5800845

Descrição

Mapa Mental por Freda Fung, atualizado more than 1 year ago

|

|

Criado por Freda Fung

aproximadamente 8 anos atrás

|

|

Economic Feasibility

- Assessment factors

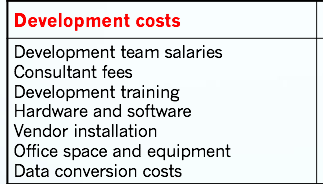

- Development Costs

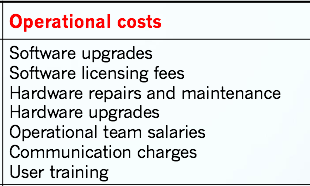

- Operational Costs

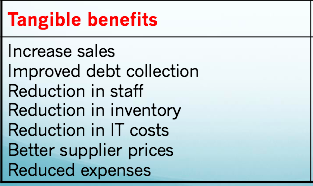

- Tangible Benefits

- Annual benefits

- Scalability and upgradability

- Intangible Benefits

- Development Costs

- enables organisation to make the go/no-go decision on projects.

- measure of how beneficial or practical an information system will be to an organization.

- Results of a feasibility study serve as an input to the business case

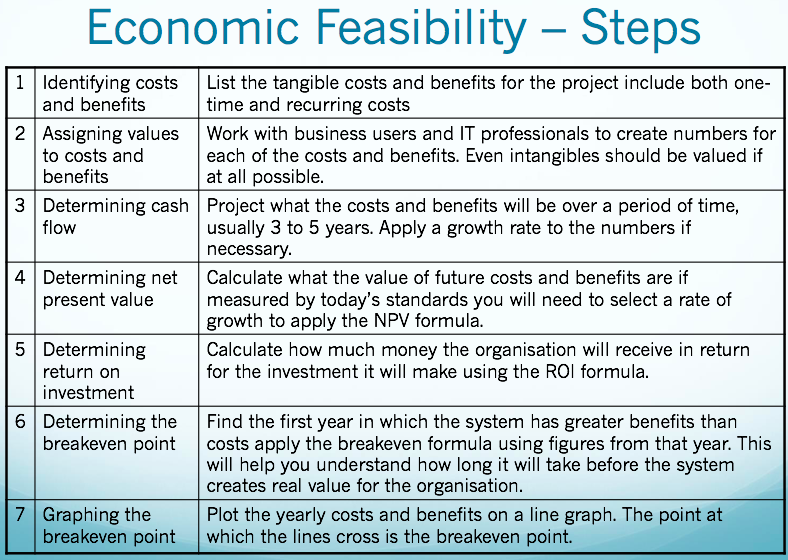

- Steps

- Techniques

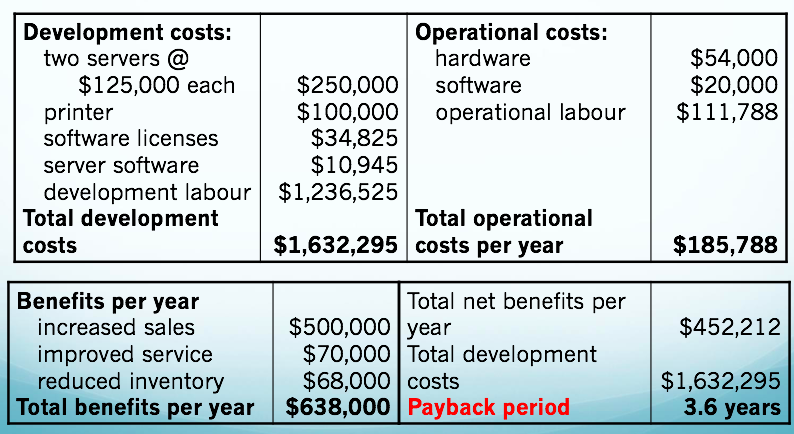

- Payback Analysis

- determining if and when an investment will pay for itself

- calculates the period within which the investment will be recovered.

- calculates the period within which the investment will be recovered.

- Payback period

Anotações:

- the period of time that will lapse before accrued benefits overtake accrued and continuing costs.

- Payback Period = Net Investment / Average Annual Cash Flow

- Ignores inflation and rate of interest

- determining if and when an investment will pay for itself

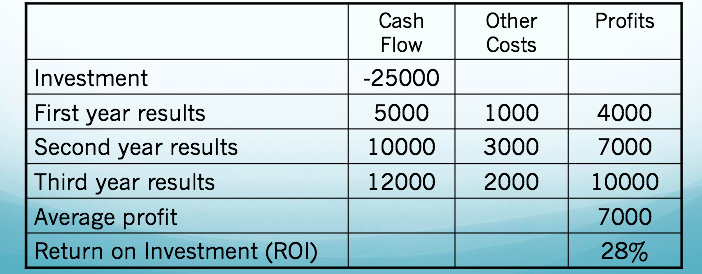

- Return On Investment

- comparing alternative investment opportunities

- Ignores inflation and rate of interest

- Return on Investment (ROI) = Annual Profit / Investment

- Calculates the annual rate of return or profit from the investment

- comparing alternative investment opportunities

- Discounted Cash Flow Techniques

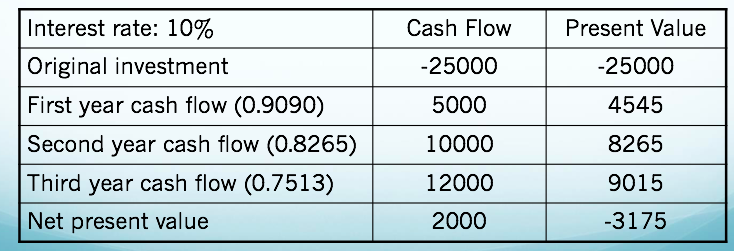

- Net Present Value

- All future cash flows are adjusted to present value

- Net present value = Original Investment +

Current value of all future cash flows

- NPV < 0 / NPV > 0

Anotações:

- In the case of multiple investments and returns, the NPV of all returns should be greater than the NPV of all investments – so the project is profitable

- NPV < 0 / NPV > 0

- All future cash flows are adjusted to present value

- Annuity and Net Present Value

- Internal Rate of Return

- Time Value of Money

- Interest

- Paid to compensate for the depreciation in money value

- Simple Interest: Interest is not re-invested

- Interest = Principal x Rate of Interest x Time (PxRxT=I)

- Interest = Principal x Rate of Interest x Time (PxRxT=I)

- Compound Interest: Interest is added to the

principal and re-invested

- Interest = Principal [(1 + Rate)n – 1]

- Interest = Principal [(1 + Rate)n – 1]

- Paid to compensate for the depreciation in money value

- Future Value of Money

- The future value of an

investment after periods (n)

of time is:

- Future Value = Principal + Compound Interest

- Future Value = Principal x (1 + Rate)n

- Future Value = Principal + Compound Interest

- The future value of an

investment after periods (n)

of time is:

- Net Present Value

- Payback Analysis

- Cost Benefit Analysis (CBA)

Anotações:

- assessing the appropriateness of an investment, based on the projected flow of costs, and the benefits expected to result from the investment.

- Appropriateness of investment

Anotações:

- to be assessed based on the above

- projected flow of costs

- outlay of cash required

Anotações:

- Any outlay of cash required for the initial purchase or maintenance of the investment at any point during the investment’s useful life.

- opportunity costs

- Identifying Costs

- Determine monetary value and timing of project costs

Anotações:

- both immediate and on-going

- Consider both direct and indirect project costs.

- Agree with project sponsor on how to deal with indirect or intangible costs.

- Document all assumptions

Anotações:

- to be clarified, or vague areas identified

- Identify alternatives

- Determine monetary value and timing of project costs

- Full Cost of Systems

- Cost of the software, initial purchase and updates

- Cost of any additional hardware requirements

- Cost of ongoing systems

support, internal and external

- Cost of initial training and

any refresher training

- Costs associated with having to

forego other activities

Anotações:

- that could have either saved money or increased revenues while staff are engaged in the project

- Cost of the software, initial purchase and updates

- Area that Costs That Will Arise

- People

- Hardware

- Software

- Data/Processes

- Networking

- Documentation

- People

- Developing the project cash flow schedule

- Determine the evaluation horizon –

usually three to five years

- Determine the time

periods (years or

months) to be used

- Allocate anticipated costs and

benefits across the schedule

- Calculate net cash flow

for each time period

- Determine the evaluation horizon –

usually three to five years

- outlay of cash required

- benefits expected to result from the investment.

- Any returns

Anotações:

- Any returns to the organization resulting from the investment that occur at any time during the investment’s useful life.

- e.g. Reductions in current costs Increased capacity to generate new revenue generating output

- Identifying the Benefits

- Identify the project benefits

- Work with the project sponsor

- project goals and objectives

Anotações:

- Primary sources

- Start with expected tangible benefits

- Determine monetary value and timing

- Document all assumptions

- Determine monetary value and timing

- Discuss how intangible benefits are to be presented.

- Transform intangibles to tangibles (sometimes).

- Identify the project benefits

- Any returns

- Limitations

- under-estimate actual costs.

- over-estimate cost savings.

- Most estimates of staff

reductions are never realized

- Most cost-benefit analyses

ignore the value of new

opportunities.

- under-estimate actual costs.

Anexos de mídia

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Quer criar seus próprios Mapas Mentais gratuitos com a GoConqr? Saiba mais.