4994357

Descripción

Mapa Mental por Kevin Reynolds, actualizado hace más de 1 año

|

|

Creado por Kevin Reynolds

hace casi 9 años

|

|

Accounting Equation and the

Accounting Cycle

- Accounting Cycle

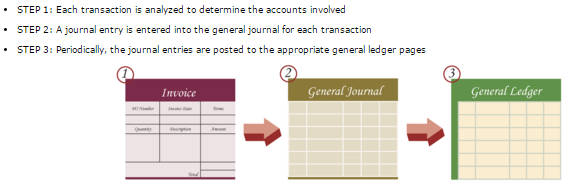

- 1) Transactions and events (source documents)

- 2) Books of original entry (journals)

- A book in which business transactions are recorded as they

happen. Both the debits and the credits of the entire transaction

are recorded in one place. The journal is a diary for the business

in which you record in day-by-day or chronological order all the

events involving financial affairs. A transaction is always recorded

first in the journal. In the general journal you must enter the

account to be debited and the account to be credited and the

amounts.

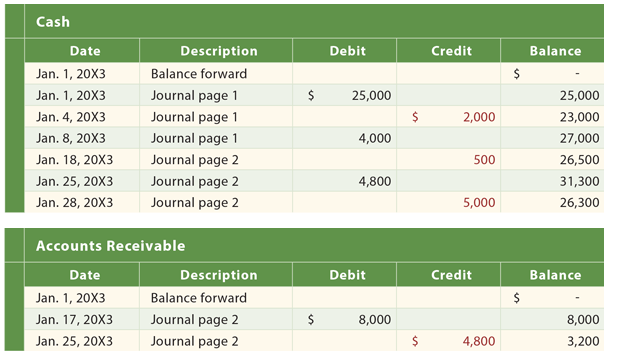

- Once a transaction is recorded in the general journal, the amounts are then posted to the

appropriate accounts. Accounts (such as Cash, Accounts Receivable, Equipment, Accumulated

Depreciation, Accounts Payable, Sales, Telephone Expense, etc.) are contained in the general ledger.

- Once a transaction is recorded in the general journal, the amounts are then posted to the

appropriate accounts. Accounts (such as Cash, Accounts Receivable, Equipment, Accumulated

Depreciation, Accounts Payable, Sales, Telephone Expense, etc.) are contained in the general ledger.

- A book in which business transactions are recorded as they

happen. Both the debits and the credits of the entire transaction

are recorded in one place. The journal is a diary for the business

in which you record in day-by-day or chronological order all the

events involving financial affairs. A transaction is always recorded

first in the journal. In the general journal you must enter the

account to be debited and the account to be credited and the

amounts.

- 3) Record to general / subsidiary ledgers

Nota:

- The general ledger is, in essence, another notebook that contains a page for each and every account in use by a company. Examples would include: *Cash Accounts *Payable Service *Revenue Accounts *Receivable Notes *Payable Advertising *Expense Land Capital *Stock Utilities ExpenseThe general ledger will include a separate page for each of these nine accounts.

- Used to sort and store balance sheet and

income statement transactions (taken from a

chart of accounts)

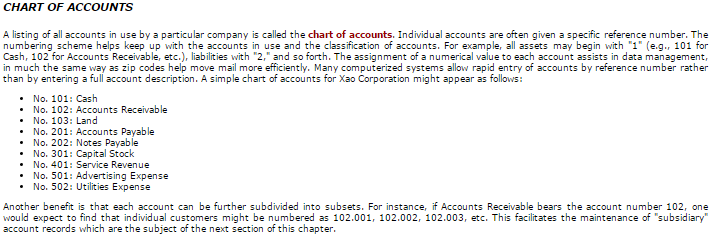

- Chart of Accounts

- Chart of Accounts

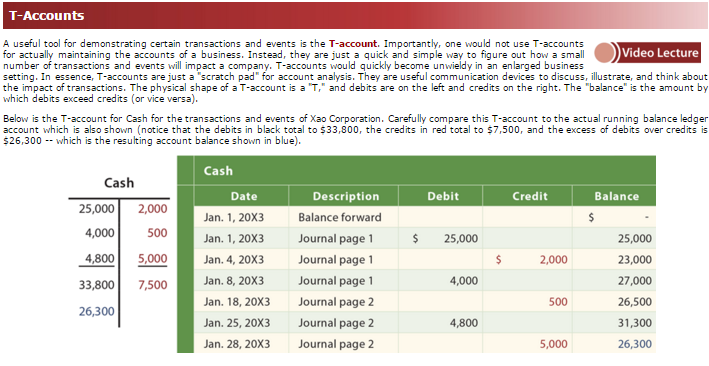

- T-accounts display the balances in each account. Each journal entry is

transferred from the general journal to the corresponding T-account.

Nota:

- A useful tool for demonstrating certain transactions and events is the T-account. Importantly, one would not use T-accounts for actually maintaining the accounts of a business. Instead, they are just a quick and simple way to figure out how a small number of transactions and events will impact a company.

- Posting - copy the entries listed in the journal into their

respective ledger accounts

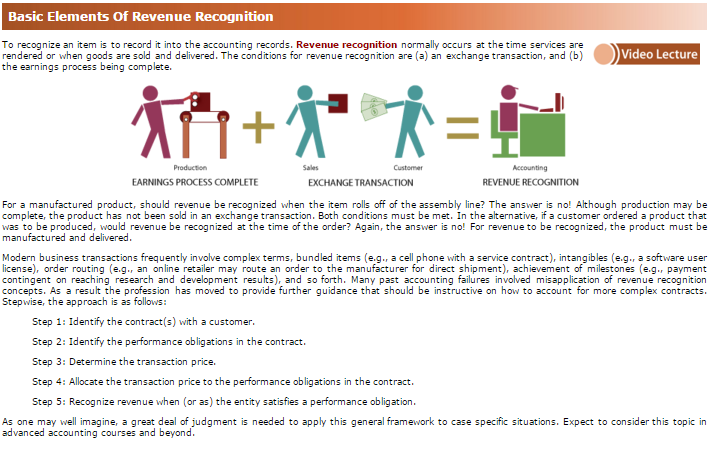

- Revenue / Expense Recognition

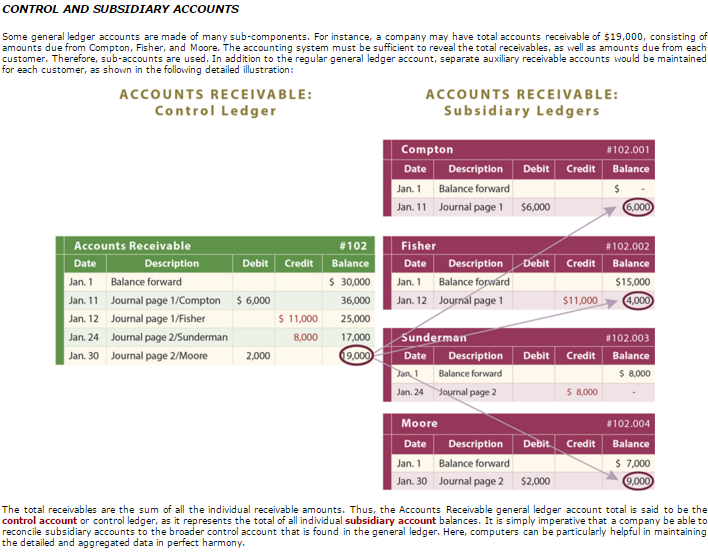

- Subsidiary Ledger

- T-Account

- Depreciation

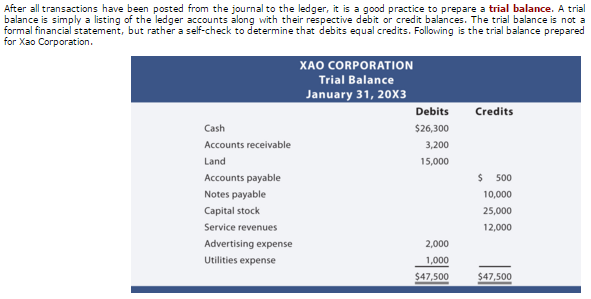

- 4) prepare an unadjusted trial balance

- 5) Adjusting entries

- Reversing entries

- Reversing entries

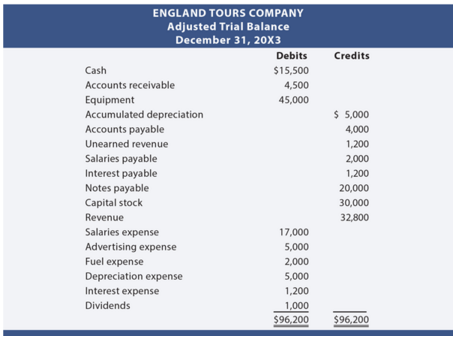

- 6) Adjusted trial balance

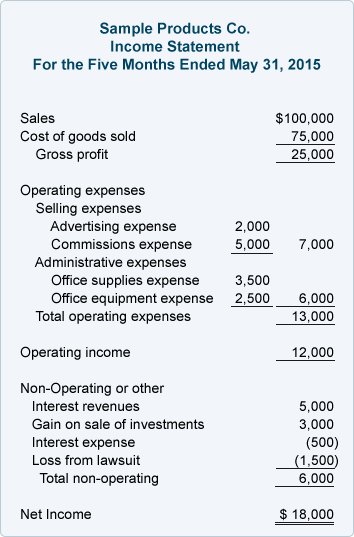

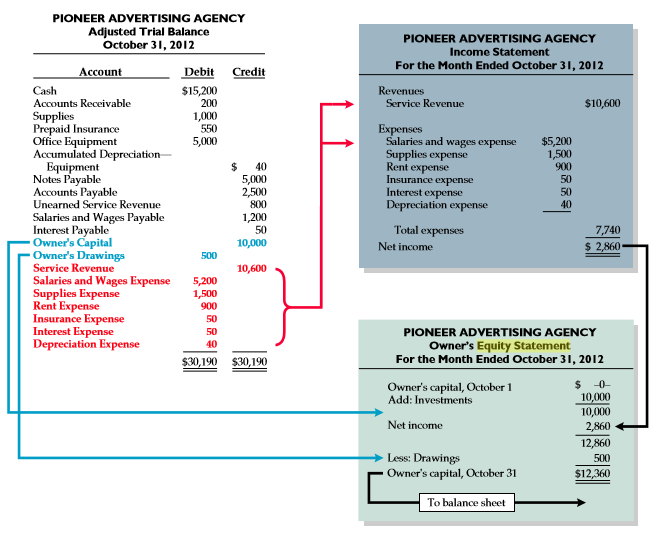

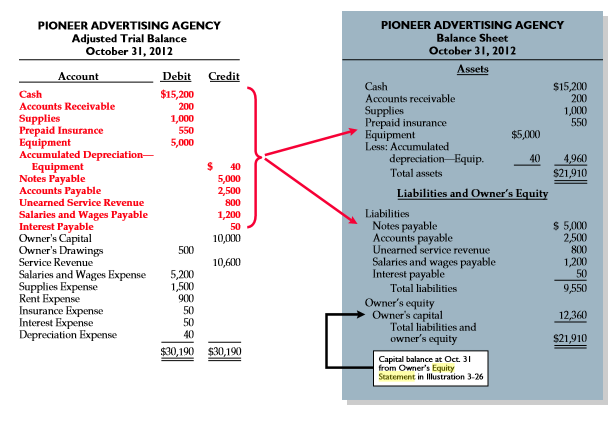

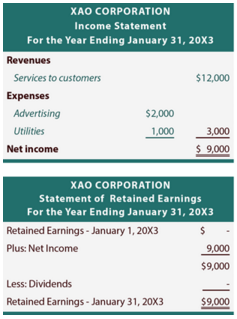

- 7) Financial statements

- Balance Sheet

- Income Statement

- Cash Flow Statement

Nota:

- The cash flow statement is a snapshot of a firm's financial resources and obligations at a single point in time, and the income statement summarizes a firm's financial transactions over an interval of time.

- Statement of

owner's equity

- Balance Sheet

- 8) Closing entries

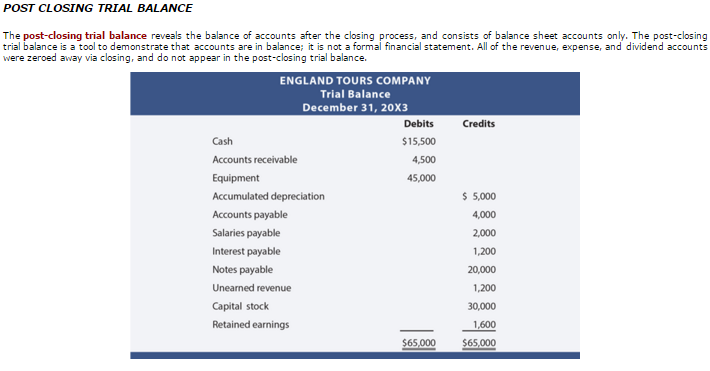

- 9) post-closing trial balance

- 1) Transactions and events (source documents)

Recursos multimedia adjuntos

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

¿Quieres crear tus propios Mapas Mentales gratis con GoConqr? Más información.