16670596

| Question | Answer |

| What do FINANCIAL STATEMENTS usually consist of when dealing with a sole trader? | Financial statements prepared for a sole trader usually consist of a Trading and Profit and Loss account, and a Balance Sheet. |

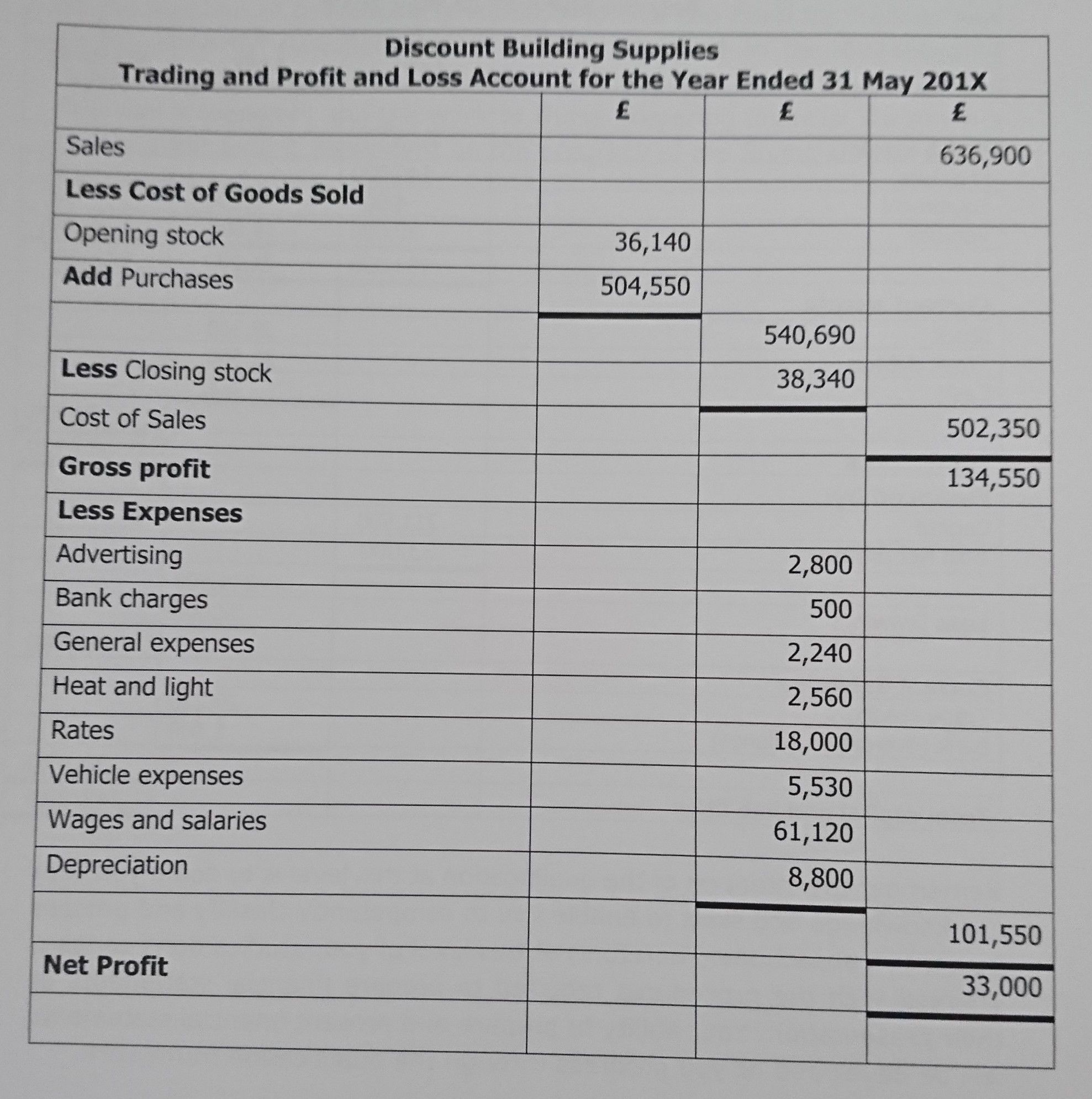

| What is a TRADING AND PROFIT AND LOSS ACCOUNT? | The trading and profit and loss account is prepared for a particular period of time. The balances on revenue income accounts and revenue expense accounts are transferred from the ledger to the TPLA. |

| What happens to the summary of the TRADING AND PROFIT AND LOSS ACCOUNT? | Having calculated the profit or loss for the trading period, the profit or loss is transferred to the trader's capital account. |

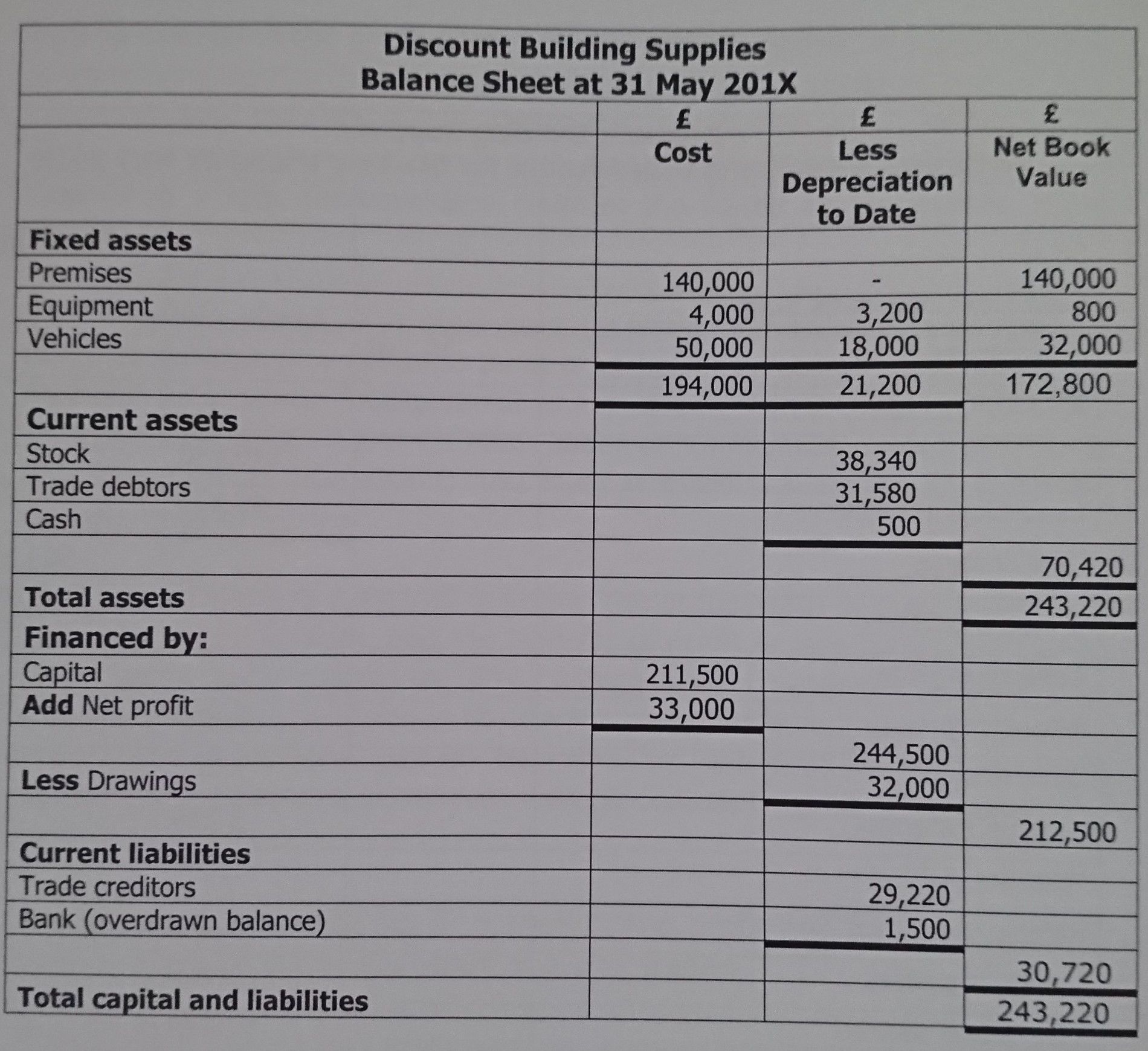

| What is a BALANCE SHEET? | A balance sheet is a statement showing the financial position of a business as at a particular point in time. It provides the reader with information relating to what a business owns and what it owes. |

| An example of a TRADING AND PROFIT AND LOSS ACCOUNT. | |

| An example of a BALANCE SHEET. | |

| True or False: A trading and profit and loss account is prepared to show the financial position of a business as at a particular point in time. | True. |

| True or False: The trading and profit and loss account shows that a business's income from sales in an accounting period is higher than the cost of the goods sold, and the expenses of running the business. Therefore, the business has made a net profit in the period. | True. |

| True or False: Net profit is transferred from the trading and profit and loss account to the owner's capital account at the end of an accounting period. The net profit increases the owners claim on the assets of the business. | True. |

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.