Descrição

|

|

Criado por Erum Shabbir Arain

quase 9 anos atrás

|

|

Página 1

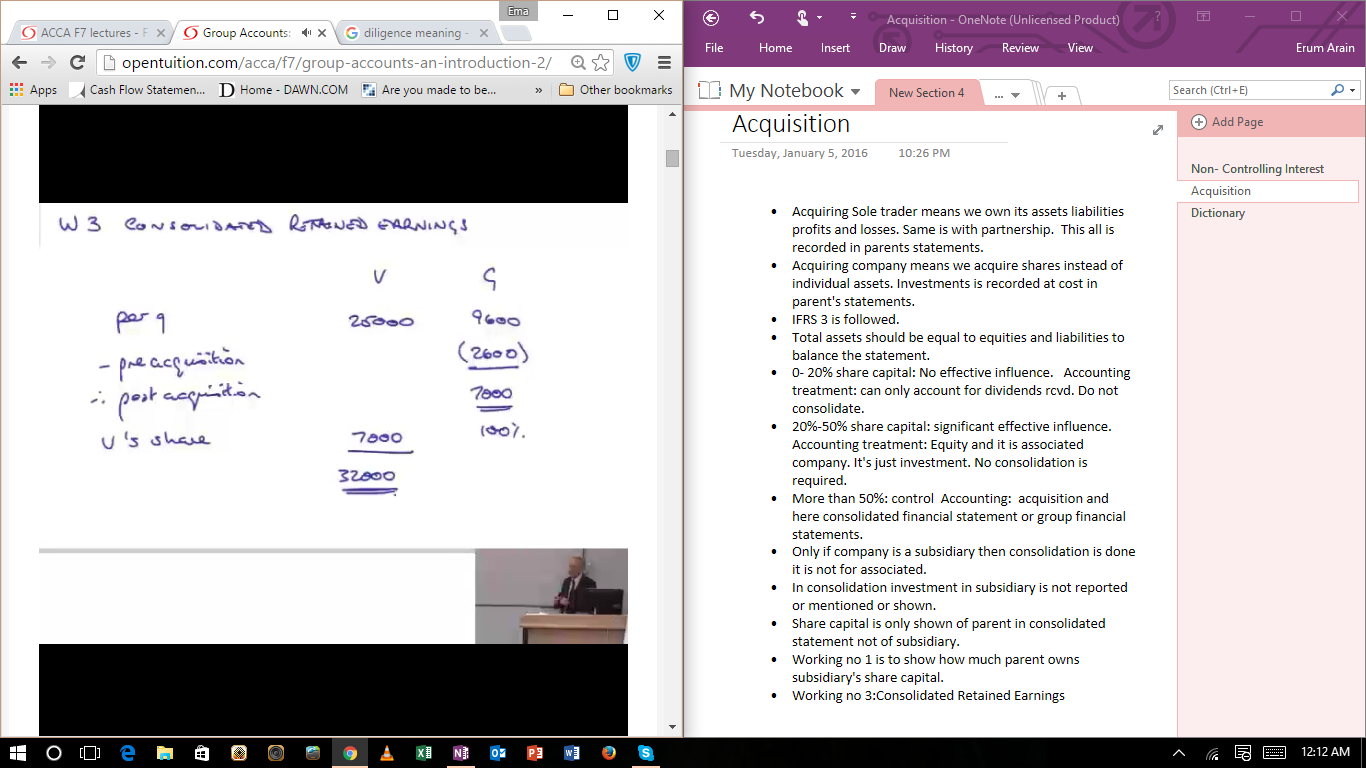

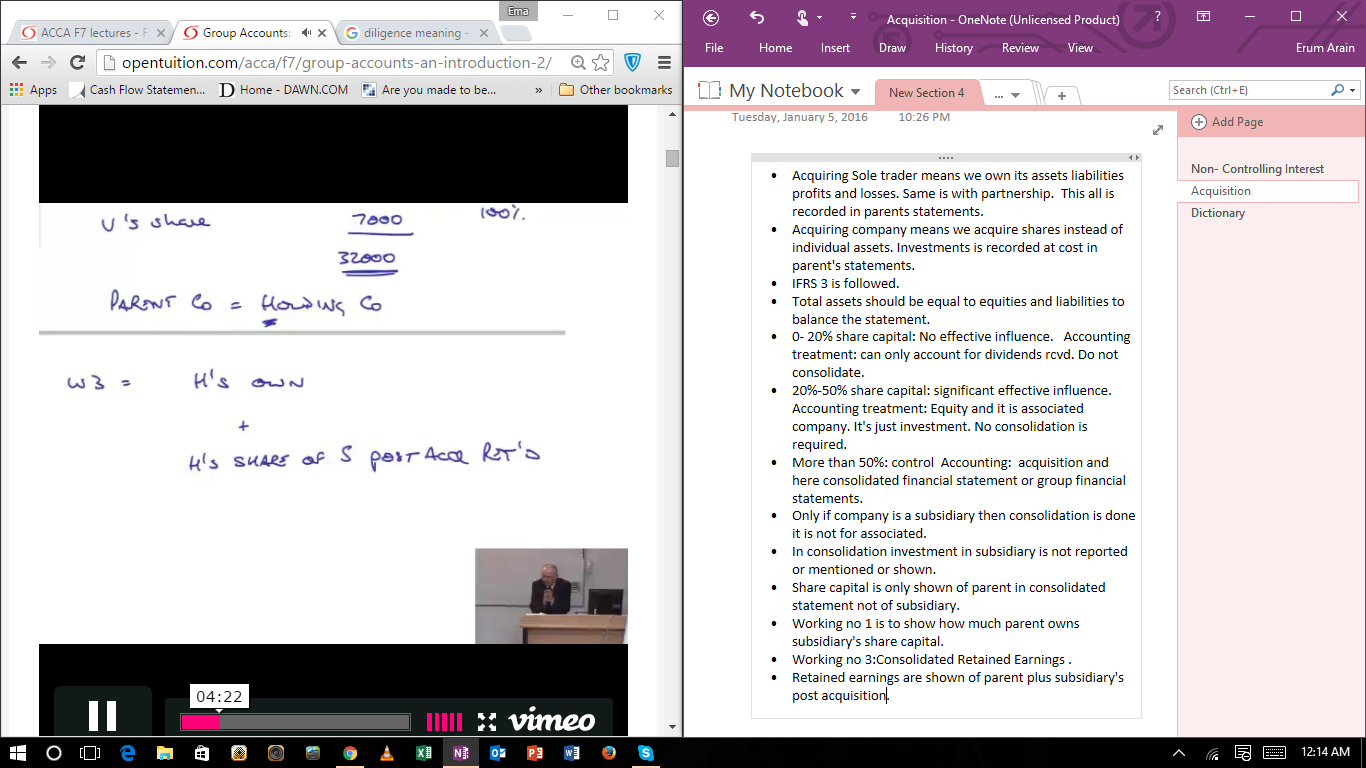

Acquiring Sole trader means we own its assets liabilities profits and losses. Same is with partnership. This all is recorded in parents statements. Acquiring company means we acquire shares instead of individual assets. Investments is recorded at cost in parent's statements. IFRS 3 is followed. Total assets should be equal to equities and liabilities to balance the statement. 0- 20% share capital: No effective influence. Accounting treatment: can only account for dividends rcvd. Do not consolidate. 20%-50% share capital: significant effective influence. Accounting treatment: Equity and it is associated company. It's just investment. No consolidation is required. More than 50%: control Accounting: acquisition and here consolidated financial statement or group financial statements. Only if company is a subsidiary then consolidation is done it is not for associated. In consolidation investment in subsidiary is not reported or mentioned or shown. Share capital is only shown of parent in consolidated statement not of subsidiary. Working no 1 is to show how much parent owns subsidiary's share capital. Working no 3:Consolidated Retained Earnings . Retained earnings are shown of parent plus subsidiary's post acquisition since we acquired subsidiary. W3 is done to achieve Consolidated retained earnings which have been achieved under the control of parent company. Sometimes it is not necessary that you have more than 50% of share capital and you do have the power to influence. Sometimes one may own less than 50% but can have an influencing right. E.g. If one lends u money and asks that on behalf of it you have to appoint my 2 directors, even I don't have the company's capital more than 50% but I can appoint in that case if the company agrees to it. Own more than half but don't have control Lender with power to appoint a majority of the board Company is in liquidation so power is transferred to liquidator even if one owns 100% of the company. Q: Where may a parent wish to exclude subsidiary form consolidation? A: Because of poor subsidiary performance. But IFRS3 says if one has subsidiary must show the subsidiary. Or because the expense of consolidation is greater than benefit. If Immaterial subsidiaries are there than 1 can exclude or do not show. To this auditors and directors must agree. Or because of Expense or delay I.e. year ends do not match Then the months coming in that accounting period of company are consolidated. Any subsidiary activity should be included until u get up to 75% u have to do segmented reporting. It was done before but not now.

{kind=link}

{kind=link}

Quer criar suas próprias Notas gratuitas com a GoConqr? Saiba mais.