7194484

Descrição

Mapa Mental por Kieran Deaville, atualizado more than 1 year ago

|

|

Criado por Kieran Deaville

aproximadamente 8 anos atrás

|

|

3) Perfect Competition, Imperfectly

Competitive Markets & Monopoly

- Contestable &

Non-Contestable Markets

- Contestable Market; A market in which the potential

exists for news firms to enter the market. Perfectly

contestable market has no entry/exit barriers + no

sunk costs. Incumbent firms & new firms have access

to same level of technology

- Assumptions

- Firms are short run profit maximisers,

producing where MC=MR

- Number of firms in industry can

vary from one to many.

- No single firm having big share of market

- Firms compete & do not collude. Freedom of entry/exit

- In contestable market theory, monopoly

power is not dependant upon the number of

firms/concentration ratio's but the difficulty

of which new firms can enter the market

- For a market to

be perfectly

contestable there

must be no

barriers to

entry/exit hence

no sunk costs.

- Sunk Costs;

Costs incurred

when entering

a market that

are

irrecoverable

- Sunk Costs;

Costs incurred

when entering

a market that

are

irrecoverable

- Because of ease of entry

making a market contestable

the threat of hit & run

competition is sufficient to keep

prices & profits at lowest levels

- Hit & Run Competition;

Occurs when a new entrant

can 'hit' the market, make

profits. then 'run; given

no/low exit barriers

- Hit & Run Competition;

Occurs when a new entrant

can 'hit' the market, make

profits. then 'run; given

no/low exit barriers

- Firms are short run profit maximisers,

producing where MC=MR

- Contestable Market; A market in which the potential

exists for news firms to enter the market. Perfectly

contestable market has no entry/exit barriers + no

sunk costs. Incumbent firms & new firms have access

to same level of technology

- Objectives of

Firms

- Other objectives: 1) Providing good

quality & service especially

important for socially minded

owners/managers 2) Growth

maximisation through achieving

economies of scale. Growth can

mean a gain in monopoly

power/managerial prestige 3)

Survial = fear of losses & closure,

survial being a primary objective 4)

Revenue Maximisation occurs

through the level of output at

which managerial revenue is zero

through managerial pay linked to

revenue rather than profit 5)

Satisficing Principle = Satisfactory

outcome may help to resolve the

conflict between manager &

shareholders objectives,

attempting to satisfice aspirations

of many groups for a firm means

compromise & achieving minimum

rather than maximum targets

- Profit Maximisation

- Profit maximisation,

the firm produces the

level of output that TR -

TC is maximised

- MR = MC means a firm's profits are greatest

when the addition to sales revenue from last

unit sold equals addition total cost from

production of last unit of output

- MR > MC Profits rise when output increases

- MR < MC Profits rise when output decreases

- MR > MC Profits rise when output increases

- MR = MC means a firm's profits are greatest

when the addition to sales revenue from last

unit sold equals addition total cost from

production of last unit of output

- If succeeds in producing & selling the output

yielding the biggest possible profit, no incentive to

change level of output

- Firms in all market structures can only maximise profit when MR = MC

- Profit maximisation,

the firm produces the

level of output that TR -

TC is maximised

- Divorce of Ownership From

Control

- Divorce of Ownership From Control; The owners & those who manage the firm are

different groups with different objectives

- Conflicts may occur between the

agents & principals when the

incentives which effect their

behaviour are not the same. Agent

does not usually receive the full

benefit of their actions, destroys the

incentive for the agent to put same

effort into tasks

- Reasons why an agent can

get away with not acting in

best interest of principle 1)

cost of sacking/punishment is

too high relative at any

benefit 2) information

asymmetry, the agent knows

more than the principle

- Various methods

can be used to

realign the

incentives facing

the owners of

businesses &

managers, Profit

related pay, giving

company shares

etc...

- Divorce of Ownership From Control; The owners & those who manage the firm are

different groups with different objectives

- Other objectives: 1) Providing good

quality & service especially

important for socially minded

owners/managers 2) Growth

maximisation through achieving

economies of scale. Growth can

mean a gain in monopoly

power/managerial prestige 3)

Survial = fear of losses & closure,

survial being a primary objective 4)

Revenue Maximisation occurs

through the level of output at

which managerial revenue is zero

through managerial pay linked to

revenue rather than profit 5)

Satisficing Principle = Satisfactory

outcome may help to resolve the

conflict between manager &

shareholders objectives,

attempting to satisfice aspirations

of many groups for a firm means

compromise & achieving minimum

rather than maximum targets

- Oligopoly

- Concentration Ratio; Measures

the Market Share of the biggest

firms in the market

- Good indicator of an

oligopolistic market.

Measures the market

structure % of the

biggest firms

- Concentration

Ratio of 5=80,

largest five firms

possess 80% of

market share

while 20% is

smaller firms

- Good indicator of an

oligopolistic market.

Measures the market

structure % of the

biggest firms

- • Competitive

oligopoly exists

when rival firms

are

interdependent

in the sense

they take into

account of other

firms reactions

when forming a

market strategy,

as result

uncertainty

occurs can

never be sure

how rivals react,

they are

non-collusive

- Cartels

- Collusive agreements to fix

prices, restrict output & deter

entry of new firms

- Cartel agreements

enable inefficient

firms to stay in

business, while

more efficient

members enjoy

abnormal profits.

- Some forms of co-operation or cartel may be justifiable, including

joint product development i.e. Ford & Volkswagen + improving health

& safety or to ensure product & labour standards are maintained.

- Collusive agreements to fix

prices, restrict output & deter

entry of new firms

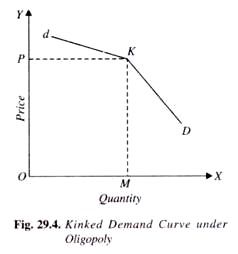

- Kinked Demand Schedule

- Developed by Paul Sweezy in the late 1930's, model

assumes there will be asymmetric reaction

- Criticisms:

1. Doesn’t explain

where market

clearing prices

come from

2. Theory only

deals with price

competition

3. No guarantee

that firms will

react the same

- Developed by Paul Sweezy in the late 1930's, model

assumes there will be asymmetric reaction

- Cartel agreements

ensure the

protection of

inefficient firms &

to enjoy an easy

life protected from

competition

- Price leadership

can occur in an

oligopoly when

a firm becomes

market leader

& other firms in

the industry

follow its

pricing example

- Price Leadership;

Setting of prices

in a market

usually y a

dominant firm

which other

firms follow

known as

benchmark

- Price Leadership;

Setting of prices

in a market

usually y a

dominant firm

which other

firms follow

known as

benchmark

- Members of

a cartel

often fix the

prices that

all members

of cartel

charge,

these price

agreements

- Price Agreement; An

agreement between

a firm and other

firms e.g. supplier

or customers

regarding the

pricing of a

good/service

- Price Agreement; An

agreement between

a firm and other

firms e.g. supplier

or customers

regarding the

pricing of a

good/service

- Price wars take

place both in

monopolistic

competition &

oligopoly which

may be started

accidentally or

deliberate to

damage

competitors

- Price Wars;

Occurs when

rival firms

continuously

lower price to

undercut each

other

- Price Wars;

Occurs when

rival firms

continuously

lower price to

undercut each

other

- Another

feature of

oligopoly is

the desire to

keep other

firms out of

industry, so

entry barriers

emerge

- Firms in oligopolistic

market are observed to

keep prices at a

constant level this

known as price rigidity,

as prices are relatively

stable (Sticky Prices)

- Most industries in

the UK are

oligopolistic since

dominated by few

firms

- Oligopolstic Firms also compete using non price competition

- Marketing

strategy

used to

distinguish

between

firm's

products &

services

- Likely to increase expenditure for firms e.g. marketing as trying to promote its own product above competition

- e.g. a supermarket issuing loyalty cards is a form of non price competition

- Marketing

strategy

used to

distinguish

between

firm's

products &

services

- Concentration Ratio; Measures

the Market Share of the biggest

firms in the market

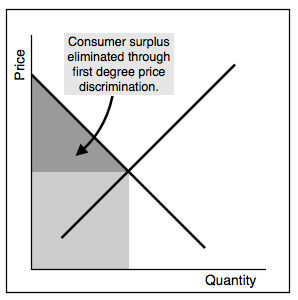

- Price Discrimination

- Both monopolists & oligopolists may be in

a position to price discriminate

- Firms who sell a product

at one price realise that

their profit could

increase if they could

appropriate more

consumer surplus

- Conditions

- The resale can be prevented from

one buyer to another

- Different elasticity's of demand some buyers

prepared to pay more than others

- The vendor can control whatever is

offered & no others firms present that can

sell at lower price in the area

- The resale can be prevented from

one buyer to another

- Methods

- Age

- Time

- Geographical

- Age

- Types

- First Degree

- Known as perfect price

discrimination, each unit

sold at maximum price

- Known as perfect price

discrimination, each unit

sold at maximum price

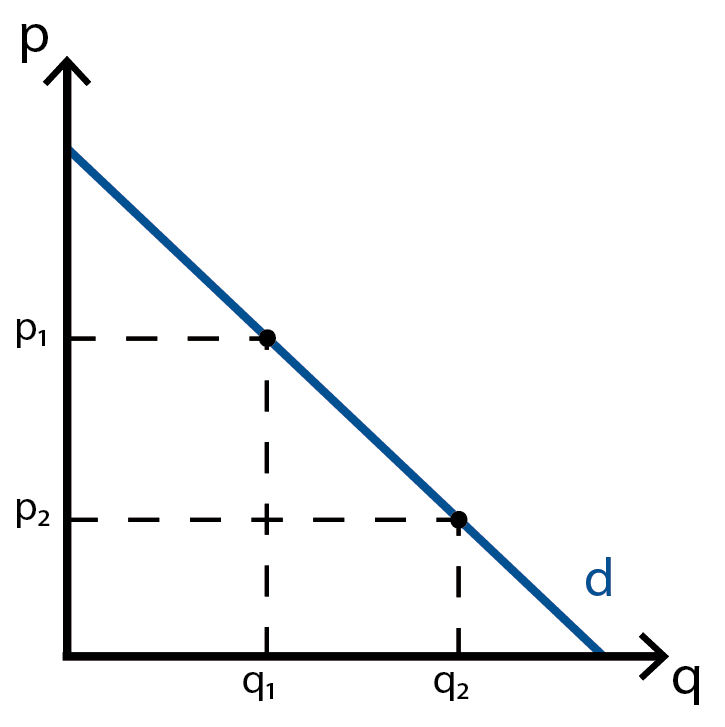

- Second

Degree

- Consumers are charged different

prices for blocks of consumption

- Consumers are charged different

prices for blocks of consumption

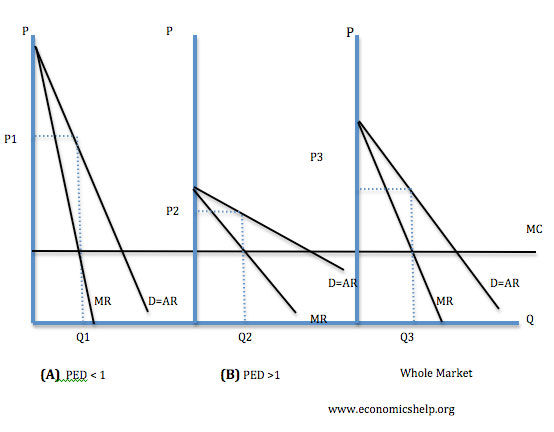

- Third

Degree

- Same product/service sold

at different prices to

different consumers in

different markets

- Same product/service sold

at different prices to

different consumers in

different markets

- First Degree

- Advantages

- Price Discrimination allows firms to

increase profits by taking away

consumer surplus and converting into

abnormal profit

- Allows firms to use up

spare capacity

- Price Discrimination allows firms to

increase profits by taking away

consumer surplus and converting into

abnormal profit

- Both monopolists & oligopolists may be in

a position to price discriminate

- Monopoly & Monopoly

Power

- Disadvantages: Market

Failure & Resource

Allocation: Output falls,

price rises & under

consumption of the good

the monopoly produces

- Advantages:

Economies of scale:

Because of limited

market size, there is

insufficient room for

more than one firm

benefitting from

economies of scale.

- By assumption monopoly

able to produce output Q1

at a LRAC of AC1, whereas

competitive firms are

unable to produce this

output without destroying

the competitive market

- Monopoly & Economic Efficiency

- Assuming an

absence of

economies of

scale,

monopoly

equilibrium is

productively &

allocatively

effiecient

- Monopoly is

also

allocatively

inefficient

since profit

maximising

price is above

marginal cost

- Assuming an

absence of

economies of

scale,

monopoly

equilibrium is

productively &

allocatively

effiecient

- Monopoly & Economic Efficiency

- By assumption monopoly

able to produce output Q1

at a LRAC of AC1, whereas

competitive firms are

unable to produce this

output without destroying

the competitive market

- Advantages: Dynamic

Efficiency:

Improvements in

productive efficiency

especially resulting

from technical

progress & innovation.

Monopolies can make

abnormal profits in

short & long run. This

profit invested in R&D

- Monopoly

is often

used in a

much

looser way

to

describe

any

market in

which

there is a

dominant

firm

- Monopoly; One firm

only in a market

- Monopoly; One firm

only in a market

- A monopoly is

protected by

barriers to entry

which prevent new

firms entering the

market to share

abnormal profit.

Barriers enable the

monopolist to

preserve abnormal

profits in long run &

short run

- Disadvantages: Market

Failure & Resource

Allocation: Output falls,

price rises & under

consumption of the good

the monopoly produces

- Perfect Competition

- Short Run Profit Maximisation

- Each firm in a

perfectly

competitive

market

accepts the

ruling market

price, which

becomes each

firm's

average

revenue &

marginal

revenue curve

- A perfectly

competitive

firm can sell

as much as

it wishes at

the

market's

ruling price

- Each firm in a

perfectly

competitive

market

accepts the

ruling market

price, which

becomes each

firm's

average

revenue &

marginal

revenue curve

- Lon Run Profit

Maximisation

- Too many new

firms enter the

market since

abnormal profits

can be made,

supply curve shifts

to the right. Price

falls to P1. Firms

make a loss

(Supernormal

Profits) so firms

leave market

- When firms

start leaving

the supply

curve shifts to

the left,

eventually the

price settles so

surviving firms

only make

normal profit

- Perfect Competition &

Economic Efficiency

- Productive efficiency & allocative efficiency occurs only if; 1) All the firms in market beenfit from all available economies of scale at low levels of output,

MES has to be small in relation to market size 2) Perfectly competitive Markets for all goods & services where P = MC in every market 3) No externalities

- Productive efficiency & allocative efficiency occurs only if; 1) All the firms in market beenfit from all available economies of scale at low levels of output,

MES has to be small in relation to market size 2) Perfectly competitive Markets for all goods & services where P = MC in every market 3) No externalities

- Perfect Competition &

Economic Efficiency

- When firms

start leaving

the supply

curve shifts to

the left,

eventually the

price settles so

surviving firms

only make

normal profit

- Too many new

firms enter the

market since

abnormal profits

can be made,

supply curve shifts

to the right. Price

falls to P1. Firms

make a loss

(Supernormal

Profits) so firms

leave market

- Short Run Profit Maximisation

- Market Structures

- Market Structure;

the organisational &

other characteristics

of a market

- Important features of Market

Structure include; *number of firms

in market, *market share of largest

firms, *Nature of the costs incurred

by the firms, *nature of sales

revenue earned by firms, *barriers

to entry/exit, *ease of access to

information about what is going on

in market, *price-setting & product

differentiation *how buyer's

behaviour effects firms

- Distinguishing between different

market structures

- Number of Firms -

a requirement for

a firm to be

perfectly

competitive is

large number of

buyers/sellers

whilst Monopoly

there is just one

firm. In oligopoly

there are only a

few firms in the

market

- Market Entry Barriers - In the short run, where at least one factor of production is fixed (usually capital) firms cannot

enter or leave the market whatever the market structure. In the long run when all the factors of production are

variable firms can enter/leave competitive markets.

- Market Entry Barriers (2) - Pure monopoly is protected by entry barriers in long & short run, in

Oligopolistic markets there may be significant barriers in long run

- Market Entry Barriers (3) - An entry barrier is a cost of production which must be carried by a firm

that seeks to enter an industry. Not carried by businesses already in the industry. Closely related

to entry barriers are exit barriers

- Limit Pricing/Predatory Pricing - when natural barriers to market entry

low/non-existent firms already in the market use limit prices to deter new firms

entering market, firms already in the market sacrafice short run profit

maximisation with this method but instead seek to maximise long run profits

- Limit Pricing;

Prices set low

enough to make

it unprofitable

for other firms

to enter market

- Limit Pricing;

Prices set low

enough to make

it unprofitable

for other firms

to enter market

- Limit Pricing/Predatory Pricing (2) - Predatory pricing occurs when a firm deliberately sets prices below

costs to force new market entrants out of business, once new entrants left the market, the firm may

decide to restore prices

- Predatory Pricing; Prices set

below average cost with the

aim of forcing rival firms out

of business

- Predatory Pricing; Prices set

below average cost with the

aim of forcing rival firms out

of business

- Product Differentiation - Most firms large, medium or small engage in varying degrees of

product differentiation. Firms often produce a range of relatively similar products some of

which compete with each other but others aimed at different market segments

- Product Differentiation; The marketing of

generally similar products with minor

variations or marketing of a range of

products

- Product Differentiation; The marketing of

generally similar products with minor

variations or marketing of a range of

products

- Number of Firms -

a requirement for

a firm to be

perfectly

competitive is

large number of

buyers/sellers

whilst Monopoly

there is just one

firm. In oligopoly

there are only a

few firms in the

market

- Market Structure;

the organisational &

other characteristics

of a market

- Monopolistic Competition

- Monopolistic markets

resembles perfect

competition; Large

number of firms, no

barriers to entry/exit,

entry of new firms

attracted by short run

abnormal profits brings

down the price of each

firm can charge.

- Monopolistic

markets also

resemble

monopoly;

Each firm

faces a

downward

sloping

demand curve

as each firm

produces a

slightly

different

product, Each

firm's MR

curve is below

AR curve

- Short Run Profit

Maximisation

- Average revenue curve

represents demand for

goods produced by just

one firm within market

rather than demand for

the output of whole

market

- Profit Maximising

level of output, Q1

located below

point A where MC

= MR & abnormal

profits made

- Average revenue curve

represents demand for

goods produced by just

one firm within market

rather than demand for

the output of whole

market

- Short Run Profit

Maximisation

- Monopolistic

markets also

resemble

monopoly;

Each firm

faces a

downward

sloping

demand curve

as each firm

produces a

slightly

different

product, Each

firm's MR

curve is below

AR curve

- Long Run Profit

Maximisation

- Absence of barriers to

entry/exit, new firms enter

causing AR curve to shift inward

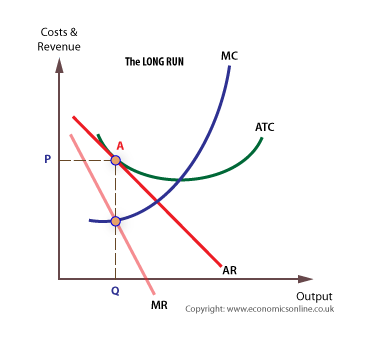

- Long Run profit maximisation occurs when AR curve

touches firm's ATC curve removing abnormal profit

- Absence of barriers to

entry/exit, new firms enter

causing AR curve to shift inward

- Monopolistic markets

resembles perfect

competition; Large

number of firms, no

barriers to entry/exit,

entry of new firms

attracted by short run

abnormal profits brings

down the price of each

firm can charge.

Anexos de mídia

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Quer criar seus próprios Mapas Mentais gratuitos com a GoConqr? Saiba mais.