Beschreibung

|

|

Erstellt von Sarah Egan

vor mehr als 7 Jahre

|

|

Seite 1

Foreward

On September 11, 2001 anyone associated with aviation knew that the industry would never be the same. What we did not know was how resilient the industry would be in the aftermath of the tragedy or the direction in which it would change. A decade after the event, there can be no doubt about aviation’s resilience. By 2004 revenues and traffic surpassed 2000 levels. And by 2006 aviation had returned to profitability—albeit with a weak 1.1% margin. In the interim airlines dealt with SARS, additional terrorist attempts, wars, and rising oil prices. It took three years to recover the $22 billion revenue drop (6%) between 2000 and 2001. When the global financial crisis struck in 2008, 2009 revenues fell by 14% ($82 billion) to $482 billion. This was largely recovered in the following year when industry revenues rose to $554 billion and airlines posted an $18 billion profit. Clearly the restructuring of the decade has left airlines leaner and more resilient in the face of crisis. Over the decade, the dimensions of global aviation have also changed. IATA expects 2011 airline revenues of $598 billion—nearly twice the $307 billion of 2001. Airlines are also expected to carry 2.8 billion passengers and 48 million tonnes of cargo. That’s a billion more people flying and 16 million more tonnes of cargo than in 2001. While it is difficult to isolate the impact of the events of 2001, we can say that they were a part of a chain of events that cost the industry three years of growth. The 2008 global financial crisis cost another two years of growth.The legacy of 9.11 is felt most in airport security. Aviation is more secure today than in 2001. But this has come at a great price in terms of passenger convenience and industry costs. As we move forward, there are five major lessons in security over the last decade: Governments must coordinate the development and deployment of security measures to ensure harmonized global standards and eliminate overlapping and redundant requirements among nations. Governments are obliged to foot the bill for security threats which are national challenges in the same manner as they would do in any other sector. Airlines and their passengers currently pay a security bill that had ballooned to $7.4 billion by 2010. Passengers should and do play an important role in helping keep air travel safe. Vigilance and cooperation with authorities are crucial. Governments need to embrace a risk-based approach to security screening. We must accept that there is no such thing as 100% risk-free security. Governments must focus on the probable and not all that is possible and avoid policies driven by knee-jerk reactions. A good place to start is by removing the hassle that comes between check-in and boarding at many airports. The building blocks to do a better job exist. The vision for IATA’s Checkpoint of the Future is for passengers to be able to get from curb to gate in a seamless and convenient process. For this, we need a risk-based approach to security powered by the enormous amount of data that we can and do collect on travelers. Combined with this will be technology that will allow most passengers to simply stroll through a checkpoint that can detect metal and harmful substances without stopping, stripping or unpacking. Parts of this vision could be realized with technology that exists today. Others are in development with a three to seven year horizon. The important thing is to keep focused on evolving the 40-year-old concept of today’s airport checkpoint into one that is more convenient, more effective and that can handle the ever increasing volume of people who want and need to fly. Finally, as we commemorate the tragedy of 9.11, the thoughts and prayers of the industry are with the families of the victims—passengers, crew and bystanders. Our best tribute to their memories is a resilient aviation industry. Aviation is a force for good and an instrument of peace that promotes trade, spreads wealth and facilitates understanding among the peoples and cultures of our world.

Seite 2

The Financial Impact of 9.11

9.11 was the beginning of the most challenging decade in aviation history. But it is important to note that the industry was already in a weak financial position. World trade had slowed and the ‘dot.com bubble’ had burst the year earlier. Global airline profits had fallen from $8.5 billion in 1999 to $3.7 billion in 2000.

{kind=link}

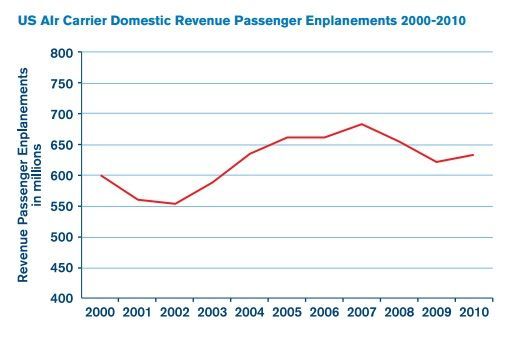

US Impact • Air Space Closed: On September 10, 2001, US airports handled 38,047 flights. On September 12, they handled 252 commercial flights. One week later (September 18) there were 34,743 flights.1 • Passenger Traffic: US passenger traffic, measured by revenue passenger kilometers (number of travelers multiplied by the distance traveled) declined 5.9% in 20012 (compared to 2000) and a further 1.4% in 2002. Airlines struggled to match this decline by cutting capacity (available seat kilometers or number of seats multiplied by distance traveled) by 2.8% in 2001 and a further 3.9% in 2002. This was the first time since World War II that industry capacity declined for two consecutive years. After stabilizing in 2003, capacity growth resumed in 2004 and continued until 2008, when it declined again owing to soaring oil prices and the global financial crisis. Capacity fell further in 2009, returning virtually to 2000 levels. Between 2000 and 2009, the US commercial aircraft fleet shrank by around 700 units. • Domestic Market: “The events of 9.11…marked a permanent decline in [US] domestic airline demand”—Barclays Capital, February 2009. Total domestic operating revenue per $100 of nominal US GDP declined from around US$0.823 in 2000 to US$0.687 in 2010, representing a shortfall of $18 billion for 2010 and $142 billion for the 2001-2010 period.3 Passengers found alternatives to short-haul travel to avoid the security hassles at airports. Network carriers shed their domestic operations to regional

Seite 3

Global Impact

Traffic: Global passenger traffic (tonne kilometers performed) declined by 2.7% in 2001 (see table below). Traffic did not surpass the 2000 level until 2003. It continued to rise until 2009 when, owing to the global financial crisis, it declined 2.1% year-onyear. • Revenues: Global airline revenues declined from $329 billion in 2000 to $307 billion in 2001 and further to $306 billion in 2002. Revenues rebounded to $322 billion in 2003 and then to $379 billion in 2004. The next revenue dip was in 2009 when they fell $82 billion to $482 billion. In percentage terms this 14% drop was more than twice the decline experienced in 2001-2. • Profitability: Airlines lost $13 billion in 2001 and a further $11.3 billion in 2002.The industry recorded its first post-September 11 annual profit in 2006 ($5 billion), and earned $14.7 billion in 2007. The following year rising oil prices and the global financial crisis plunged airlines back into the red with 2008-9 total losses of $25.9 billion. • Bankruptcies: Within months of the attacks, Swissair and Sabena went bankrupt as the 9.11 shock pushed these financially weak carriers into collapse. • Oil price: In the decade since 9.11 the industry fuel bill rose from 13% of costs (2001) to 30% (projected for 2011).

{kind=link}

Möchten Sie kostenlos Ihre eigenen Notizen mit GoConqr erstellen? Mehr erfahren.