, high-value procurements) | 1. exec summary 2. reference 3. context 4. value proposition 5. scope 6. deliverables 7.impacts 8. work planning 9. resource requirements 10. risk management and contingency 11. commitments |

| value | the perceived 'worth' of a product or service |

| competitive advantage | the ability to deliver value to customers more efficiently or effectively than one's competitors |

| costs | 1. financial costs 2. non-financial costs 3. opportunity costs |

| risks (e.g. outsourcing, single sourcing, international sourcing) | necessary to balance risks and associated costs against the benefits of the proposal risks must be assessed for probability of occurrence and the impact of the risk if it occurs - contingency planning |

| cost/benefit analysis | putting a monetary value to the benefits of a course of action and deducting the costs associated with it. often difficult to calculate intangible benefits |

| advantages of outright purchase vs advantages of leasing | disadvantages of outright purchase vs disadvantages of leasing |

| strategic alignment | 1. suitability 2. feasibility 3. acceptability 4. environmental sustainability 5. social sustainabilty |

| environmental procurement | organisations meet their needs for goods, services, works, and utilities in a way that achieves value for money on a whole life basis while generating benefits for society, the economy, and the environment |

| triple bottom line | 1. economic sustainability (profit) 2. environmental sustainability 3. social sustainability |

| CHAPTER 2 price vs cost | price: what a seller charges to the buyer cost: what the buying organisation pays to acquire the goods or services purchased - acquisition, installation, maintenance, disposal etc |

| price and cost research | 1. primary data - surveys, interviews, questionnaires or observations 2. secondary data - data already gathered for other purposes (pg 25) |

| external factors to supplier pricing decisions | 1. prices charged by competitors 2. extent of competition 3. market conditions - levels of demand and supply 4. environmental factors affecting the cost of raw materials 5. customer perceptions of value |

| internal factors to supplier pricing decisions | 1. cost of production and sales 2. risk management 3. shareholder expectations and managerial objectives 4.strategic objectives of the organisation 5. customer vs supplier relationship |

| cost-based pricing | 1. full-cost pricing 2. marginal pricing 3. rate of return pricing 4. contribution pricing |

| market-driven pricing | 1. price volume (breakeven) 2. market share pricing (low introductory prices) 3. market skimming (high introductory prices) 4. promotional pricing |

| price analysis | determines whether the price offered is fair and appropriate for the goods / services / works. |

| cost analysis | specialised technique - looks specifically at how the quoted price relates to supplier's cost of production. often used to support price negotiations where the supplier justifies its price by the need to cover costs |

| understanding costs - components of the cost base | 1. raw materials 2. labour 3. overheads |

| overheads | expenditure which cannot be directly identified with the output of any particular production item. e.g. electricity, maintenance, office expenses, marketing and advertising, logistics and transport |

| ***profit is not a cost - although along with cost, it is a component of price*** | > direct vs indirect costs < |

|

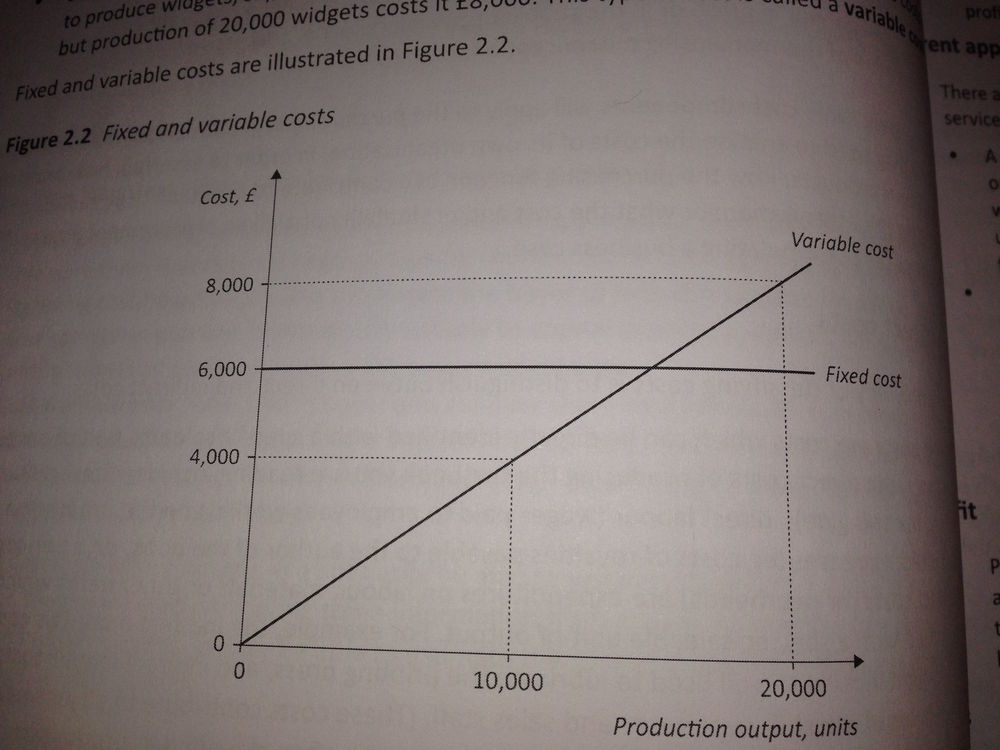

what is cost behaviour?

fixed cost vs variable cost

Image:

Img 4091 (image/jpeg)

|

the way in which the cost of output are affected by fluctuations in the level of activity fixed cost: staff salary or building rent (costs incurred by the business whether they produce anything or not) variable cost: dependant on production and sales |

| calculating costs 1. marginal costing 2. absorption costing | marginal costing uses only variable costs to derive a unit cost absorption costing attempts to calculate the total cost of producing products |

| profit? | the difference between the selling price of the product and the cost of producing the product |

| contribution analysis | the difference between sale revenue and the variable cost of making sales |

| total cost of ownership | 1. various transaction costs (taxes, foreign exchange rate) 2. finance costs 3. acquisition costs 4. operating costs 5. storage costs 6. end of life costs |

| Ways to calculate whole life costs | 1. Discounted cashflow (DCR) 2. payback / recovery period (pg 35) 3. accounting rate of return (ARR) / return of investment |

| benefits of calculating whole of life costs | 1. enables the fair comparison of competing options 2. enabling realistic budgeting over the life of the asset 3. highlights risks early 4. promotes functional communication 5. supporting the optimisation of value for money |

| limitations to whole of life costing (WLC) | 1. not exact, future cost estimates are subjective 2. many costs are incurred through the life of the product or asset 3. a wide range of factors may affect costs over the lifecycle of the product / service 4. systematic WLC exercise can be time-consuming, labour intensive and costly |

| qualitative methods used to estimate cost | 1. supply market research 2. expert opinion |

| budget | a plan quantified in money terms, prepared and approved prior to a defined period of time |

| procurement budget info (page 38) | cash budgets (page 39) |

| primary data sources | 1. communication with suppliers 2. the buyer's database of market data 3. marketing communications of suppliers 4. online market exchanges 5. trade fairs, exhibitions, conferences 6. informal networking |

| secondary data sources | 1. financial trade or industry press 2. published / online market analysis 3. published statistical surveys 4. price listing and comparison websites |

| a cash budget should include... (objective: to anticipate cash shortages or surpluses and allow time to make plans for dealing with them) | 1. the cash balance at the start of the period 2. receipts 3. payments 4. the anticipated cash balance at the end of the period |

| CHAPTER 3 Benefits of budgeting | 1. express organisational objectives as operational targets 2. motivates people to attain performance and cost targets 3. motivates managers to identify risks and problems 4. to pre-authorise estimated levels of expenditure 5. to control procurement activities and costs |

| limitations of budgeting | 1. cumbersome to establish and maintain 2. political aspects 3. cost estimation - often inaccurate and unreliable 4. budget data may become quickly outdated 5.often focus on short term performance rather than long term value |

| two types of budget | 1. incremental budget 2. zero-based budget |

| incremental budget | begin by looking at actual figures from the previous period, then adjust in line with known changes to occur during budget for the period |

| zero-based budget | ignores previous periods and starts completely from scratch. |

| two budgeting techniques... 1. forecast - at intervals during the year the budget is revisited and updated inline with new information | 2. rolling budget - maintained and added to at the end of the budgeting period, linking with the next |

| fixed budget | based on a particular estimate of activity levels - e.g sales volume of 2000 units sold a year, a problem arises when this estimation is incorrect |

| flexible budgets | recognise different cost behaviour patterns and are designed to change as the volume of output changes |

| variance analysis | based on a comparison of what something should have cost vs actually cost |

| examples of explanations for variances | 1. the skill of the buyers negotiation team 2. fluctuations in commodity prices 3. fluctuations in exchange rates 4. incurring late payments or other price penalties |

| CHAPTER 4 what is a specification? | a systematic statement of the requirement to be satisfied in the supply of a product or service |

| a specifications must: | 1. define the requirement 2. communicate the requirement 3. provide a means of evaluating the quality or conformance |

| tolerance a supplier can not always meet the exact requirement of a specification every time | 'leeway' - how much variation from the specification is acceptable |

| use the 'five rights of procurement' when defining a specification | right time right place right quantity right quality right price |

| zero defects implications | 1. specifications will have low tolerance 2. supplier pre-qual, selection and appraisal - suppliers must be capable, reliable and dependable consistently 3. quality control despite being fully audited 4. costs of assuring quality are significant |

| why don't all specifications have zero tolerance? | 1. work may be difficult to specify accurately or prescriptively 2. tight tolerances are more costly to achieve (e.g. advanced machinery) |

| specifications give purpose for what a purchased item is to be used for | example: specify a 5L bucket, but get delivered a 3L bucket = not fit for purpose. The 5L also needs to be durable enough to hold chemicals |

| advantages of specifications | 1. encourages you to consider alternative ways of achieving goals 2. provide useful criteria for measuring quality 3. provide evidence in the event of the dispute 4. allow for ease and speed of use, understanding and evaluation 5. enables potential bidders to 'self-select', avoiding wasted time on further analysis 6. enables and encourages supplier flexibility and innovation |

| disadvantages of specifications | 1. often expensive an time consuming process 2. specifications can become too firmly embedded - they need to be regularly reviewed 3. can create temptation to over-specify, adding cost and increasing stock variation 4. there may be misunderstanding over requirements and expectations with both suppliers and other stakeholders 5. quality defects |

| types of specification | 1. conformance 2. performance |

| evaluating conformance specifications (generally becoming less common) | 1. it can be difficult, time consuming and costly to draft a comprehensive description of exactly what you want 2. the buyer bears risk of the design not performing to expectation 3. conformance specifications may restrict the potential supplier base - capabilities 4. the prescriptive nature may restrict innovation |

| circumstances where conformance specifications are appropriate... | 1. technical or design specification e.g. engineering drawing 2. composition specification (the chemical or physical make-up of properties required |

| evaluating the use of performance specifications | 1. easier and cheaper to draft 2. efficacy of the specification does not depend on the technical knowledge of the buyer 3. suppliers can use their full expertise and innovative capacity 4. potential supplier base becomes wider than with a conformance specification 5. greater share of specification risk is borne by the supplier |

| circumstances where performance specifications are appropriate... | 1. suppliers have greater relevant technical and manufacturing expertise than the buyer 2. the buyer is not in a position of specifying yesterdays technologies 3. there are clear, objective criteria for evaluating alternative solutions 4.the buyer has sufficient time and expertise to assess functionality and outcomes |

| specification by chemical or physical properties (conformance specification) | composition specifications specify different types of product materials (plastic) 1. physical properties - strength, flexibility, durability are important for safety and performance 2. certain materials are restricted by law, regulation and codes of practice for health, safety and environmental reasons |

| Four other types of conformance specification: 1. specification by brand 2. specification by sample | 3. specification by market guide 4. specification by standards (pages 64 - 67) |

| output based specification (performance specification) | specifies the output of a system or process, e.g.: the deliverables of a project, the outputs of a process (commonly used in IT projects) |

| specifying services services are.... | 1. intangible 2. variable 3. inseparable 4. perishable 5. performed in different locations |

| outcome based specification (performance specification) | the buyer specifies outcomes to be met by the provider. the provider / supplier has the responsibility of determining the activities that will be performed (example: project17!) |

| sustainable specifications - triple bottom line | 1. economice (profit) 2. environment (planet) social (people) |

| CHAPTER 5 an effective specification is... | 1. clear 2. concise 3. comprehensive 4. compliant 5. up-to-date 6.value-analysed |

| procurement professionals provide: | 1. supply market awareness 2. supplier contacts 3. awareness of commercial aspects 4. awareness of legal aspects 5. purchasing disciplines (value analysis, cost reduction) |

| Four possible approaches to organising the specification process | 1. Early buyer involvement 2.formal committee approach 3. informal approach 4. purchasing coordinator approach |

| the buyers role in specification | 1. understanding the needs of users 2. liaising with users 3. minimising tolerances 4. understanding the legal implications of specification |

| early buyer involvement (EBI) | where procurement specialist are involved in defining the specifications |

| information required for specification development (page 80) | 1. technical requirements 2. availability of commercial products or services 3. schedules and lead times (timeline) 4. cots and budgetary constraints 5. supplier process 6. company policy 7. legislation |

| Definition of 'standard' | A published specification which establishes a common linkage, and contains a technical specification or other precise criteria, and is designed to be used consistently as a rule, guideline, or a definition |

| two methods of minimising stock proliferation | 1. standardisation - involves agreeing and adopting generic specifications or descriptions of the items required 2. variety reduction - is a systematic reduction in the range of items used, stocked, bought or made |

| proactive approach | uses the smallest range of inputs to produce the widest range of outputs |

| reactive or remedial approach | undertaken periodically by a specialist team comprising relevant stakeholders |

| benefits of standardisation | 1. specification: generic vs bespoke 2. purchasing: enables consolidation of requirements & takes advantage or bulk discounts & reduced handling costs 3. transport: efficient planning 4. inventory: reduces risk of deterioration 5. quality management: easier to inspect and measure quality & conformance |

| CSR specific specifications best to incorporate sustainability criteria is at the need definition, specification and pre-qual stages, then again through negotiations and post-contract | social ethical environmental (page 87) |

| waste hierarchy | reduce re-use recycle rethink |

| Information assurance - corporate governance - contingency - strategic development and management | the practice related of managing risks related to the use, processing, storage, and transmission of information and data - related to information security |

| information assurance involves these steps: | 1. systematic risk assessment 2. risk management planning 3. agreement, implementation, testing and evaluation |

| CHAPTER 6 what is supplier performance measurement | the assessment and comparison of a suppliers current performance against: 1. defined performance criteria 2. previous performance 3. he performance of other comparable organisations |

| the purpose of performance measures | they define business needs in terms of measurable outputs, outcomes, and behaviours which indicate the required level of performance to meet needs |

| supplier performance appraisal can be used to... | 1. identify the highest quality and best performing suppliers 2. suggest how relationships with suppliers can be enhanced to improve their performance 3. ensure suppliers live up to expectations agreed in their contracts 4. provide an incentive for suppliers to maintain / continuously improve performance levels 5. improve supplier performance by identifying problems / areas of development |

| what is a KPI | KPIs are clear qualitative or quantitative which define desired performance / critical areas of success against which progress and performance can be measured |

| quantitative KPIs focus on efficiency suitable for purchase of products | are 'hard' statistical / numerical / facts based. may be measured in terms of cost, quantity of outputs, or other statistics / ratios |

| qualitative KPIs focus on effectiveness suitable for purchase of services | are 'soft' and subjective indicators / attributes that cannot be readily quantified and drawn from less structural data (such as customer surveys) |

| advantages of using KPIs | 1. increased and improved communication on performance issues 2. motivation to achieve or better specified performance goals 3. supports collaboration between buyer and supplier 4. provides the ability to directly compare year on year performance 5. can focus on key result areas 6. clearly defines shared goals, facilitating teamwork 7. reduces conflict and goal confusion |

| disadvantages of KPIs | 1. some may try to cut-corners in quality to meet targets 2. teams may prioritise their own targets at the expense of collaborative / cross-functional targets |

| process of developing KPIs | 1. identify critical success factors 2. identify measures of success / improvement for each factor 3. develop and agree KPIs with key stakeholders - critical to align with business needs and purchasing objectives |

| definition of benchmarking | measuring your performance against 'the best' companies, and determine how these companies achieve their performance levels and using this information as a basis for your own company's goals, strategies and implementation - realistic and challenging |

| four types of benchmarking | 1. internal 2. competitor 3. functional 4. generic |

| the benchmarking process (cons = can be costly and reqires effective communication internally) | 1. conduct market and organisational analysis to determine priorities 2. identify suitable organisations to compare to 3. research and assess comparators performance 4. analyse research feedback to identify performance gaps and best practice 5. set targets for improvement and development of gaps |

| focus of contractual performance in this textbook | 1. quality 2. time 3. total cost of ownership 4. resources 5. delivery 6. service performance 7. compliance with CSR and other ethical standards 8. stakeholder satisfaction levels |

| the eight dimensions of product quality | 1. performance 2. features 3. reliability 4. durability 5. conformance 6. serviceability 7. aesthetics 8. perceived qulity |

| service level agreement | are formal statements of purpose requirements, specifying the nature and level of service to be provided by a service supplier |

| the purpose of an SLA | is to define the customers service level needs and secure the commitment of the supplier to meeting those needs - performance, conformance and compliance |

| benefits of SLAs (communication, relationship management, conflict management, performance monitoring, review and evaluation) | 1. clear identification of customers and providers services 2. focuses the attention on what services actually involve and achieve 3.identify real service requirements of the customer - whats adding / not adding value 4. better customer awareness of services 5. improved customer awareness of service level costs 6. supports ongoing / periodic reviews 7. supports problem solving and planning 8. improves relationship between supplier and buyer |

| limitations of SLAs | 1. lack of commitment by providers or customers 2. inadequate support structures 3. may overload staff with extra work 4. overly detailed SLAs become a burden to monitor 5. insufficient detail or specific SLAs allow problems to 'slip through' |

| contents of SLAs should include... (print page 107) | 1. what services are included 2. standards or levels of services expected (response time, speed, quality etc) 3. other expectations of the supplier (environmental and employment) 4. the allocation of responsibility for activities, risks and costs 5. how services and service levels will be monitored and reviewed 6. how complaints and disputes will be managed 7. when and how the agreement will be reviewed and revised |

| what is the process of developing and implementing SLAs | 1. information gathering 2. expectations are clarified 3. process negotiation 4. SLA development 5. securing buy-in 6. establishing monitoring and reporting mechanisms, allocated responsibilities 7. implementation 8. monitoring and reporting |

| CHAPTER 7 What is a contract? | An agreement between two (or more) parties which is intended to be enforceable by the law |

| The information found in a contract includes... | 1. who / which parties are involved and agreed 2. conditions and contingencies which may alter the agreement 3. the rights of each party if the other fails to do what has been agreed 4. who is responsible or 'liable in the event of problems 5. how disputes will be resolved |

| Express terms e.g. specify price, delivery dates, sharing of insurance costs | explicitly inserted into a contract by the parties to it, whether negotiating terms specifically for the particular contract; by applying standard terms of business, or by utilising a model form contract which has been developed to represent standard terms |

| Implied terms | are automatically assumed to be part of a contract |

| contract conditions | vital terms of the contract - failure to perform is essentially a 'deal breaker' |

| warrenties | are non-vital terms of the contract, the breach of which do not cause the contract to collapse |

| general contract structure | 1. the agreement 2. definitions 3. commercial provisions 4. secondary commercial provisions 5. standard clauses |

| Model form contracts - who are they published by? | Are published by a third party |

| advantages of using standard and model form contracts | 1. helps reduce time and costs of contract development 2. avoids repetition of work, but can be adapted to suit particular circumstances 3. industry model forms are widely accepted, reducing negotiation time and costs 4. designed to be fair to both parties |

| disadvantages of using standard and model form contracts | 1. terms may not be as advantageous to a powerful buyer as if contract was negotiated 2. terms may not include special clauses or requirements or variations to be made 3. legal advice is still required if significant amendments or variations are made 4. costs of training buyers to use model forms |

| Contract clause : time and performance | dates of shipment, transfer of delivery are example of conditions of a contract. If these are specifically expressed, the delay in performance may not be paid out by the buyer |

| Contract clause : passing of title / property | to transfer the ownership of goods (not possession!). only a person who owns goods is entitled to sell them allocation of risk for the owner / buyer |

| Contract clause : liquidated damages | a liquidated damages clause is used to guarantee the buyer damages against loses arising from a suppliers late or unsatisfactory completion of a contract |

| Contrat clause : penalty clause | penalty clauses are not enforceable by law, and are void in the event of breach |

| Model clause examples | 1. NEC - New Engineering Contract 2. FIDIC - The International Federation of Consulting Engineers 3. IMechE - The Institution of Mechanical Engineers |

| Contract clause : Force majeure | The purpose is to release parties from liability in circumstances where their failure to perform a contract results from circumstances which were unforeseeable, for which they were not responsible, and which they could not have avoided. E.g. natural disasters, war and other terrorist activity, death |

| Contract clause : guarantees | Designed to protect the buyer. The supplier will guarantee to make good any defects in the items supplied |

| Contract clause : exclusion | can totally exclude one party from liability, restrict or limit liability, or seek to offer some form of guarantee. the clause must: 1) be incorporated into the contract and 2) be constructed in a clear and concise way |

| Contract clause : Indemnities | Designed to secure an undertaking from the other party that it will accept liability for any loss arising from events in performance of the contract, and will make good the loss to the injured party/parties. |

| Contract clause : insurances | A buyer will wish to confirm the supplier has the ability to pay compensation in the event of any indemnities or legal claims arising against it. Types of insurances: 1) employer liability insurance 2) public liability insurance 3) professional indemnity insurance 4) product liability insurance |

| Contract clause : subcontracting | when the original supplier contracts out the work to a third party - the original supplier will remain liable for any failures of the third party |

| Ethics / CSR | A set of moral principles or values about what constitutes 'right' and 'wrong' behaviour given in society, market or organisation |

| CHAPTER 8 Two types of pricing arrangements | 1. fixed - agreed in advance of work 2. flexible - cost plus fixed percentage |

| Pricing schedule firm price agreements | contracts that are negotiated with fixed payment schedules, payment based milestones, or payment based on fixed fees for a service |

| firm price arrangements are appropriate when... | 1. a comprehensive and accurate specification in available 2. fair prices can be estimated and established 3. when there is relatively little risk of cost variation 4. electronic purchase to pay systems are utilised |

| firm price arrangements are advantageous to the buyer because: | 1. the supplier bears all the risk of cost fluctuations 2. cashflow management is reliable because payments are pre-planned 3. motivation and an incentive to complete work |

| Pricing schedule lump sum contracts | a fixed sum for completing work by a given date. has an element of flexibility, e.g. price fluctuations arising from contingency factors |

| reasons for cost/price variations | 1. underestimation of costs at forecasting stage 2. price inflation, escalating materials cost 3. wage inflation, escalating labour costs 4. commodity and energy price fluctuations 5. exchange rate fluctuations 6. unforeseen contingencies |

| the use of indexation and price adjustment formulae | the calculation of average changes in price or cost can: 1. estimate the current average prices or costs of a product 2. eliminate effects of inflation or deflation when analysing price and cost trends 3. allow for currency fluctuations when estimating or negotiating future costs |

| fixed price incentive (or gainshare) contracts provides adjustment of the final price to include various supplier incentives | options for incentivised contracts: 1. staged payments 2. specified bonus payments (meet KPIs) 3. price penalties for performance failure 4. when the product or services year on year through the contract |

| cost-based pricing arrangements | based on guaranteeing that the supplier covers its costs incurred in performing the contract, in addition to earning an agreed profit percentage. |

| cost-plus pricing (cost-based pricing arrangement) | the buyer agrees to reimburse the supplier for all allowable and reasonable costs incurred in performing the contract, plus a fixed fee or percentage representing the suppliers profit |

| types of cost-plus pricing | 1. cost plus fixed fee 2. cost plus incentive fee 3. cost plus award fee 4. cost without fee 5. cost sharing 6. time and materials (per labour hour) |

| disadvantages of cost-plus pricing arrangements for the buyer | 1. financial risk - total price commitment is not known in advance and bears all risk of cost variations 2. supplier motivation 3. administration and contract management costs |

| target costing each member of the supply chain must work closely with others to identify opportunities for cost reductions, driving costs downwards | the supplier estimates the maximum selling price that the market will be willing to pay. the cost is work backwards to calculate the production cost and ensure reasonable profit (opposite of cost-plus pricing) |

| target cost with maximum price | the contract stipulates a target price (based on target costs and profit margin) and a maximum ceiling price for the contract. Any excess costs over and above the maximum price are charged to the supplier. Any savings are shared on a agreed percentage basis between supplier and buyer. |

| target cost with maximum price are suitable when... | the target cost can be determined with a reasonable degree of accuracy but exact total costs cannot be accurately forecast at the time of the contract and the buyer has the power to negotiate a position where it does not bear extra risks and cost |

| target cost without maximum price | there is no ceiling price to protect the buyer; a target price is determined on the basis of target cost. Any excess costs over and above the target price are shared between the supplier and buyer. Any savings are also shared on a agreed percentage |

| target cost without maximum price are suitable when... | for long-term contracts, especially volatile supply markets (over the life of the contract) - creates an incentive for cost management as suppliers and buyers will anticipate to be reimbursed for extra costs |

| payment methods | 1. payment in advance - often used in high-risk supply contexts 2. payment on delivery 3. open account or credit - agreed payment period after delivery (usually 30 to 60 days) |

| credit terms | standard payment approach to commercial purchasing. the buyer and supplier specify and negotiate a standard credit period |

| credit limit | suppliers will credit reference in order to check buyer can afford product or service |

| stage or progress payments | usually used for capital projects. An initial payment is paid, then followed up with agreed percentage payments at agreed 'stages' of project completion |

| commercial and legal considerations in regard to payment terms | the length of credit periods is important for a) securing cashflow b) as a bargaining tool c) as a source of short-term finance |

| express payment terms are used to specify | 1. when goods will be paid for 2. what interest, if any, the buyer will be liable for in the event of late payment 3. whether time for payment will be 'of the essence' of the agreement, giving the supplier the right to repudiate the contract if the buyer fails to pay on time |

| Romalpa clause | when a supplier has the rights to retain ownership of the good and/or service until they goods/services have been paid for in full. this allows the supplier to reposes the goods if the buyer does not pay for them. |

| CHAPTER 9 make/do vs buy decisions | Three levels of planning: 1. Strategic: determine the long-term activities, capabilities and resources 2. tactical: reflect the organisations response to short term changes 3. operational: product design and manufacturing decisions |

| factors which influence make/do vs buy decisions | 1. strategically important / 'core' business 2. availability of in-house resources in-house competencies / capability 3. availability of suitable external suppliers 4. assessed risks 5. human resource impacts e.g. need of training or cause redundancies |

| advantages of making / doing | 1. opportunity to extract value from otherwise idle resources and capacity 2. potential for time reductions 3. cost of work is known in advance 4. can exert direct control over production and quality 5. confidentiality is better protected 6. less supply risk and supplier risk 7. helps to maintain a stable workforce |

| advantages of buying in / outsourcing | 1. quantity of work required is too small for economic reduction 2. avoid costs of specialist machinery and labour 3. financial risk shared with supply chain 4. access to contractors specialist research, expertise, technology, designs etc 5. helps to maintain a stable workforce in periods of rising sales |

| supply chain management | the management of upstream and downstream relationships with suppliers and customers to deliver superior customer value at less cost to the supply chain as a whole |

| outsourcing | the transfer of responsibility to a third party of activities which used to be performed internally can occur on 1) a project basis or 2) ongoing responsibility e.g cleaning or security |

| subcontracting | the use of an outside organisation to do work that the buying organisation cannot do itself, often due to lack of capacity and resources |

| globalisation | the increasing integration of internationally dispersed economic activities |

| drivers for outsourcing | 1. quality 2. cost 3. business focus 4. financial 5. relationship (minimise supply chain conflict) 6. human resource |

| benefits of outsourcing ** can only be secured by excellent supplier relationship management because of risks of selecting the wrong supplier, service standards, ethical issues etc | 1. focus its staff and other resources on its core competitive competencies 2. leverage specialist expertise, technologies, resources and economies of scale of suppliers 3. increases the flexibility of productive capacity in response to demand changes 4. cost certainty in the performance of activities |

| risks / disadvantages of outsourcing ** | 1. potentially higher cost of services 2. difficulty ensuring service quality and consistency and CSR 3. potential loss on in-house expertise, knowledge, contacts or technologies 4. reputation risk - dependent on suppliers 5. added distance from customer / end-user may weaken comms and relationships 6.risk over confidential data and property 7. ethical and employee relations issues |

| costs involved in outsourcing | 1. planning and sourcing costs 2. contractual price (supplier payments) 3. failure costs 4. performance costs 5. hidden costs (specification ambiguity, over-specifying service levels, opportunity cost of lost skills, experience in-house) |

| offshoring | the relocation of business processes to a lower-cost location, usually overseas |

| advantages of 'in-sourcing' | 1. transaction costs are low 2. the relationship between the customer and 'supplier' is likely to be long-term and stable 3. higher quality of service - no profit motive 4. customer and supplier are part of the same organisation, so should share same values |

| competencies --> non-core competencies should be outsourced | the activities or processes through which the organisation deploys its resources effectively. two types of competencies: 1. threshold - basic capabilities / support 2. core - value adding and strategic |

| when should you out-source? | 1. non-core competency work 2. when external contractors have the required competency and capability 3. occasions where it will increase value for money 4. resource insensitive, discrete, and specialist |

| CHAPTER 10 main criteria for making a procurement proposal business case | 1. costs and benefits 2. evaluation of options 3. alignment with organisational needs and timescales |

{kind=link}

Möchten Sie mit GoConqr kostenlos Ihre eigenen Karteikarten erstellen? Mehr erfahren.