Descripción

|

|

Creado por Josiane Giacomelli

hace alrededor de 7 años

|

|

Página 1

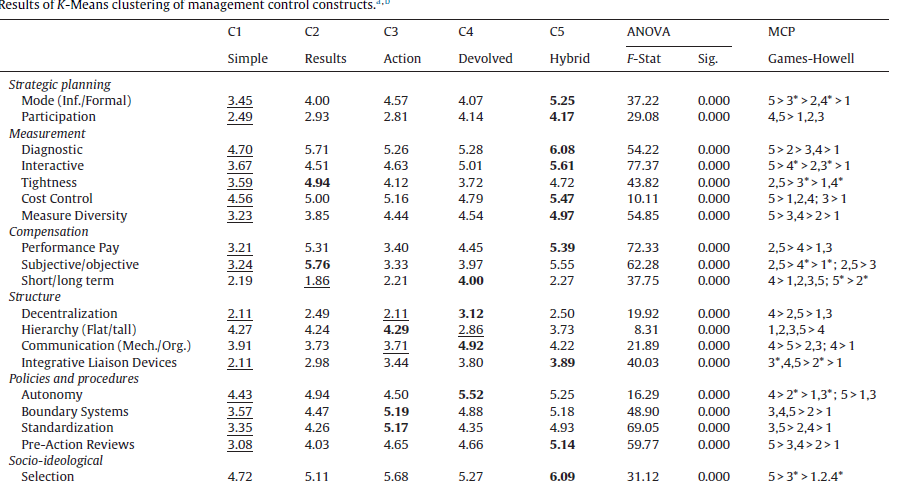

accounting and other control mechanisms combine as apackage and the associations these combinations havewith contextual circumstances. Specifically, this studydevelops a taxonomy of control configurations. The configuration approach contends that a compre-hensive understanding of accounting and control structurediversity requires organizations to be investigated asmultidimensional arrangements of interrelated compo-nents Configuration refers to a specific arrangement of multiple parts,components, elements, mechanisms, attributes, or the like. The first is to providean understanding of the control logic underpinning eachconfiguration.29The second is to further validate the clus-ter solution. Simple (C1) - The relatively unelaborated pattern that emerges inC1 suggests that the basis for control and coordina-tion is largely informal, achieved through centraliseddecision-making Results (C2) and action (C3) controlFirms in C2 place a high emphasis on the diagnosticuse and tight application of accounting information andobjectively determined, performance-based compensation(>C1,C3,C4). Devolved control (C4) - The central thread of these structures is a shift in thelocus of authority from managers to subordinates, wherecoordination primarily occurs through self-organizationand mutual adjustment, such that “control of the work restsin the hands of the doers” Hybrid control (C5) - The final cluster represents the most elaboratedarrangement, characterised by an intensive and demand-ing application of accounting and a significant bureaucraticapparatus.

{kind=link}

¿Quieres crear tus propios Apuntes gratis con GoConqr? Más información.